Virtu Financial (VIRT) has had a bad few months. Since its sky-rocketing rally early this year amid heavy market volatility up to almost $38 a share it has now slumped back down to $21 a share as volatility has simmered down.

As described in their post-earnings conference call, the decline in quarter-to-quarter revenue and net trading income was due to a mix of generally lower volatility and volume as well as lower retail trading action in the United States.

While the stock had already been declining before the earnings call for a mix of seemingly profit-taking reasons and worries over changes in market behavior, the earnings on July 27 then sent it plummeting again almost 15%.

Virtu Financial is now a company with a market capitalization of $4.02 billion, dividend yield of 4.55%, and P/E ratio of about 26.71 based on the adjusted EPS. Even after the recent collapse the stock is still up 15.30% YTD and 25.60% year-on-year, not to mention its dividend as well.

I still believe the company’s rightful valuation remains at the moment around the $30 to $35 range, giving it a market capitalization of around $5.7 billion to $6.6 billion. As we’ve seen, Virtu Financial remains an unusual financial services company because its precise business model and field of operations is quite distinct, as if taking slivers of the bulge bracket banks’ trading divisions and merging them with exchanges, brokers, and other boutique shops that often aren’t publicly traded.

Virtu Financial’s market behavior seems now extremely linked to the momentary net trading income it is bringing in each quarter, with its valuation then adjusting accordingly. If this is so, then in the upcoming few months we might only see moderate appreciation in price given expected seeming lower volatility as the market has stabilized from the recent tariffs conflicts.

Nonetheless, if we were valuing Virtu Financial on a broader estimation of the business’ value in terms of its extensive operations across tens of thousands of asset classes and seeming ability to increase its net trading income even amid the lower volatility of the past quarter, I think a stable level at $30 to $35 remains right.

A Less Turbulent Quarter But Still An Increase In Trading Income

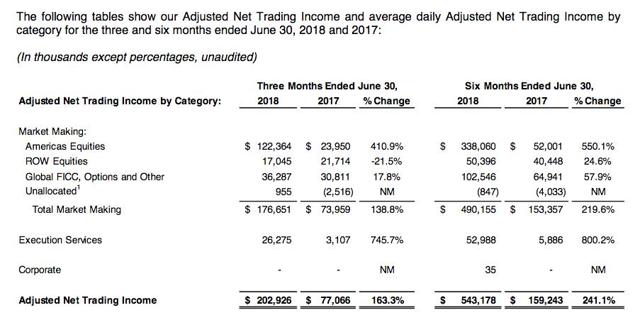

One particularly interesting thing I noticed in Virtu’s Q2 2018 earnings report was despite the relatively significant earnings miss, in terms of net trading income it still made quite the leap year-on-year despite what only seems like a moderately increase volatility environment.

(Source: Virtu Financial Q2 2018 Earnings)

On the negative side, and apparently a big reason for the earnings miss, was that operating expenses across the board have also increased in everything from data processing to employee compensation to interest expenses. As a cushion though, with an increase in operating expenses from $139 million in Q2 2017 to $278 million in Q2 2018 or essentially doubling, revenues grew about 128% from $144 million to $328 million.

One major question is that it remains to be seen if Virtu Financial can really find a way to better stabilize its net trading income and therefore perhaps give its own valuation more stability rather than being so tied to momentary events.

As we see with this quarter, the very profitable Q1 2018 for Virtu Financial amid extreme volatility in the wake of the market’s fierce reaction to the beginnings of the tariffs conflict dissipated quite significantly, dropping in net trading income over 43%.

(Source: Virtu Financial Q2 2018 Earnings)

Conclusion

I think Virtu Financial remains a company that has found an incredible niche and gained initial solid market share in an area which, as shown in Q1 2018, can get it enormous and consistent profit even when the broader market goes haywire.

As we also saw this quarter however there are many other factors that go into Virtu’s revenues and net trading income, ranging from volume to retail participation and which seem to consistently push Virtu Financial’s valuation to a very limited reference point of just the immediate few quarters around it.

With the broader market seemingly having priced in the continuing tariffs conflicts it seems volatility like we saw at the end of Q4 2017 and throughout Q1 2018 may not materialize again soon, making Virtu’s return to its prior $38 a share level, or more, seemingly unlikely at the moment. However I think at its current stage it still is undervalued to some degree and retains, even under its current valuation behavior, the ability to climb back to the $25-$30 level.

At Tech Investment Insights I discuss specific companies and investment products that I believe are especially poised to gain in the market, as well as the one to avoid.

Focusing on technology, in particular, I provide you updated risk/reward ratings of dozens of companies, price targets on potential worthwhile investments, portfolio strategies, and alluring risks to avoid. I hope you will give it a look.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment