![]()

Since the end of the Great Recession, trillions upon trillions of investor dollars have piled into large-cap US stocks, particularly large-cap dividend stocks, such as the Dividend Aristocrats. This movement of money has been driven by the search for yield, thanks to the “ZIRP” policy practiced by the Federal Reserve until very recently. I believe that this has resulted in a moderate overvaluation of dividend-paying large-cap stocks. As such, I like to occasionally add dividend-paying small-cap companies to my income portfolio in order to help diversify against the overvaluation risk that I believe is inherent in large-cap dividend-paying equities at current prices.

One such company that has recently crossed my radar screen is Village Super Market, Inc. (VLGEA), a grocery-store operator with a market capitalization of around $425 million. Founded in 1937, Village Super Market operates 29 “ShopRite” grocery stores, primarily in the New Jersey area. The chart below is from the company’s 2015 Annual Report but is still largely accurate in terms of the distribution of the stores.

Source: Village Super Market 2015 Annual Report

Given the fact that it only has 29 stores, Village Super Market competes with larger supermarket chains by participating in the Wakefern Food Corp., the largest retailer-owned co-op in the United States. This co-op, consisting of 50 members which together operate over 340 supermarkets, allows members to use the “ShopRite”, “thefreshgrocer”, and “PriceRite” brands. It also handles loyalty programs, advertising and other ancillary services for its members, for which it is paid. This helps to promote economies of scale, and the fact that the co-op is member-owned means that any profit earned by Wakefern is distributed back to its members in the form a “patronage dividend”. This reduces costs even further for Wakefern members.

However, membership in Wakefern does come with a few restrictions. Members have to source at least 85% of the portion of their inventory which Wakefern can provide from Wakefern. This can potentially lessen Village Super Market’s flexibility in choosing suppliers, but I believe the fact that Wakefern ultimately refunds any profits it makes back to its members probably makes it competitive relative to any alternative suppliers. A more troubling limitation, from my perspective, is the fact that members of Wakefern which are acquired without Wakefern’s consent by a company not meeting Wakefern’s definition of a “qualified successor” (i.e., a small- to mid-size locally-oriented company that either is or commits to becoming a member of Wakefern) are required to compensate Wakefern for the “profit contribution shortfall” which would occur if the member were to stop doing business with Wakefern. This hurdle could prevent a nationally-oriented chain of supermarkets from “gobbling up” Village Super Market and likely paying investors a sizable control premium in exchange for the privilege of doing so.

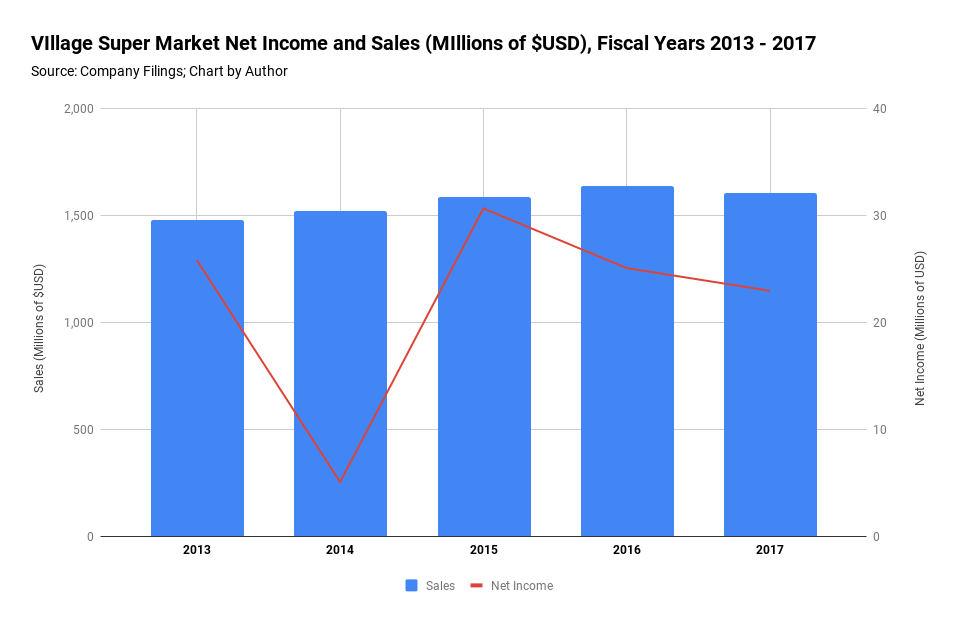

Given the fact that same-store sales essentially flatlined between fiscal years 2016 and 2017, investors should not delude themselves into thinking that Village Super Market is on a path to rapid growth. The company’s sales appear to have begun to stagnate around 2016, and net income has bounced around from $20 to $30 million per year, with 2014 being a notable exception.

The 13 weeks ending on April 28, 2018, show an improvement in net income, which rose from $6 million for the same period in 2017 to $6.5 million this year. However, this improvement seems to have been driven by a reduction in the company’s income tax liabilities, not an improvement in the company’s operations.

The 13 weeks ending on April 28, 2018, show an improvement in net income, which rose from $6 million for the same period in 2017 to $6.5 million this year. However, this improvement seems to have been driven by a reduction in the company’s income tax liabilities, not an improvement in the company’s operations.

Dividends

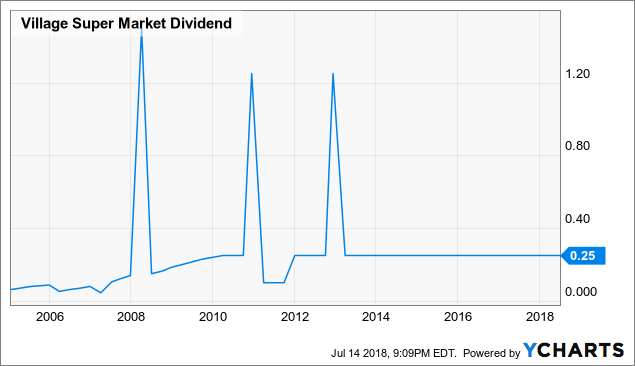

Village Super Market’s dividend history leaves much to be desired in terms of dividend growth, although the sporadic special dividend payments have perhaps compensated shareholders for the lack of long-term dividend growth from the late 2000s onward. The company also yields around 3.4%, a reasonably generous payout in today’s interest rate environment. The temporary dividend cut shown in 2011 on the chart below was, in part, the result of a deliberate decision on the part of management to move the dividend payments for early 2011 into 2010, in order to help investors minimize their 2011 tax liability due to an anticipated increase in dividend taxation rates.

VLGEA Dividend data by YCharts

VLGEA Dividend data by YCharts

Debt

Village’s balance sheet is in very good shape. According to its most recent quarterly SEC filing, the company has about $42 million of long-term debt, compared with almost $80 million of cash and cash equivalents on hand. As such, I am very confident that the company’s cost of debt service will not pose a risk to the sustainability of the dividend in the foreseeable future.

Risks

The supermarket industry is a notoriously low-margin business. Village Super Market is no different, with net income only amounting to 1.43 percent of sales in 2017. Such razor-thin margins leave little room for error. Given the fact that low margins are inherent in the industry in which Village Super Market competes, the primary way for the company to grow sales, profits, and ultimately dividends is to either grow sales, grow the number of stores it operates, or both. Since the number of stores has largely flatlined over the years, as have revenues over the past year, it is difficult for me to see any meaningful earnings growth “in the cards” for Village in the immediate future. This is particularly true if food price inflation picks up, and competitive conditions force Village Super Market to “eat” the costs of those price hikes rather than passing them on to customers.

Another factor which makes an investment in Village Super Market less attractive to me is the restrictive covenants with which the company must comply in order to remain a member of the Wakefern co-op. Namely, any “change of control” event (i.e., an acquisition) that occurs without Wakefern’s approval could result in Village Super Market having to compensate Wakefern for the “annual profit contribution shortfall” if the new owners decide to change suppliers. I am not a fan of this provision because it reduces the likelihood of a potential suitor being interested in acquiring Village Super Market.

The final major risk to Village Super Market’s investment prospects comes from its highly unionized workforce. According to the company, approximately 91% of its employees are covered by collective bargaining agreements. If inflation picks up, it is likely that the seven unions which represent various groups of Village Super Market employees will demand increased wage concessions at precisely the same time that Village’s margins would shrink due to increased costs for goods sold.

Closing Thoughts

Although Village Super Market’s three percent dividend yield and tiny market capitalization kindled my hopes that I had found an underappreciated investment opportunity, consideration of the industry in which the company operates, the lack of regular dividend growth, and the constraints put on the company by its relationship with Wakefern have dampened my enthusiasm. The small size of companies such as Village Super Market can make them ideal acquisition opportunities, which in turn can lead to quick capital gains for shareholders if a significant enough control premium is offered. Wakefern’s restrictions on the circumstances under which a member can sell itself without potentially incurring financial sanctions reduce the likelihood of such an event occurring. The grocery industry is also an extremely low-margin industry, and I feel that sustained food-price inflation in the medium- to long-term could pressure Village Super Market, both in terms of cost of goods sold and in terms of the concessions it is forced to make to its relatively well-unionized workforce. As such, I am not sure that future returns on Village Super Market will be sufficient to compensate investors who get in at current prices for the risks they are taking.

I think income investors would want some measure of exposure to the grocery industry are better off looking into shopping-center REITs, such as Regency Centers (REG) and Weingarten Realty Trust (WRI), which lease space to grocery operators and offer similar or higher income yields to Village Super Market.

Disclaimer: Use my work as a starting point for your own due diligence, not as a substitute. All investments involve the risk of loss of income as well as the principal. Consider consulting with an investment adviser before making any investment. I am not a tax professional or investment adviser. Please consider consulting with a tax professional before making any investment. Author-generated charts are subject to error due to discrepancies in source data or securities being listed on multiple international markets.

Like what you read? Click the “Follow” button at the top of this page!

Disclosure: I am/we are long WRI.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment