The REIT space is flush with yield-rich opportunities for income investors to consider, but in this article, it’s actually one of the lower-yielding firms that I have come to find an interesting opportunity in LTC Properties (LTC), a smaller player in the Skilled Nursing and Assisted Living space with a market capitalization of $1.81 billion, and has a yield right now that’s just shy of 5%. Even in spite of this low payout though, the company’s prospects appear attractive and investors would be wise to consider a stake in the business.

A look at LTC

At its core, LTC focuses on two primary areas of operation: Skilled Nursing Facilities (also known as SNFs) and Assisted Living Facilities (aka ALFs). In short, the REIT, which was founded in 1992, provides real estate for companies that need to offer customers various medical and life management services. Conceptually, I can appreciate this type of company, not only because it offers necessary nursing and other related services to help those that need it, but also because the space is expected to grow as the population of the US continues to age.

*Taken from Omega Healthcare Investors

In the image above, for instance, you can see an analysis provided by one of LTC’s rivals, Omega Healthcare Investors (OHI). While current facilities are enough to meet near-term demand (the total industry occupancy rate for SNFs is estimated at 80.5%), this won’t always be the case. By 2030, the aging population will push demand higher such that current investments in SNFs will mean that 18% of the population that needs access to SNFs won’t be able to get it. That situation will rise to nearly one-third of interested parties by 2035. As a note, Omega did not provide estimates for ALFs because that space represents only 17% of its business, but it’s probable that a similar trend will exist there.

Obviously, the market will respond accordingly and a mix of higher prices and continued investment in the relevant facilities will lead, likely, to an oversupply of locations just like there is now. However, what this does illustrate is that the next several years can prove lucrative for LTC and other players like it, because as demand grows, so too can their firms. This future growth will come off of already attractive growth over the past few years.

*Created by Author

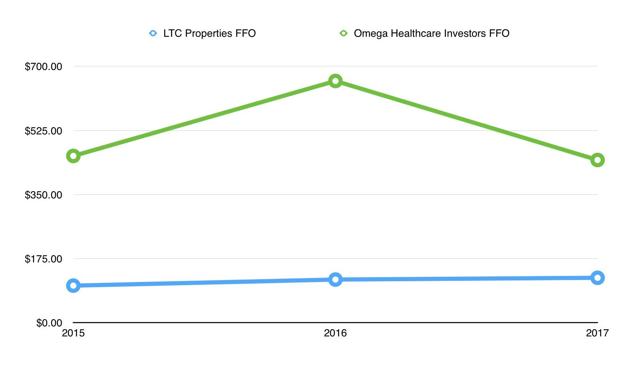

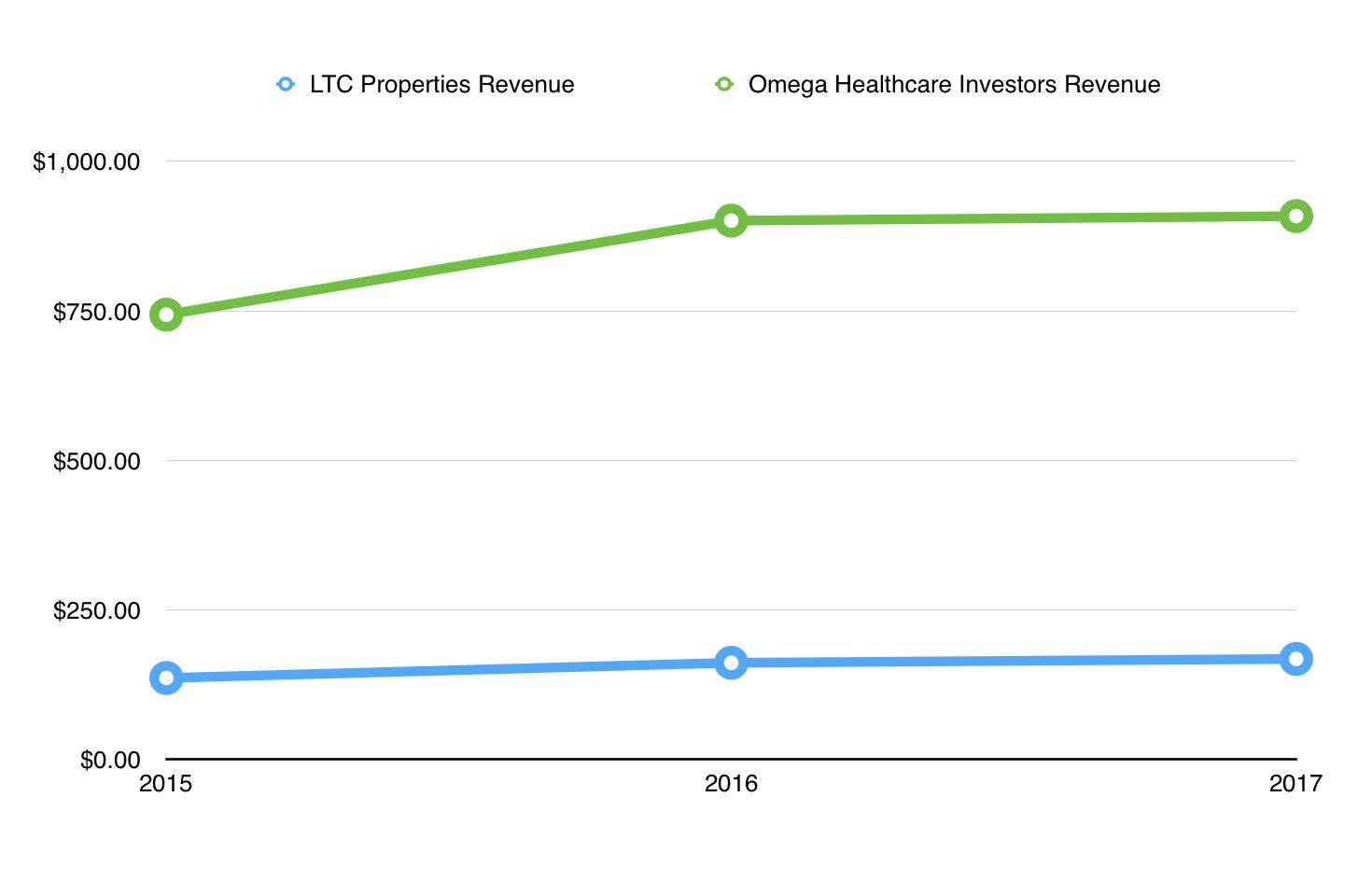

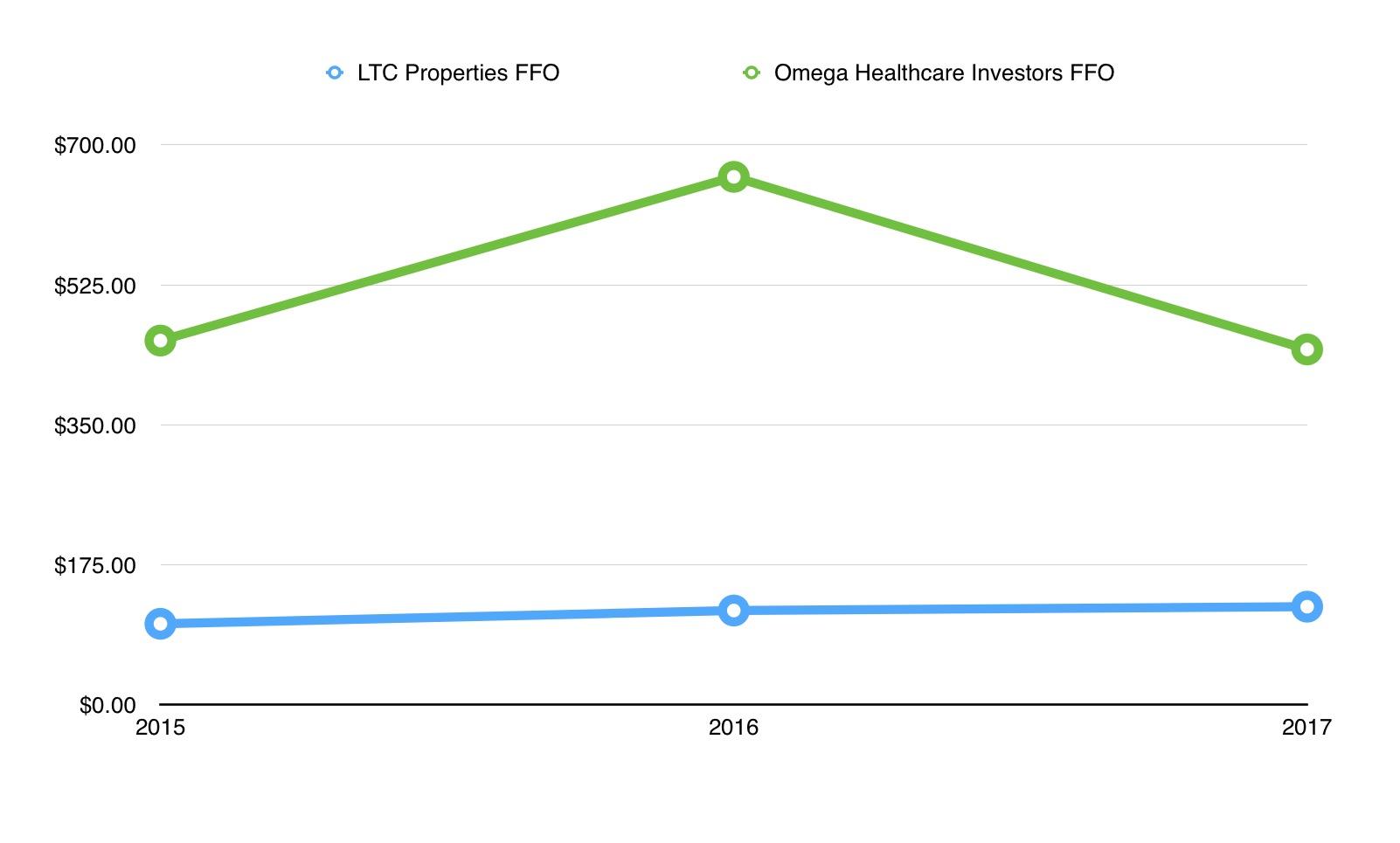

Take a look, for instance, at the graph above. In it, you’ll see that revenue for the three years ending in 2017 expanded by 23.4% from $136.20 million to $168.07 million. This is actually marginally better than the 22.2% revenue growth posted by Omega, but in its case, sales grew from $743.62 million to $908.39 million. It’s not only sales growth where LTC’s management team has excelled, but it’s also in relation to cash flow margins as well. As the graph below shows, FFO (funds from operations) reported by LTC has expanded nicely, growing from $101.24 million in 2015 to $122.65 million last year.

*Created by Author

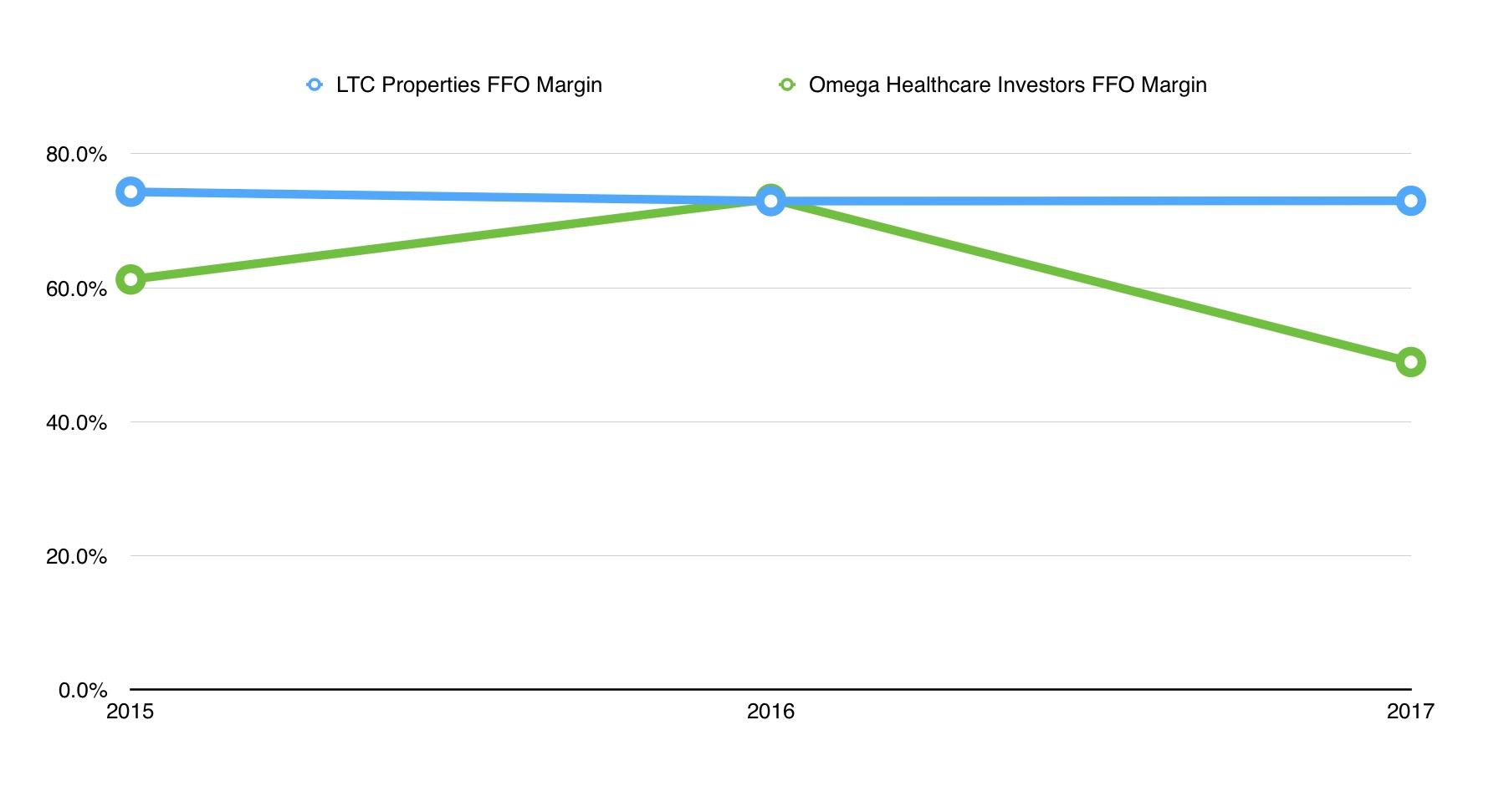

What is probably most telling from this though is the FFO margin (FFO relative to sales). For LTC, this figure has stayed fairly consistent for the past three years between 72.9% in 2016 and 74.3% in 2015. Last year, the figure was a respectable 73%. To put this in perspective, Omega has also posted attractive measures, but as the graph illustrates, only one of the three years covered has a comparable margin compared to LTC.

*Created by Author

Getting into occupancy figures, the picture is a little more complex. The SNF industry as a whole had an occupancy rate last year of 80.5%, which is actually higher than the 78.3% reported by LTC. That said, its ALFs are performing nicely, with occupancy rates of around 84.4%. Omega, for its entire portfolio, has an occupancy rate of 82.2%, positioning it as a solid player, but if you average out LTC’s portfolio, you end up with a similar reading.

*Taken from LTC Properties

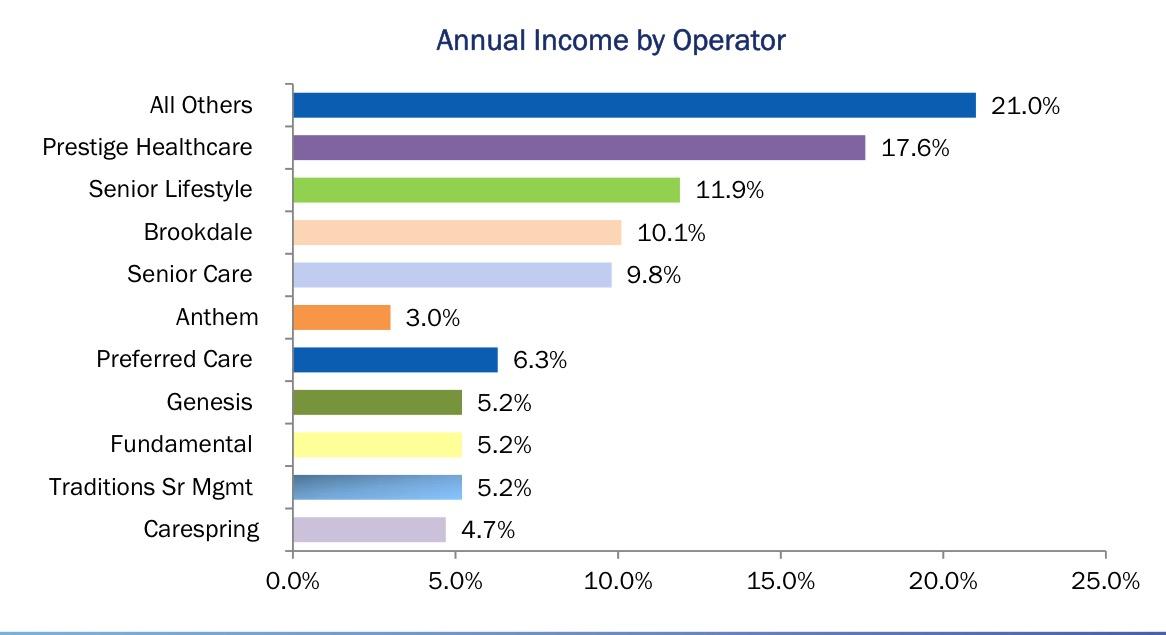

One thing I am always cognizant of when it comes to any landlord-like relationship is the concentration of key customers. As we found out with Omega earlier this year, even one problem customer can throw the business for a loop. This is a particularly risky problem for LTC because its largest customer, as is illustrated above, represents 17.6% of the firm’s annual income. In all, its five largest customers account for 55.7% of LTC’s revenue.

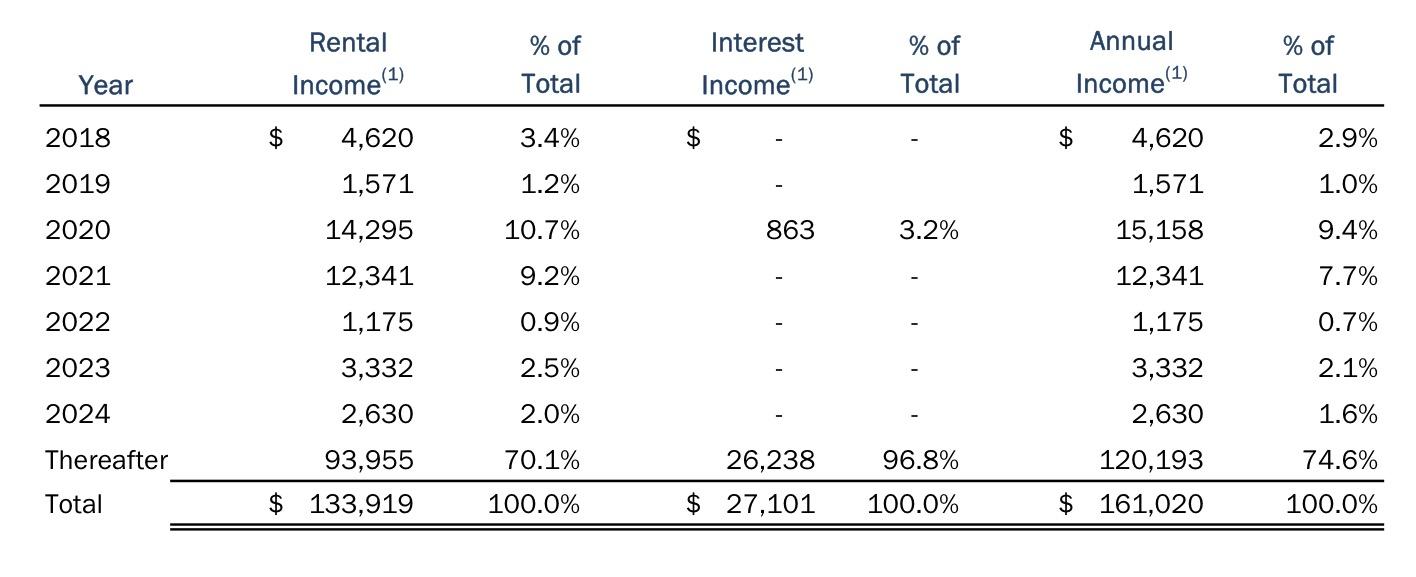

This brings me to one more piece of news that investors should be aware of. As the image below shows, there are some near-term contract maturities. Between this year and 2021, customers representing 24.5% of rental income will either see their contracts expire or they will have to renew them with LTC. This creates third-party risk for the REIT that isn’t there, on the same scale, as it is for Omega. Over the same four-year period, contracts representing only 3.7% of Omega’s income will expire. While LTC will see 70.1% of its rental income and 74.61% of its total income roll off after 2024, Omega’s figure for post-2024 is 82.5%, meaning that it’s more protected from near-term clients not renewing their contracts than LTC is.

*Taken from LTC Properties

This isn’t to say that the market should definitely favor Omega over LTC though. Certainly, it looks as though Omega, operationally, is the more secure of the two businesses, but we should also consider differences in payout. In the first two quarters of 2018, LTC generated FFO per share of $1.50, and yet it paid out $1.14 per share in the form of distributions for a distribution payout ratio of 0.76. Omega’s $1.32 distribution from $1.46 per share in FFO implies a higher payout of about 0.90. What this means is that LTC could, in theory, keep its distribution where it is easier than Omega could in the event of a downturn. Of course, differences in required maintenance capex could affect this payout ability to some degree, but with LTC’s debt/EBITDA ratio at 4.3 compared to Omega’s 5.2, LTC could technically borrow more easily to keep its distribution high or to even raise it.

Takeaway

From my experience following and writing about Omega, I must say that it’s a company that I like and that I’m impressed by. That said, LTC looks equally interesting in my book. Sure, the firm’s 5% yield is small compared to Omega’s 8.1%, but growth in recent years has been impressive, occupancy rates are hovering around where they should (they could be a bit higher), and the business isn’t paying out so much of its FFO that management is strapped. This suggests to me that investors who like the SNF and/or ALF space, but for some reason who already own enough of Omega or don’t want to buy it, could turn to LTC as an interesting alternative.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment