EvaluatePharma’s comprehensive “World Preview 2018, Outlook to 2024” estimates that Opdivo sales will grow by 10% compounded annually while Keytruda sales grow by an industry-topping 19%.

Over the past 4 quarters, Keytruda sales growth has been slightly more than double that of Opdivo’s, so the EP estimate is roughly in-line with the current spread.

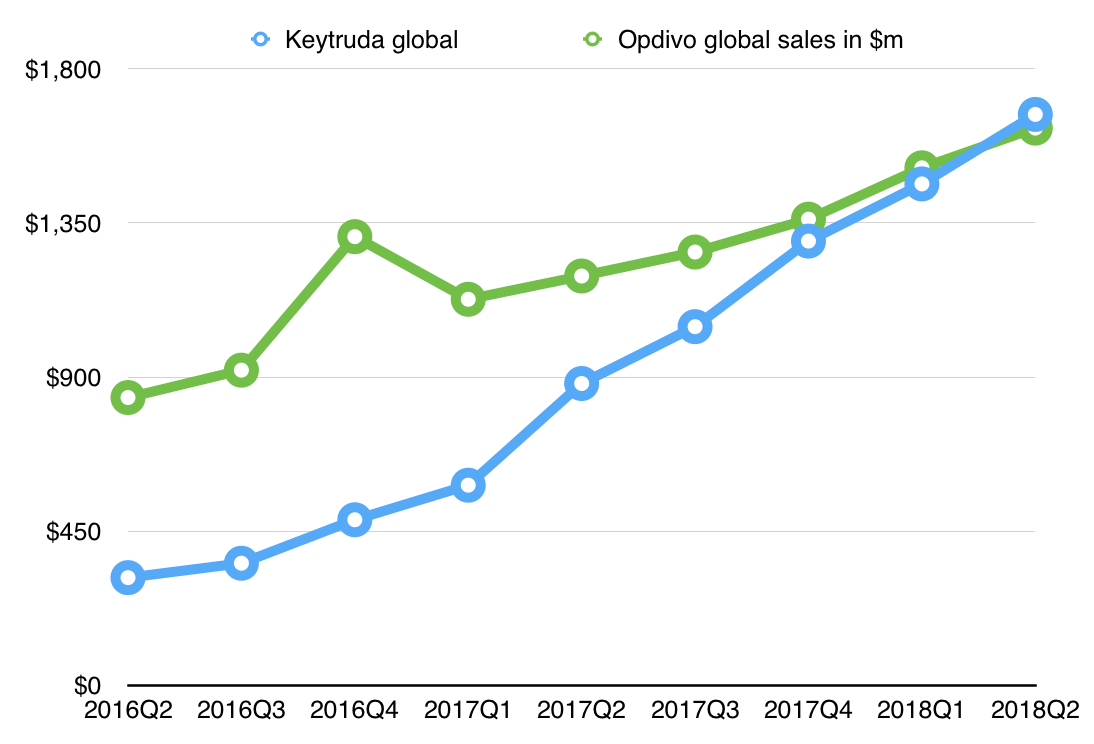

Source: Author using data from SEC filings

But nowhere in EP’s 47-page report is Bristol-Myers Squibb’s (BMY) Yervoy even mentioned, as if it is of no significant economic importance. Yes, Yervoy sales over the past 4 quarters have only been 1/5th that of Opdivo sales. But the Opdivo-Yervoy combination is gaining traction and evidence is accumulating that growth of both drugs should accelerate.

Following the FDA approval of the O-Y combo for renal cell cancer in April, Yervoy saw a resurgence in 2018Q2 after 4 quarters of declining sales.

But CheckMate 067 may have also helped fuel the Q2 rally in Yervoy sales. The National Comprehensive Cancer Network saw fit to upgrade the use of O-Y from category 2A to category 1 as first-line therapy in version2.2018 Guidelines for melanoma even though O-Y did little to extend the benefit of Opdivo alone on overall survival (Wolchok et al. NEJM 2017).

The weight of prior evidence is that blocking both CTLA-4 (Yervoy) and PD1 (Opdivo) offers synergism by targeting two distinct immune checkpoints.

CheckMate 204 should give Yervoy sales a further boost.

Results were published in the August 23 issue of NEJM. CheckMate 204 focused on patients with non-irradiated, asymptomatic melanoma brain metastases. As a phase 2 trial, there was no control arm, but among 94 patients treated with Opdivo and Yervoy in combination, a durable (>6 months) response was achieved in more than half, and in 76% of those positive for PD-L1.

The 54% rate of benefit with the O-Y combination compared favorably to the intracranial benefit for brain metastases in prior studies of Yervoy alone (24%), Opdivo alone (20%), and Keytruda alone (22%).

The authors of an accompanying editorial suggest that the Opdivo-Yervoy “regimen be considered as first-line therapy for all patients with brain metastases who meet the inclusion criteria for this study.” That would exclude a lot of sicker patients. But it would include a lot: more than a third of patients with advanced melanoma have brain metastases at diagnosis and up to 75% have brain metastases at the time of death.

A major goal in immuno-oncology is to determine why immune checkpoint inhibitors are so beneficial in some cancer patients but not at all in the majority. Researchers from Harvard have shed light on this enigma using data from the Checkmate 064 and 069 trials of Opdivo and Yervoy in patients with advanced melanoma.

Results were published in the 18 July 2018 issue of Sci. Transl. Med. (Rodig et al.). Important takeaways are the following:

- Melanoma cells resisted the effect of Yervoy in part by producing less of a protein called MHC class I which is required for recognition of cancer by immune cells (CD8+ T cells).

- MHC class I deficiency did not enable melanoma cells to resist the effect of Opdivo as long as it was given early in the course of therapy.

- MHC class I and II proteins are biomarkers that should be useful in determining which patients are more likely to respond to inhibitors of CTLA-4 (Yervoy) and PD1 (Opdivo) either alone or in combination (perhaps even better as biomarkers than PD1 and PD-L1).

- MHC class I deficiency in Yervoy-resistant cancers could be druggable.

MHC class I deficiency occurred in 43% of all patients which explains why so many are resistant to Yervoy. Finding solutions begin with understanding the problem.

EvaluatePharma forecasts worldwide prescription sales CAGR at +1% for Merck (MRK) and +6% for Bristol-Myers, but that CAGR from biotechnology will be about 200 basis points higher for MRK (11% versus 9%). The latter projection is reasonably tilted in favor of MRK because Keytruda has the NSCLC indication and BMY does not. But that could change.

Furthermore, because the EP outlook does include any mention of Yervoy or its recently improved growth prospects, I believe that BMY offers better growth than consensus estimates and better growth – even in biotechnology products – than MRK. Since they are priced at comparable multiples of earnings, I consider BMY to be undervalued and a better buy.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment