Royal Dutch Shell (NYSE:RDS.A) (NYSE:RDS.B) is an oil giant that has benefited from the rally of the oil price in the last 12 months, just like its peers. However, the oil major has paid the same dividend for 18 consecutive quarters, as it froze its dividend at the onset of the downturn of the oil market that began in 2014. Therefore, the big question is whether the company will raise its dividend in the upcoming quarters.

Dividend record

Despite the downturn that began in 2014, Exxon Mobil (XOM), Chevron (CVX) and Total (TOT) have continued to raise their dividends, albeit at a low single-digit rate. BP (BP) followed the same path as Shell and froze its dividend for 15 consecutive quarters, but eventually raised it in the running quarter, thanks to the strength of the oil price and the brightening outlook of the oil market. Therefore, Shell is the only oil major that has kept its dividend flat for such a long period.

While Shell is not a dividend aristocrat, it has an exceptional dividend record. To be sure, it has not cut its dividend since World War II. This degree of consistency is extremely rare, particularly for a cyclical stock, and is a testament to the strength of its business model and its execution.

On the other hand, Shell has remarkably slowed its dividend growth rate in the last decade, as it has raised it at an average rate of only 2.7% per year. This rate is much lower than that of its American peers. Nevertheless, the current 5.6% dividend yield of Shell is much higher than the 4.1% and 3.8% yields of Exxon and Chevron, respectively. If Shell resumes raising its dividend, it will have a much more attractive dividend than its American peers.

Free cash flows

Just like the other oil majors, Shell is highly leveraged to the oil price. Consequently, when the oil price began to plunge in 2014, the upstream segment of Shell, which used to generate the vast majority of its total earnings (~90%), saw its earnings collapse. As a result, the earnings of Shell in 2015 and 2016 came out 87% and 75% lower, respectively, than those in 2014. In addition, the free cash flows of the company plunged and hence they were insufficient to fund its dividend.

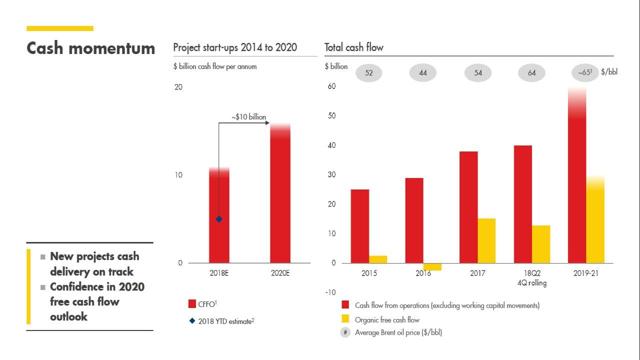

However, thanks to the production cuts of OPEC and Russia, and the drastic investment cuts of all the oil producers during the downturn, the oil market has eliminated its supply glut and has become much tighter this year. As a result, the oil price has enjoyed a strong rally since last summer and is now trading near a 3.5-year high. This rally has resulted in a great rebound of the free cash flows of Shell, which have bounced from -$1.5 B in 2016 to $14.8 B in 2017 and $8.9 B in the first half of this year. Hence the free cash flows of Shell have increased so much that they can easily cover the approximate $13 B in annual dividends. It is remarkable that Shell recently surpassed Exxon in annual operating cash flows ($35.7 B vs. $30.1 B) for the first time in about two decades.

Moreover, thanks to the recent fierce downturn of the oil sector, Shell has greatly improved its efficiency. It has reduced its operating expenses by 35% in the last four years while it has focused on investing in high-quality oil reserves, with markedly low breakeven prices. Furthermore, the company expects more than 700,000 barrels/day from projects that will start up this and next year. Overall, thanks to the strength in the oil price and expected production growth, the management of Shell expects the free cash flows to hover around $30 B per year during 2019-2021.

Such a level can easily cover not only the current dividend but also meaningful hikes in the upcoming years.

Management has noticed the excessive cash flows and recently initiated a 3-year share buyback program worth $25 B. Moreover, it has turned off the scrip dividend and thus it now pays the dividend only in cash, not in shares anymore. These two moves reflect the confidence of management in the brightening outlook of the company. As long as the oil price remains strong, which is the most likely scenario, the next move of the company will be to raise its dividend.

Final thoughts

After a fierce downturn in its sector, Shell has emerged stronger, with its free cash flows reaching all-time high levels. This is an outstanding achievement, as the price of oil is still about 30% lower than it was before the downturn that began in 2014. This performance confirms that Shell utilized the downturn in a highly productive way by cutting its expenses and investing only in high-return growth projects. Thanks to its excessive free cash flows and its exciting prospects, the oil giant has turned off its scrip dividend and has initiated a gigantic buyback program. The next move in its shareholder distribution policy will be to raise its dividend. Investors should expect a dividend hike in the upcoming quarters.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment