Okta’s (OKTA) share price has seen a 100% growth since the beginning of the year. Yet when investors see Microsoft (MSFT) and Oracle (ORCL) as competitors, sentiment shifts, as belief that a small company can compete and succeed in the enterprise software industry diminishes. However, by understanding the specific niche that Okta covers, investors should see the cloud war among Amazon (AMZN), Microsoft and Oracle serve as a positive growth factor for Okta. As long as the enterprise software industry remains competitive, companies will look to remain flexible and avoid vendor lock-in, which frees Okta to continue growth in the long run. Okta provides companies with a “single sign-on” solution, offering a user authentication software that will help companies mitigate cyber threats, and comply with data privacy regulations.

Data Privacy Industry Growth

Before understanding how Okta can succeed in the long run, we should first look at how the data privacy industry is growing. The General Data Protection Regulation (GDPR) has been implemented. IT departments now have a major requirement that needs to be added to almost any project. The failure to do so? Companies will be forced to pay an incredibly high fee. GDPR is also not the end of the data privacy regulations, as multiple countries, including India and America, are looking to fortify their own countries’ data privacy needs.

To counteract this, spending in data privacy is growing quickly. Data privacy and cybersecurity are expected to become a $1 trillion industry in the next few years. But the damages of cyber threats? Expected to be about $6 trillion annually by 2021.

Where does Okta fit in this? One of the main types of cybersecurity attacks comes from spoofing, which is where a hacker attempts to enter a system pretending to be a client or user, allowing the hacker to successfully infiltrate it. User authentication is how companies mitigate this, and Okta provides a vendor flexible authentication solution. (For investors interested in learning how multi-factor authentication is used to meet GDPR rules, I recommend this post).

Source: Akins IT

Understanding the Need for Okta

The Okta Identity Cloud is the main offering of Okta. It integrates with already existing company software, and allows users to log in through Okta, then access their enterprise software. Effectively, it becomes the gateway to the company’s system. From Okta’s 10-K, “We designed the Okta Identity Cloud to provide organizations an integrated approach to managing and securing all of their identities. Our platform allows our customers to easily provision their customers, employees, contractors, and partners, enabling any user to connect to any device, cloud or application, all with a simple, intuitive and consumer-like user experience. Developers leverage the Okta Identity Cloud to secure and manage the identities of their own customers accessing their cloud and mobile applications.”

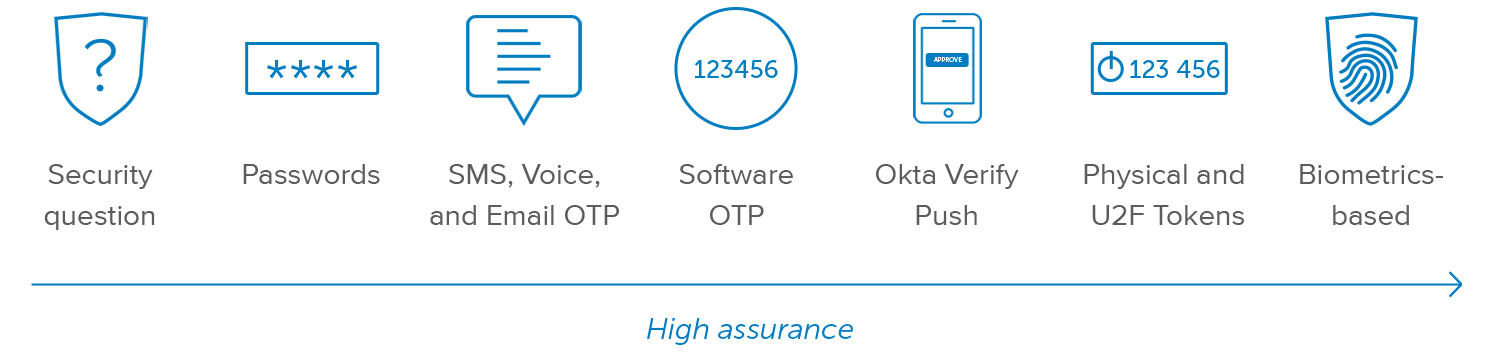

Okta is providing companies an easy way to comply with GDPR provisions regarding user identity and spoofing. Within the Okta product, companies can add two-factor authentication and/or multi-factor authentication to their own ecosystem. This allows companies to choose their security parameters (image below), and provide a simple platform for allowing employees to go through authentication, then proceed to whichever application they need to access, regardless of who the vendor is.

Source: Okta

Okta’s Moat

The advantages of Okta over similar offerings from Microsoft and Oracle is that it is a focused platform, with one purpose. This is important because their competitors offer a similar platform, but it can only be used with that vendor’s software. Meaning Microsoft MFA can only be used with Microsoft products.

Okta recognizes this, and have focused their R&D to provide a solution that is designed to be easily integrated with other cloud and enterprise software platforms their customers already use. This ease of integration is crucial for remaining flexible and meeting a growing and changing list of data privacy regulations, as GDPR has shut down products that do not comply with their standards.

A vendor flexible solution is the key to building Okta’s moat. Microsoft offers Azure Multi-Factor Authentication, and Oracle and AWS (Amazon Web Services) also offer their own MFA add-ons. The companies will choose Okta’s solution over their current vendor for two reasons: Companies want to remain flexible in their IT department, and avoid vendor lock-in.

Vendor lock-in is where a customer uses one company as their main cloud provider, and the cloud infrastructure becomes so ingrained into the customer’s business that a customer is “locked in” with this software. This gives the vendor pricing power, and leads to an overall shift of power as the customer is a victim to whatever terms the vendor gives.

Okta’s main differentiation from Amazon and others is their ability to provide a platform that allows companies to switch cloud providers without having to reconfigure their authentication software (avoiding vendor lock-in is a key factor for future growth for Okta, and I recommend this article if you want more information).

To summarize the above, Okta provides a single platform solution that serves companies that have more than one cloud provider, or companies that want the flexibility to change to a better or cheaper cloud provider in the future. Their competitors do not, and do not have an incentive to provide this, as they want customers to use all of their own products.

Understanding Risks

However, there is the risk of customers that don’t want the flexibility. If customers are aware of the risk of vendor lock-in, but still believe in the end that this will provide cost savings, then Okta becomes severely disadvantaged. This can come from a company deciding that retraining their employees to use a new cloud service, or the costs of switching providers, outweigh the savings of switching to a cloud provider with better costs or services. Also, companies that have only one cloud provider will likely just use the authentication software product associated with it (such as Microsoft’s Azure MFA for clients using Microsoft Azure). Also, if competition decreases in the cloud industry, Okta will likely see their growth prospects diminish, as Okta relies on a competitive cloud industry that encourages customers to remain flexible.

The other risk often cited, which I view as highly unlikely, is that one of the big cloud providers will offer a product similar to Okta. But this doesn’t make sense in terms of overall profitability. Cloud providers want to develop an entire ecosystem. Using vendor flexible software doesn’t help them; they want you to use their cloud offering, then expand and use their supporting products. Creating a product that allows a customer to easily switch to a competitor will be counterintuitive, and ruin the high-switching cost aspect of the enterprise cloud industry.

Financials – Revenue Structure and Path to Profitability

Okta is a great investment for those seeking exposure to the growing data privacy industry. However, Okta’s shares have also seen a nearly 100% increase so far this year. With the stock falling within the last week, along with other tech stocks, it’s important to see if Okta still has room to grow.

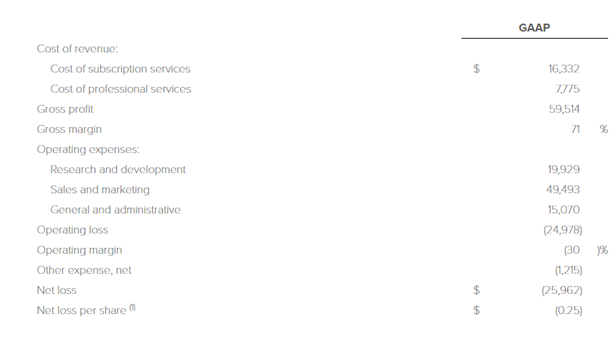

In the last earnings call (transcript here) and earnings release, Okta reported a revenue increase of 60% YoY, totaling $83.6 million. Most of this is attributed to a rise in subscriptions, their main source of revenue. Okta sells their products through multi-year subscriptions, which ensure both steady sales and high switching costs. On the margin side, we see a GAAP operating margin of 71%, ensuring a clear path to future profitability.

Source: Okta Investor Relations

Okta won’t be seeing positive earnings for a while, and they warned investors of this in their 10-Q. R&D and sales and marketing expenses are also growing sharply YoY, so Okta will be trading in earnings for growth for the foreseeable future.

But despite the lack of earnings, investors still want to see positive cash flow. In the last quarter, Okta has lowered their FCF margin loss from -26% to -2%, and is on pace to become free cash flow positive by end of the year, if not next quarter. This should ease concerns for a company that is giving up earnings for growth.

Also, another positive trend is the operating cash flow. Okta started the year being operating cash flow positive for the first time, and saw this increase significantly last quarter, from $0.16 million to $3.97 million. Again we want to check cash flows to see any warning signs, not necessarily to provide a valuation, as we understand Okta’s growth model, and the importance of spending heavily in growing the business.

Okta also released revenue guidance, expecting 2019 revenue to be between $353 million and $357 million, although it should be noted Okta has continuously beat their guidance with ease. For these high growth companies, I like to use P/S to determine if the stock is overvalued. As of this writing, Okta’s market cap is at $5.45 billion, giving us a P/S ratio slightly above 15. When we use the 2020 revenue expectations, $470 million, we now see Okta’s future P/S ratio sit at 11.6.

However, these P/S ratios are likely on the high end. Okta’s ability to easily outpace guidance has caused analysts to become skeptical. In the earnings call, Heather Bellini from Goldman Sachs (NYSE:GS) asked, “… if I look at your sequential revenue guidance given how well you guys did in Q1, it looks like you’re implying flat up 2% kind of sequential guide. I am just wondering under what circumstances would like what would have to happen to you guys to see kind of flat sequential revenue growth kind of what things would be factored into that just given all the great momentum in your business?”

CEO Todd McKinnon replied that there were big deals in Q4 2018 that ended up being deployed in Q1 2019. He also stated, “The second thing is that during the course of the Q1 quarter, we had a lot more linearity in the business than we had anticipated.” Either investors should take this as leadership seeing some difficult situations in the near future, or that they’re looking to make headlines by greatly exceeding expectations. I think it’s the latter.

Without any noticeable warning signs in the financials for a company in this situation, investors should focus on two metrics: revenue growth and operating margin. How fast is this company growing? And is there a path to profitability? With revenue growth forecast to be 40% YoY next quarter (and I view this as a low conservative guidance) and current operating margin at 71%, I believe the financials solidify the case that Okta’s business model is growing, and has a solid path to profitability.

Investor Takeaway

Okta is providing investors a solid risk/reward investment for those seeking high growth investments. Data privacy spending is growing and will continue to grow, Okta is effectively creating a moat against mega-cap competitors, and they are doing this without risking financial stability. The two most important metrics investors need to consider (revenue growth and operating margin) both provide a clear picture that Okta’s business is sustainable, and their business model is effective.

Okta serves as a good risk/reward investment for the growing industry’s need. Okta’s recent sell-off looks like a good time to start a position. However, investors may want to wait to see if the tech sell-off continues, but interested investors will likely want to begin entering a position before their next earnings call, where Okta will look to easily exceed their questionably low guidance.

Disclosure: I am/we are long OKTA.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment