Introduction

Over the past few months, most of you have noticed our increased activity in closed-end funds as the inflow of volatility finally shook them up and created various arbitrage, and directional, opportunities for active traders like us.

Now that these products have grabbed our attention, we are continuously monitoring most funds by sector and will reinstate our Weekly Review, publishing a recap of the groups of interest.

The Benchmark

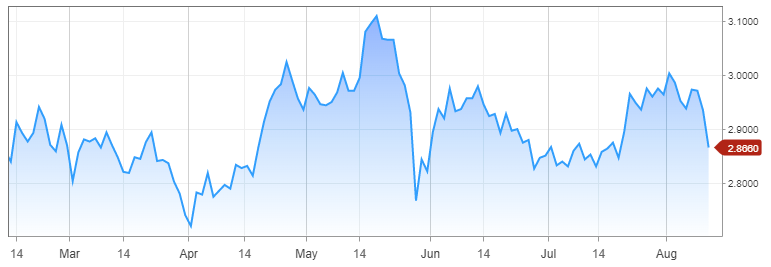

The price of the iShares National AMT-Free Muni Bond ETF (NYSEARCA:MUB) was struggling at the beginning of the week, but on Friday we saw a positive performance from the benchmark. Ultimately, we find an increase of $0.12 on a weekly basis. As a positive factor for the sector was the falling of US 10-year Treasury yield below the psychological level of 3%.

Source: Barchart.com – iShares National AMT-Free Muni Bond ETF

On Friday, the market participants changed their focus again on the safer assets. U.S. government debt prices jumped due to the global credit contagion fears surrounding Turkey. The Turkish lira collapsed to an all-time low against the U.S. dollar. Likewise, investors continue to monitor trade tensions between Washington and Beijing.

Despite the positive impulse for the fixed-income sectors, we remain cautious. No doubt, we are in raising interest rates environment and the market expects the next increase most probably in September.

The Munis are interest rate sensitive due to their higher duration compared to the corporate bonds, high yield (junk) bonds or floating rate bonds. On the other side, Munis provide downside protection in a recessionary environment because of their less chance of default. They will still fall but much less.

Source: CNBC.com, US 10-Year yields

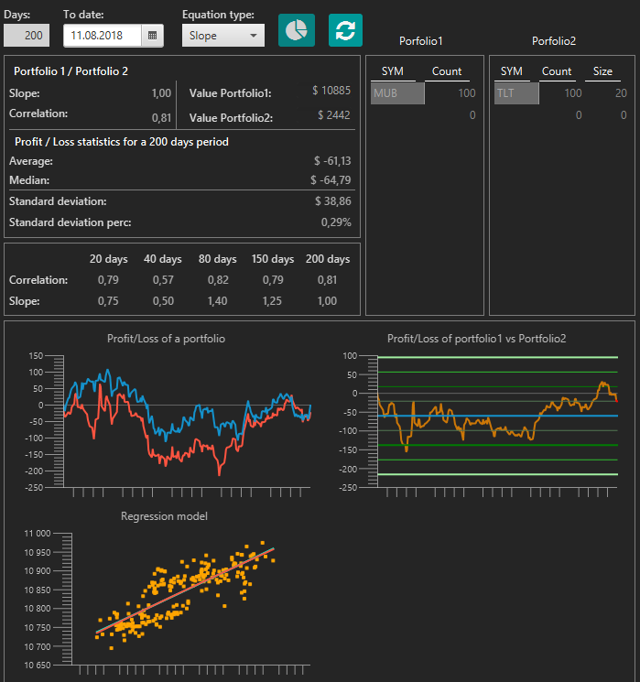

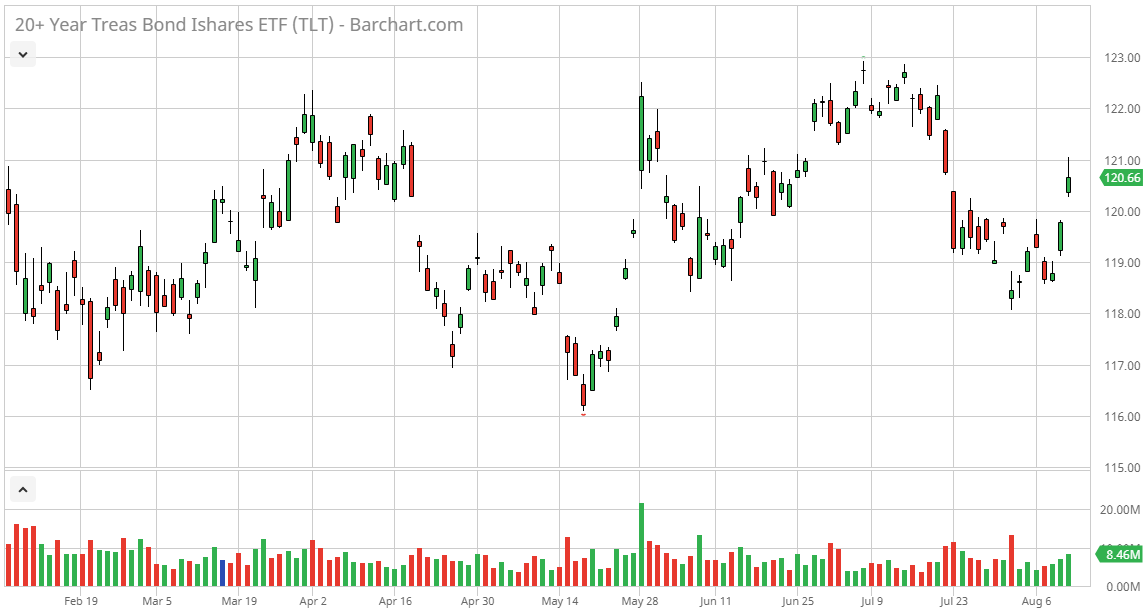

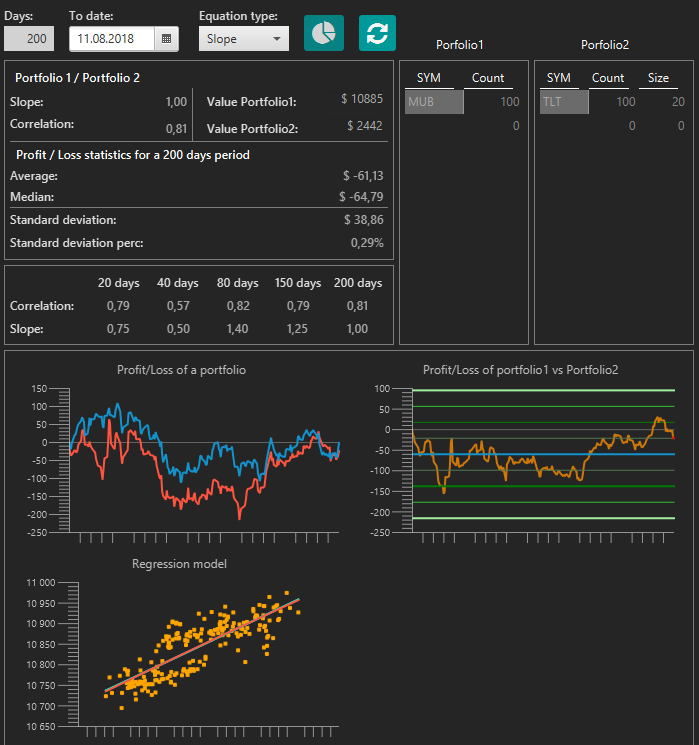

As you know, we follow the performance of the U.S. Treasury bonds – considering them the risk-free product – with maturities greater than 20 years: the iShares 20+ Year Treasury Bond ETF (NYSEARCA:TLT). The reason for that is the strong correlation between these major indices and the chart below proves it. Additionally, a statistical comparison is provided by our database software:

Source: Barchart.com – iShares 20+ Year Treasury Bond ETF

Source: Author’s software

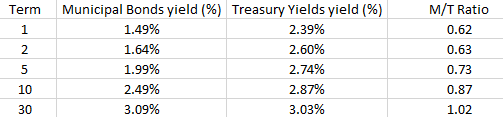

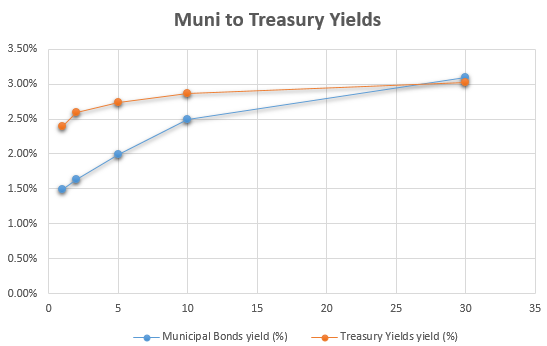

Comparison Of The Yields And Municipal/Treasury Spread Ratio

Investing in municipal bonds is popular because they have the potential to offer higher yields than similar taxable bonds. If an investor wants to know whether muni bonds are cheap in comparison to taxable bonds or Treasuries, they could find out by comparing them. However, this method does have its limitations, and the investor should perform a more thorough analysis before making a decision:

Source: Bloomberg.com, Municipal and Treasury Yields

Source: Bloomberg.com, Municipal and Treasury Yields

The Municipal/Treasury spread ratio, or M/T ratio as it is more commonly known, is a comparison of the current yield of municipal bonds to U.S. Treasuries. It aims to ascertain whether or not municipal bonds are an attractive buy in comparison. Essentially, an M/T ratio north of 1 means that investors receive the tax benefit of muni bonds for free, making them even more attractive for high net worth investors with higher tax rate considerations.

Source: Bloomberg.com, Municipal and Treasury Yields

Weekly Charts

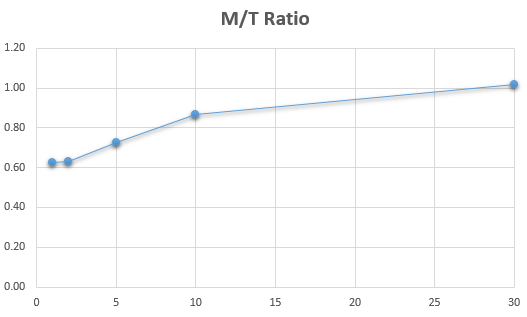

1. Funds traded at discount and Z-score less than -1.50 points

Source: CEFConnect.com

2. Funds traded at discount and yield on NAV above 5%

Source: CEFConnect.com

Source: CEFConnect.com

The News

Source: Yahoo News, Municipal Bond Closed-End Funds News

Over the past week, several funds from the sector announced their regular dividends:

| Fund | Distribution rate |

| Delaware Investments Minnesota Municipal Income Fund II (NYSEMKT:VMM) | $0.0375 |

| Delaware Investments National Municipal Income Fund (NYSEMKT:VFL) | $0.0500 |

| DWS Strategic Municipal Income Trust (NYSE:KSM) | $0.0500 |

| DWS Municipal Income Trust (NYSE:KTF) | $0.0475 |

| Federated Premier Municipal Income Fund (NYSE:FMN) | $0.0540 |

Review Of Municipal Bond CEFs

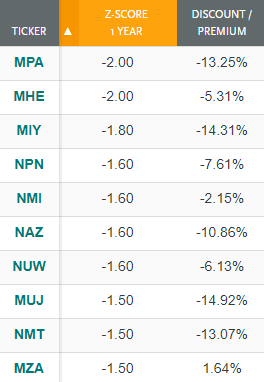

1. Lowest Z-Score

Source: CEFConnect.com

Sorting the funds by the lowest Z-score, we find out that more of the funds are statistically undervalued. The Z-score is an appropriate indicator to see how many times the discount/premium deviates from its mean for a specific period. In our case, we use it to find closed-end funds with a statistical edge for a “Long” position. Currently, the average 1-year Z-score for the sector is -0.52 point.

BlackRock MuniYield Pennsylvania Quality Fund (NYSE:MPA) is sharing the first position with Massachusetts Health&Education Tax-Exempt Trust (NYSEMKT:MHE). Both of them have Z-score equals to -2.00 points, but the discount of BlackRock MuniYield Pennsylvania Quality Fund makes it more interesting to me.

Source: CEFConnect.com, BlackRock MuniYield Pennsylvania Quality Fund

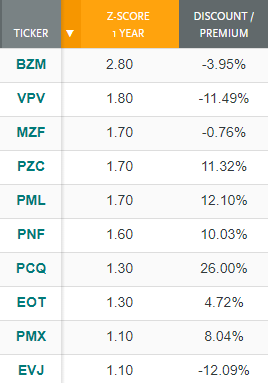

2. Highest Z-Score

Source: CEFConnect.com

On the other side of the coin are the funds whose Z-score indicates that they should be overpriced at the moment. Of course, the statistical parameter is not telling us the whole story and we can use it only as a starting point for our analysis.

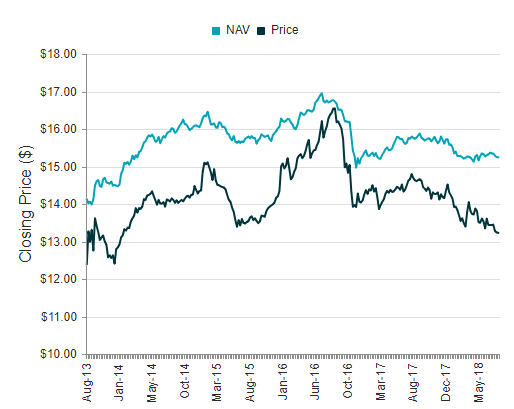

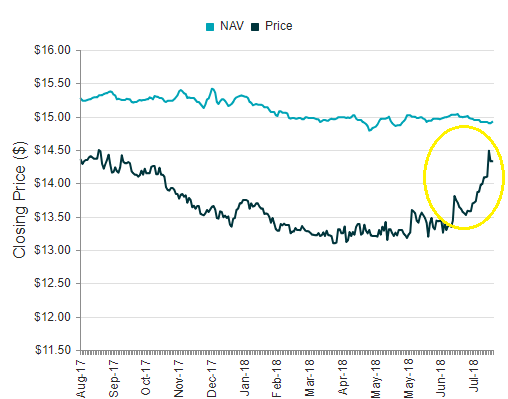

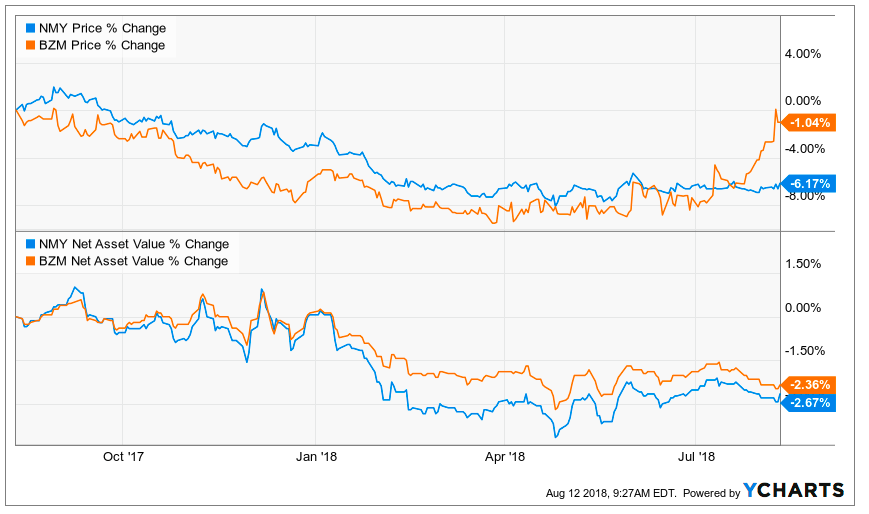

The fund which caught my attention last week was the leader of the chart BlackRock Maryland Municipal Bond Trust (NYSEMKT:BZM). On a weekly basis, its Z-score has increased by another 0.80 point to 2.80 points. It is still trading at a discount, so I will not keep it as a naked “Short” position, but why not to include it in a pair trade.

Source: CEFConnect.com, BlackRock Maryland Municipal Bond Trust

Source: Ycharts, BlackRock Maryland Municipal Bond Trust and Nuveen Maryland Premium Income Municipal Fund

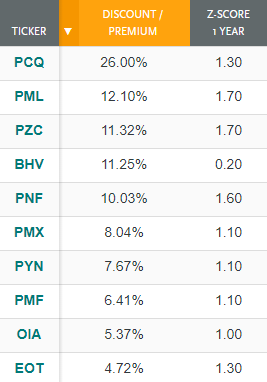

3. Biggest Discount

Source: CEFConnect.com

The above ranking highlights the current market situation and proves that there are many interesting “Buy” opportunities in the sector. I think it is worth it to spend some time to review NBW, MUJ as potential “Long” positions. Currently, they offer an attractive discount and we see relatively low Z-score. The average discount/premium for the sector is -7.87%.

4. Highest Premium

Source: CEFConnect.com

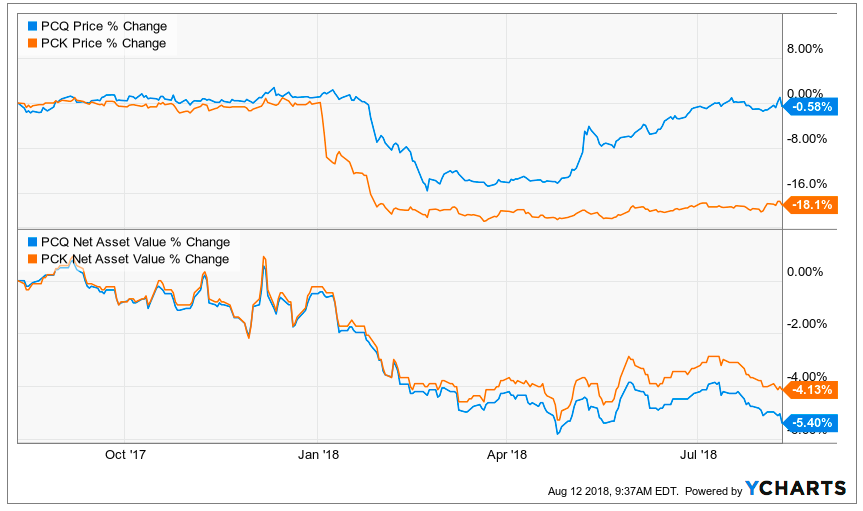

The funds plotted here are trading above their net asset value, which is a sign that we can find potential “Short” candidates. Ideally, our “Sells” should have a Z-score as high as possible. I still consider the PIMCO California Municipal Income Fund (NYSE:PCQ) and the Pimco California Municipal Income Fund II (NYSE:PCK) as an interesting arbitrage trade.

Probably, you noticed the dominance of the PIMCO funds. The market participants constantly pay a premium for them. If we do not have a strong logic behind our “Short” position, it can lead to unfavorable results.

Source: Ycharts, PIMCO California Municipal Income Fund and Pimco California Municipal Income Fund II

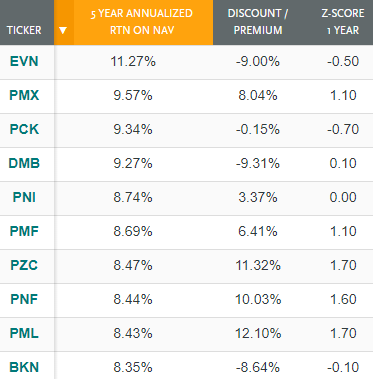

5. Highest 5-year Annualized Return On NAV

Source: CEFConnect.com

The above sample shows the funds with the highest return on net asset value for the last 5 years. The raw data is just answering the question why mainly these funds are traded at a premium.

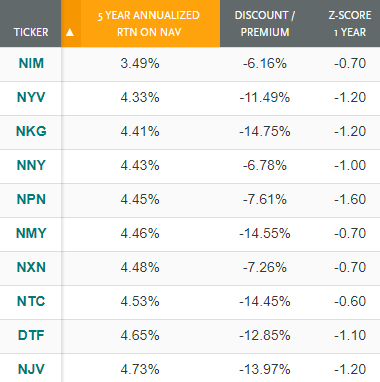

6. Lowest 5-year Annualized Return On NAV

Source: CEFConnect.com

If you want to bet on a stable credit quality and no leverage, Nuveen New York Municipal Value Fund 2 (NYSE:NYV) looks like a possible choice for your portfolio. Armed with a discount of 11.49% and a Z-score of -1.20 points, the fund may be reviewed as a potential “Buy” candidate by those who are not fans of the leveraged funds.

Source: Fund Sponsor Website

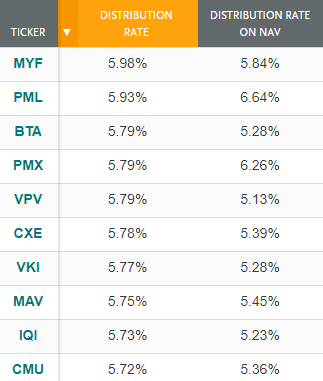

7. Highest Distribution Rate:

Source: CEFConnect.com

The table shows the funds with the highest distribution rate on price. Additionally, I have included here the distribution rate based on the net asset value. Most of the market participants find the second metric to be more important.

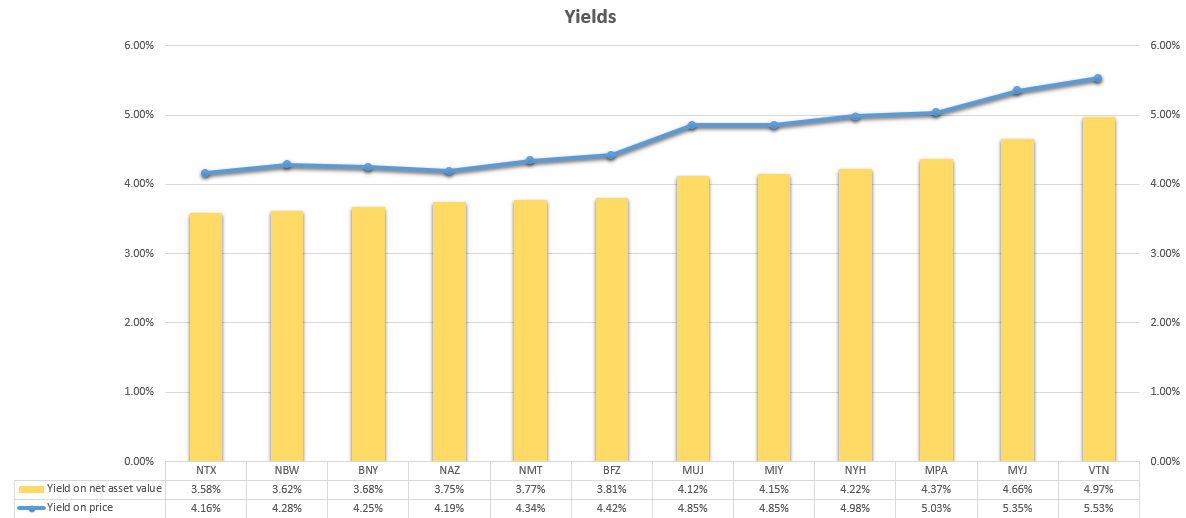

Below on the chart, I plotted the yields of funds from the sector with a discount of more than 10% and a Z-score less than -1.30 points.

Source: CEFConnect.com

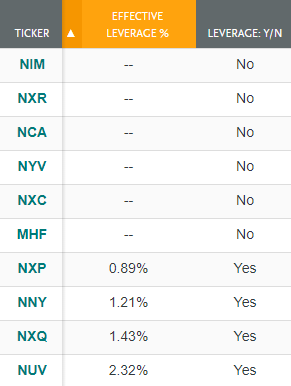

8. Lowest Effective Leverage %

Source: CEFConnect.com

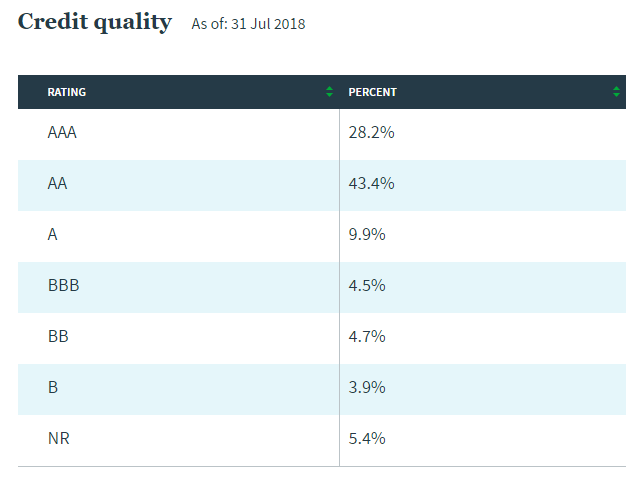

From a leverage perspective, we have six closed-end funds whose effective leverage is equal to zero. Do not underestimate the effect of the leverage, and be sure it is included in your analysis.

Conclusion

Definitely, the change of the interest rates will play a role, and we should anticipate a reflection on the Muni sector as well. Compared to the previous year, the discounts of the closed-end funds holding such products have significantly widened. While I find this to be fundamentally justified, I always expect some buying impulse to give us at least a mean-reversion trade in these products.

Note: This article was originally published for our subscribers on 8/12/2018, and some figures and charts may not be entirely up to date.

Trade With Beta

At ‘Trade With Beta‘ we also pay close attention to closed-end funds and are always keeping an eye on them for directional and arbitrage opportunities created by market price deviations. As you can guess, timing is crucial in these kinds of trades; therefore, you are welcome to join us for early access and the discussions accompanying this kind of trades

Disclosure: I/we have no positions in any stocks mentioned, but may initiate a long position in PCK over the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment