I have written quite a bit recently about off-price and discount retailers, some of which I believe could be positioned to outperform in (either case) strong or deteriorating macroeconomic environments. After turning bullish on Dollar General (DG) and TJX Companies (TJX), today I look at another robust performer: Burlington Stores (BURL).

Credit: Burlington Coat Factory

The New Jersey-based company reported earnings on August 30th. Interestingly yet not unlike other names in the space, shares dipped following a robust earnings beat and raised outlook, but staged a comeback over the past couple of trading days, likely the result of an investor rotation that has now fully flushed through the system.

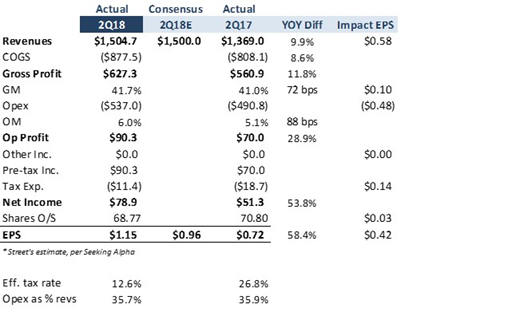

Regarding the results of the most recent quarter, revenues that rose nearly 10% YOY reflected a healthy combination of solid comps (2.9% on a shifted basis over last year’s already robust +3.5%) and 51 net new stores opened since the end of 2Q17 (which contributed with about 7% of top-line growth). Given the known challenges in the general retail sector, I like to see a company deeply engaged in footprint expansion, especially when such a strategy is complementary to solid management of existing stores. Lack of inorganic growth, in fact, is at the heart of my distaste for names like Big Lots (BIG).

Source: DM Martins Research, using data from company reports

Source: DM Martins Research, using data from company reports

Elsewhere in the P&L, I like to see both gross and op margins expand YOY. I believe strong pricing and possibly merchandise sourcing upside (same-store inventory, adjusted for back-to-school receipt acceleration, was down 2% despite positive comps) played a role in GM that rose 70 bps, more than offsetting the expected pressures from higher wages and freight costs. The above suggests to me that Burlington’s management team has been competently running a tight ship, despite the solid sales growth that could easily mask some level of inefficiency.

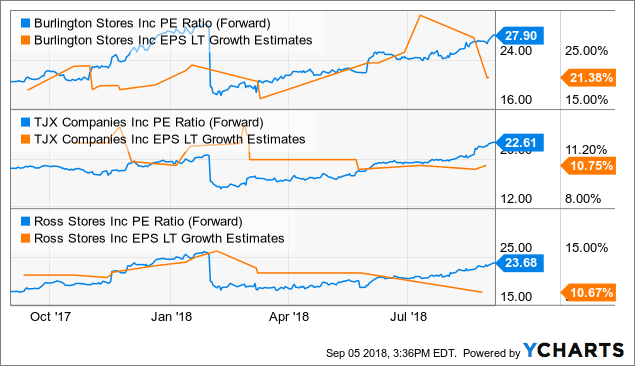

One potential concern regarding the stock are valuations. BURL currently trades at a forward earnings multiple of 27.9x, following a bull run that has pushed the share price up more than 40% YTD and caused the stock to nearly double in market value over the past 12 months. But as the graph below suggests, at least compared to peers TJX and Ross Stores (ROST), Burlington seems to have better earnings growth prospects. On a long-term PEG basis, and assuming no downside or upside to consensus estimates, BURL trades at a much more attractive 1.3x multiple compared to TJX’s 2.1% and ROST’s 2.2%.

BURL PE Ratio (Forward) data by YCharts

BURL PE Ratio (Forward) data by YCharts

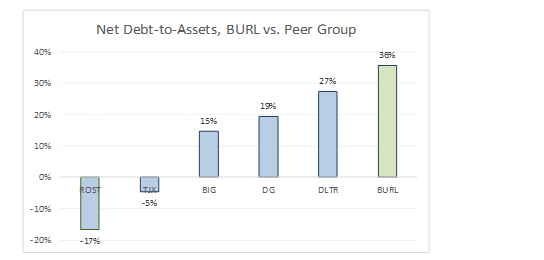

One of the possible explanations for BURL’s lower growth-adjusted earnings multiple is the company’s balance sheet leverage. The graph below illustrates Burlington’s heavy net debt position, particularly when compared to its key peers TJX Companies and Ross Stores.

Source: DM Martins Research, using data from company reports

Source: DM Martins Research, using data from company reports

All taken into account, I continue to favor an investment in TJX, in part due to the stock’s longer track record as a publicly-traded vehicle and its performance during bear periods that caused me to ask recently if the stock was “anti-gravity”. BURL, having IPO’d only in 2013, has yet to endure a severe downcycle as a public company.

I will likely keep BURL in mind and potentially bring it into my portfolio at a later date, should I choose to replace TJX at any point or complement my position for diversification purposes. Burlington’s shares may have risen sharply recently, but I believe they may continue to march forward even when economic growth and broad investor sentiment finally wane.

Note from the author: DG is only one of the names that I have discussed in more detail with my Storm-Resistant Growth community. To dig deeper into how I have built a risk-diversified portfolio designed and back-tested to generate market-like returns with lower risk, join my Storm-Resistant Growth group. Take advantage of the 14-day free trial, read all the content written to date and get immediate access to the community.

Disclosure: I am/we are long DG, TJX.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment