Making a virtue of necessity, Eversource Energy (NYSE:ES) is transforming itself into a clean energy/lower-hydrocarbon supplier of electricity and natural gas. After being required to sell most of its electrical generation plants, the company is focusing more narrowly on electrical transmission and distribution, as well as natural gas distribution. It is also growing its water supply division and has solar and wind energy-fueled generation projects underway. This regulated utility holding company offers a solid, consistently growing dividend.

Brief Company Summary

Eversource Energy is an energy delivery company headquartered in Springfield, Massachusetts, with four general divisions: electrical transmission, electrical distribution, natural gas distribution, and water distribution. It is the holding company for several regulated subsidiaries: a) in electrical distribution and transmission – Connecticut Light and Power, Public Service Company of New Hampshire (PSNH), and NSTAR Electric Company serving Massachusetts, b) in natural gas distribution – Yankee Gas, NSTAR Gas, generation facilities of PSNH, Aquarion, and c) the solar power facilities of NSTAR Electric.

Eversource employs 8100 people full-time. The company serves 3.5 million electric and gas customers in three states, which it divides into four regions as shown below: New Hampshire, eastern Massachusetts, western Massachusetts, and Connecticut. All are part of the ISO-NE electric reliability grid.

Eversource Electricity Supply

In 2015, Eversource agreed to sell most of its generation facilities as part of a major restructuring and rate stabilization agreement. In January 2018, it sold its hydrocarbon-fueled (coal, oil, gas, and wood) generating facilities comprising 1130 MW of capacity to Granite Shore Power, LLC. Last week, at the end of August 2018, it completed the sale of its nine hydroelectric generating units with 68.2 MW of capacity to Hull Street Energy, LLC. Under the sales agreements, the new owners have to keep the plants in service for at least 18 months.

The company retains ownership in a few small solar projects. However, it now buys most of its electricity on the wholesale market.

Natural Gas Supply

As Eversource detailed in its annual report presentation, its service area is less than two hundred miles from the enormous Marcellus natural gas reserves. Among its goals are to encourage New England households to switch from expensive and higher-carbon heating oil – New England is the only region in the country so reliant on oil for heating – to cleaner and less expensive natural gas.

In particular, the company pointed out that last winter’s cold snap highlighted the unavailability of ready natural gas supplies – resulting in $0.5 billion of additional costs in 13 days – that some plants were only two days away from running out of oil, that the use of oil as a backup fuel led to incremental carbon emissions equivalent to 6 million cars, and that LNG supplies came from unstable source countries like Russia.

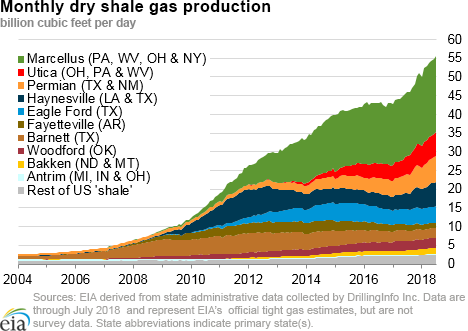

The graph below shows the growth of U.S. dry shale gas production. The largest wedge is the Marcellus. Ohio’s Utica is also nearby.

Clean Energy Focus

Eversource is investing in solar and wind generation, as well as expecting to source some electricity from Hydro-Quebec. In its annual report presentation, the company noted dramatic reductions in New England power generation emissions through the substitution of natural gas for oil and coal. In particular, in 2001, natural gas represented 23% of generation fuel; by 2018 it is 50%, displacing oil and coal. Despite generation growth over the time period, this resulted in a 29% reduction in carbon dioxide emissions, a 73% reduction in nitrogen oxide emissions (NOx), and a 98% reduction in sulfur oxide emissions (SOx).

First-Half 2018 Results

The company’s earnings per share (EPS) for the first half of 2018 was $1.61. This is divided as follows:

- Electric distribution – $0.65, or 40%

- Electric transmission – $0.69, or 43%

- Natural gas distribution – $0.20, or 12.5%

- Water distribution – $0.03, or 2%

- Parent and other – $0.04, or 2.5%

State Regulators

As a regulated utility, Eversource does not have direct competitors. However, it has oversight from and reporting responsibilities to public utility commissions and other state and federal regulators for every state in which it operates. In rate cases, it answers to and is subject to input from a wide variety of customer stakeholders.

Eversource’s Capital Expenditures

In the next four years, the company expects to make $7.1 billion of capital expenditures. For 2018, Eversource will spend $2.7 billion in capital, including $1.17 billion for electrical distribution and solar projects, $870 million for transmission, $420 million for natural gas distribution, $100 million for water projects, and $180 million for information technology and other projects.

Company Governance

Institutional Shareholder Services ranks Eversource’s overall governance as a 4, with sub-scores of Audit (2), Board (6), Shareholder Rights (7), and Compensation (1).

Short shares are 1.6% of floated shares. Less than half of a percent of outstanding stock is owned by insiders.

Eversource’s Financial and Stock Highlights

The company’s most recently reported trailing twelve-month earnings per share is $3.18, giving it a 3.25% return on assets and a 9.1% return on equity. Estimated 2018 earnings per share is $3.25. Estimated 2019 earnings per share is $3.47, resulting in a forward price-to-earnings ratio of 17.9.

Eversource’s beta is 0.19, meaning its price moves directionally with the market but to a far smaller degree than the market average.

ES data by YCharts

ES data by YCharts

At June 30, 2018, the company had $25.8 billion in liabilities and $37.2 billion in assets, giving a liability-to-asset ratio of 69%. Its market capitalization is $19.7 billion at an August 29th, 2018, stock closing price of $62.18 per share.

Eversource’s most recently reported operating cash flow is $1.8 billion and its levered free cash flow is $21.9 million. The company’s enterprise value (EV) is $34.2 billion.

The company’s 52-week price range is $52.76-66.15 per share, so its August 29th, 2018, closing price of $62.18 is 94% of its 1-year high. The 1-year target price is $63.50/share, putting its August 29th closing price at 98% of that level.

Eversource pays a dividend of $2.02/share, resulting in a dividend yield of 3.22%.

Overall, the company’s mean analyst rating is a 2.3 or “Buy,” leaning toward “Hold” from the fourteen analysts who follow it. This average includes five “Strong Buy” ratings and seven “Hold” ratings. Since April 2018, the last four ratings changes have been upgrades.

As of December 30, 2017, the top six institutional holders of Eversource’s stock were Vanguard (10.7%), BlackRock (7.95%), State Street (5.0%), Bank of New York (4.8%), Wellington (3.65%), and T. Rowe Price (3.5%). Many of these companies hold a wide distribution of stocks to accurately reflect the market in their index funds.

A Note on Valuation

The company’s book value per share of $35.58, approximately 60% of its current market price, indicates positive market sentiment.

Unlike a producing company such as EOG Resources (NYSE:EOG), the company’s market capitalization is less than its accounting-measured assets ($19.7 billion market capitalization compared to $37.2 billion in balance sheet assets.)

Positive and Negative Risks

Potential investors should consider state economic growth (New Hampshire, Connecticut, and Massachusetts) and state regulatory environments, including the ability to earn a markup on wholesale gas and electric purchases, as the factors most likely to affect Eversource.

Recommendations for Eversource

I recommend Eversource Energy to investors looking for dividends (3.22%), a stock price much less volatile than the overall market, a company investing in solar and wind projects, and one actively encouraging the substitution of lower-carbon natural gas for higher-carbon (and more expensive) heating oil in New England, aided by purchases from the nearby giant Marcellus gas field.

![]()

While you’re here, consider subscribing to Econ-Based Energy Investing, a Seeking Alpha Marketplace platform. Weekly in-depth articles provide you with recommendations for long energy investments.

Subscribers get actionable ideas, make decisions with larger industry context, and save time on research. My service focuses on publicly-traded small & mid-cap oil producers (by basin) & refiners (by area) drawing from a public energy space spanning more than 400 companies.

I’m an industry insider with +30 years’ experience working for & investing in energy companies. As you plan your research and investing strategies for the year, consider Econ-Based Energy Investing.

Disclosure: I am/we are long EOG.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment