It’s obviously always good news when a company beats both its earnings and sales estimates. However, in case of Phillips 66 (PSX), we see that the company is not only perfectly able to turn a favorable market environment into strong bottom line growth but also that the company is expected to continue to do really well in the current market, thanks to strategic investments and strong economic growth. The company remains a solid long-term buy.

Source: Phillips 66

The Second Quarter Was A Hugh Success

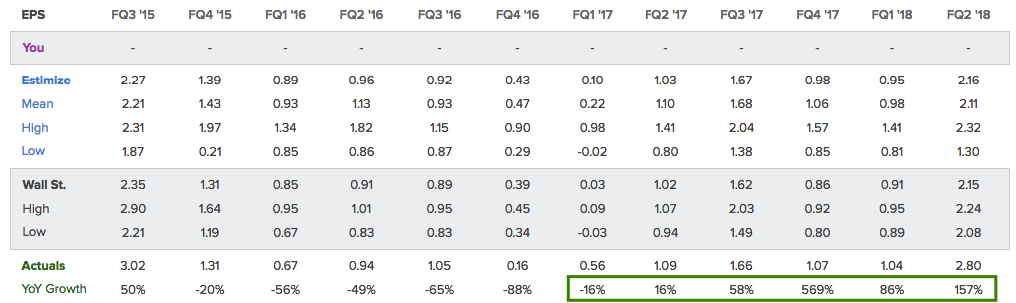

The second quarter of this year saw a massive earnings beat. Phillips 66 reported earnings of $2.80, which is $0.65 above expectations and 157% higher compared to the prior-year quarter. This is also the 6th consecutive earnings beat since the fourth quarter of 2016.

Source: Estimize

Source: Estimize

Sales came in at 29,736 which is roughly $300 million above expectations and 21% higher compared to Q2 of 2017. The bigger picture shows that sales (on a trailing twelve months basis) are in a very strong recovery. Earnings are already back at their pre-slowdown highs.

PSX data by YCharts

Adjusted earnings soared 132%. The difference between total net earnings and EPS, in this case, is the lower share count of 471,638 shares compared to 520,160 shares in Q2 of 2017.

That said, the company achieved strong growth in 3 out of 4 segments. The overview below shows the net income (in $MM) changes between Q2 of 2017 and Q2 of 2018 per segment.

- Refining $233 -> $911 (+291%)

- Chemicals $196 -> $262 (+33.7%)

- Midstream $101 -> $202 (+100%)

- Marketing & specialties $218 -> $195 (-10.6%)

Refining, which is the company’s main business segment, benefited from strong economic growth and high product demand. However, there were also other facts that caused the company to massively beat estimates. Pipeline constraints for Canadian crude made this type of oil cheaper than oil from other places. Phillips 66 has the capabilities to process more of that oil. This was one of the reasons why the company achieved a utilization rate of 100% while margins per barrel improved to $12.28. Hence, net income was able to grow from 2.24% in Q2/2017 to 4.50% in Q2 of this year.

PSX data by YCharts

PSX data by YCharts

What’s Next?

Phillips 66 is now working to keep these margins high. The company continues to invest in its midstream operations. The biggest two projects are the Gray Oak Pipeline and the Sweeny Hub. The Gray Oak pipeline will provide crude oil transportation from the Permian in Eagle Ford to Texas Gulf Coast destinations, including the Sweeny Refinery. This means that the company is further expanding its network in an oil region that is currently suffering from outperforming production growth and a too low takeaway capacity. The pipeline will have an initial capacity of 800,000 barrels per day. The pipeline is expandable to roughly 1,000,000 barrels per day and will be fully operational by the end of 2019.

Besides the company’s own measure to capture as much growth as possible, it is important to mention that the macro situation is also quite favorable of a long Phillips 66 position.

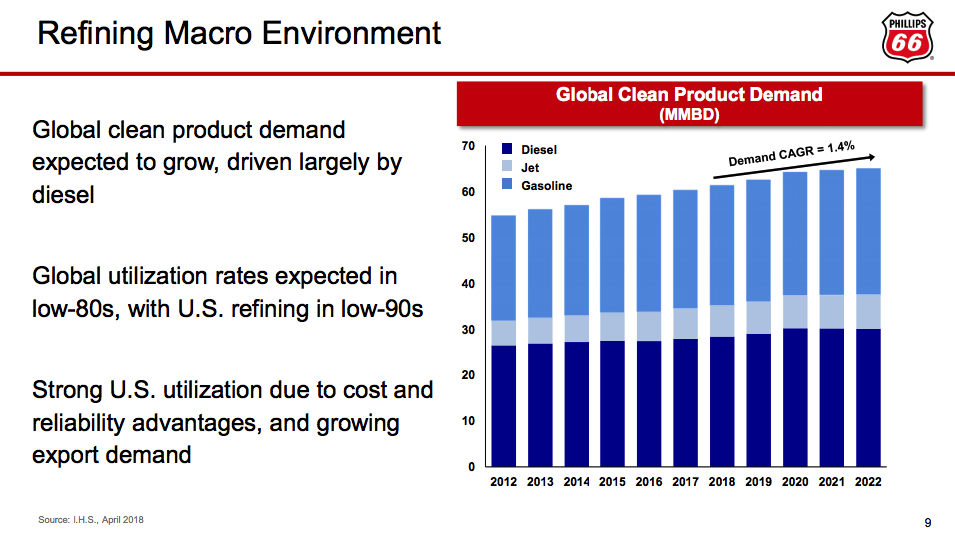

Refining companies in the US will continue to benefit from high clean product demand growth. Clean product demand is growing 1.4% on a CAGR basis between 2018 and 2022, according to Phillips 66. Additionally, US companies will be benefiting from growing export demand which will lift utilization rates above the international average by roughly 10 points.

Source: Phillips 66 Investor Presentation August 2018

Source: Phillips 66 Investor Presentation August 2018

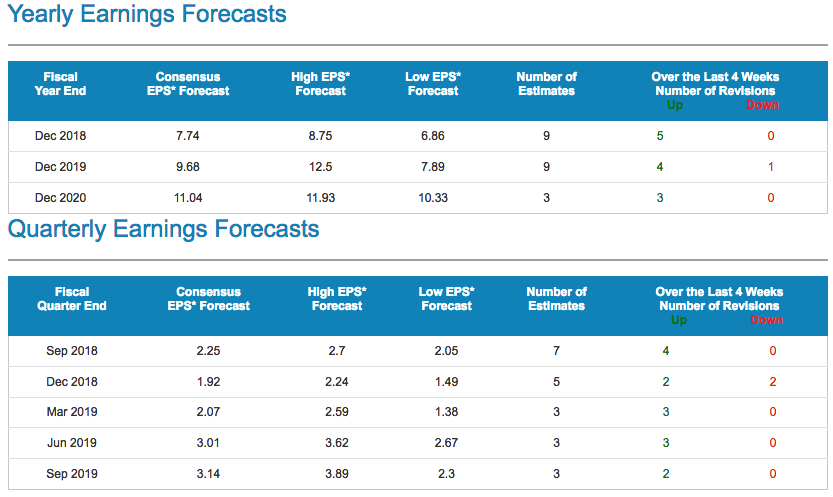

Analysts seem to agree that Phillips 66 is in a very good place. EPS estimates are rising across the board. 2018 alone has gotten 5 upgrades over the past 4 weeks while both 2019 and even 2020 got each 3 net upgrades. The same goes for quarterly expectations. Only the fourth quarter of this year got 2 downside revisions.

Source: Nasdaq

Source: Nasdaq

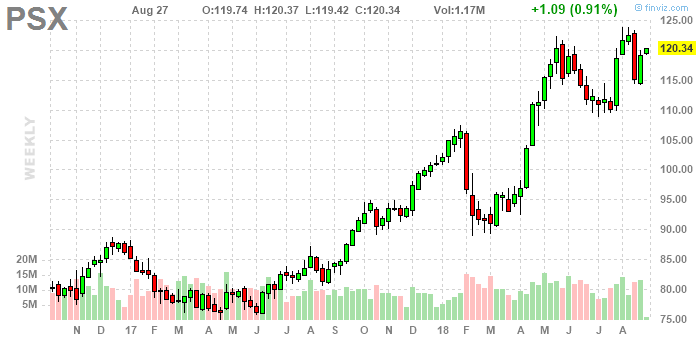

When it comes to the company’s stock price, I believe that we are in for an extended rally. The valuation is extremely attractive. The Phillips 66 is trading at 19 times earnings with a forward PE of 12.1 and a PEG ratio of just 0.57.

The downside risk is a slowing (global) economy. This would massively lower utilization rates and pressure export volumes. However, at this point, I am not worried that petroleum products demand is going to decline over the next few months and maybe even beyond.

The downside risk is a slowing (global) economy. This would massively lower utilization rates and pressure export volumes. However, at this point, I am not worried that petroleum products demand is going to decline over the next few months and maybe even beyond.

All things considered, I have to say that Phillips 66 is in a very good spot. The company continues to benefit from strong petroleum products demand, rising exports, and overall economic growth. Adding to that, the company is positioning itself to benefit even more from Permian oil growth by adding pipelines and additional refining capacities.

I expect the current earnings growth streak to continue well into 2019. Also note that the company is paying a 2.7% dividend yield, which makes the trade even more interesting in the long term. I am very excited about this trade and think this company will go much higher from here.

Stay tuned!

Thank you for reading my article. Please let me know what you think of my thesis. Your input is highly appreciated!

Disclosure: I am/we are long PSX.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: This article serves the sole purpose of adding value to the research process. Always take care of your own risk management and asset allocation.

Be the first to comment