Quick Take

Zekelman Industries (ZEK) intends to raise gross proceeds of $100 million from a U.S. IPO, according to an S-1 registration statement.

The firm is an independent steel tubular manufacturer in the US and Canada.

ZEK is growing quickly but faces an uncertain tariff environment as trade negotiations fixate on steel and other basic goods.

Company & Technology

Chicago, Illinois-based Zekelman Industries was founded in 1877 to manufacture industrial steel pipe and tube products. The company owns 13 pipe and tube production facilities in seven U.S. states and one Canadian province, with total annual production of approximately 2.1 million tons.

Management is headed by Director, Executive Chairman and CEO Barry Zekelman, who was previously CEO of Atlas Tube.

Below is a brief video of one of the company’s latest commercials:

(Source: Zekelman Industries)

The majority of the company’s products are used in infrastructure and non-residential construction applications. It also supplies products for use in the fabrication, automotive, oil and gas, agricultural and industrial equipment and retail end markets.

Zekelman produces products that operate under specialized conditions, including in load-bearing, high-pressure, corrosive and high-temperature environments.

Market & Competition

According to a 2018 market research report by IBIS World, the North American industrial steel pipes and tubes market has reached $10.0 billion in 2018 and is projected to grow during the period between 2018 and 2023.

The main factors driving market growth are the growing demand from the energy sector and sustained demand from other key markets.

Major competitors that provide or are developing industrial steel pipes and tubes include:

- Allied Tube & Conduit

- Southland Tube

- Independence Tube

- Republic Conduit

- TMK IPSCO

- Bull Moose Tube

- EXL Tube

Financial Performance

ZEK’s recent financial results can be summarized as follows:

- Strong recent growth in topline revenue; previously uneven

- Consistent gross profit growth

- Uneven gross margin

- Decreased cash flow from operations

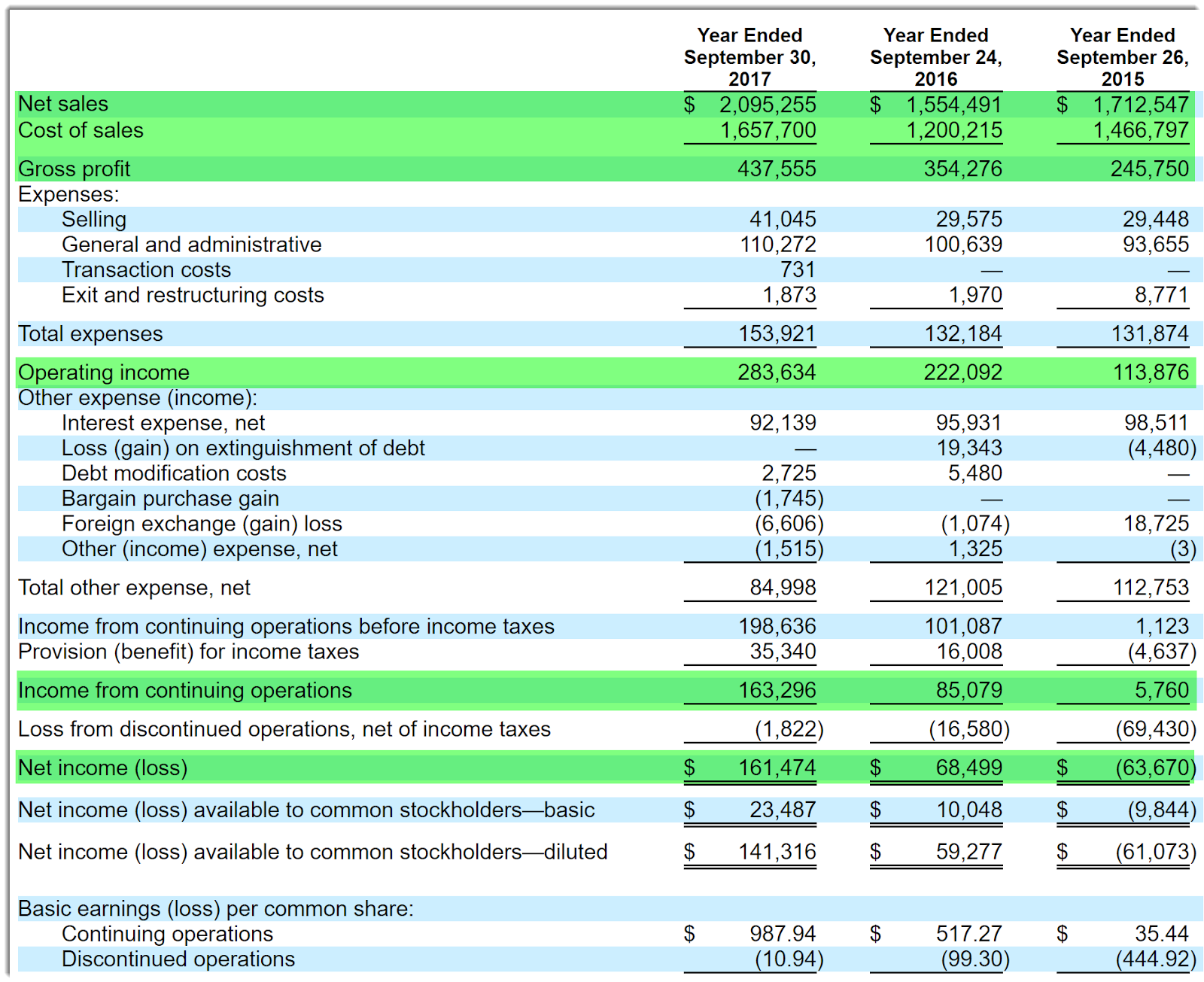

Below are the company’s financial results for the past three years (Audited PCAOB):

(Source: Zekelman S-1)

(Source: Zekelman S-1)

Total Revenue

- FQ3 2018: $1.98 billion, 33.9% increase vs. prior

- FYE 2017: $2.1 billion, 34.8% increase vs. prior

- FYE 2016: $1.6 billion, 9.2% decrease vs. prior

- FYE 2015: $1.7 billion

Gross Profit

- FQ3 2018: $473.0 million

- FYE 2017: $437.6 million

- FYE 2016: $354.3 million

- FYE 2015: $245.8 million

Gross Margin

- FQ3 2018: 23.9%

- FYE 2017: 20.8%

- FYE 2016: 22.1%

- FYE 2015: 14.4%

Cash Flow from Operations

- FQ3 2018: $100.9 million cash flow

- FYE 2017: $159.0 million

- FYE 2016: $174.1 million

- FYE 2015: $202.6 million

As of June 30, 2018, the company had $36.6 million in cash and $1.8 billion in total liabilities.

Free cash flow during the nine months ended June 30, 2018, was $40.0 million.

IPO Details

ZEK and selling stockholders intend to raise $100 million in gross proceeds from an IPO of its Class A subordinate voting stock.

Class B multiple voting stock will be entitled to ten votes per share vs. one vote per share for Class A shares.

Also, the firm will issue Special Voting Shares to the holders of Exchangeable Shares in one of its subsidiaries.

Multiple classes of shares are typically employed by management or existing shareholders to entrench their voting control even after losing economic control of the company.

The S&P 500 Index no longer admits firms with multiple share classes to its index.

Management says it will use the net proceeds from the IPO as follows:

We intend to use [an as-yet-undisclosed amount] of the net proceeds of this offering to repay a portion of our outstanding indebtedness. As of June 30, 2018, we had $1.3 billion of total indebtedness outstanding (excluding $10.3 million of letters of credit).

I expect the final amount sought in the IPO to be materially higher than $100 million, as ZEK needs to pay down its significant debt load.

Management’s presentation of the company roadshow isn’t available yet.

Listed bookrunners of the IPO are Goldman Sachs, BofA Merrill Lynch, BMO Capital Markets, Credit Suisse, GMP Securities, KeyBanc Capital Markets, William Blair, Stifel, BTIG and PNC Capital Markets.

Expected IPO Pricing Date: Not on the calendar.

An enhanced version of this article on my Seeking Alpha Marketplace research service IPO Edge includes my initial commentary on the IPO.

Members of IPO Edge get the latest IPO research, news, market trends and industry analysis. Get started with a free trial.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment