Tenable (TENB) is the latest cybersecurity company to go public this year following the highly anticipated offerings from Zscaler (ZS) and Carbon Black (CBLK). I believe all of these companies are great pure plays in the cybersecurity industry and their unique SaaS platform is a competitive advantage over their legacy counterparts. I recent wrote an article on why CBLK is a great investment since their price has settled since their hot IPO.

TENB offers cloud-based vulnerability management services which helps protect an enterprises assets such as network containers and web applications. Their SaaS based approach is favorable compared to legacy players who still provide hardware offerings. TENB continues to grow and take market share, and their software offerings deserve a premium trading multiple.

TENB Price data by YCharts

Brief Overview

TENB claims to be “the first and only provider of solutions for a new category of cybersecurity that we call Cyber Exposure” (Source: Company Filings). They define Cyber Exposure as an area for managing and measuring cybersecurity risk, focusing on vulnerability assessment and management market. Essentially TENB provides enterprises an offering to help quantify how much damage would be caused by a security breach. This information is very valuable for enterprises as security breaches seem to make the headlines at least once a week.

The shift to a more modern infrastructure has included the transformation from hardware to a more software focused architecture. These software offerings from an array of cybersecurity companies are becoming easier to integrate and can essentially sit on top of any commodity hardware. This brings the challenge of determine where an enterprise has vulnerabilities and how expense these vulnerabilities could become if breached. Let’s face it, hackers are getting smarter and are finding more ways to breach into an enterprise than traditional security products are used to.

The ability for an enterprise to maintain visibility and control over the security of their assets is now essential. Enterprises are also adapting to newer technologies, such as the Internet of Things, containers, new business models, and more. All of these require increased efficient security and control measures. TENB is looking to fill what they call the “Cyber Exposure Gap”, or an enterprises’ inability to see “the breadth of the modern attack surface and analyze the level of cyber exposure” (Source: Company Filings).

Tenable.io is TENB’s SaaS offering which manages and measures cyber exposure across an enterprises’ IT assets. These assets typically include networking infrastructure, desktops, on-premise servers, containers, web applications and many more. This offering will essentially tell an enterprises where they are vulnerable and the best way to manage this vulnerability.

TENB also offers SecurityCenter which is specifically built to manage and measure cyber exposure and can be run on-premise, in the cloud, or in a hybrid environment. The main difference between SecurityCenter and Tenable.io is that Tenable.io can only be provided through a SaaS offering.

Either way, both of these offerings gives an enterprise the ability to manage their assets and vulnerability, through running tests and analytics. This is an essential offering for all enterprises to seriously consider, especially as IT assets are become more widespread. Think of the average employee owning a cell phone and a company provided laptop. That enterprise now has to make sure all business-related activity done on either the phone, laptop, or other mobile device is secure and not vulnerable to an attack. This is not an easy task, yet is essential for today’s modern enterprise to succeed.

Financial Results

At the end of F17, TENB has over 24,000 global customer including over 4,400 enterprise platform customers. TENB defines an enterprise platform customer as one who has a current license agreement in excess of $5,000 during the year. TENB’s customer have a global span reaching 160 countries including government agencies. Also, over 53% of the Fortune 500 and 29% of the Global 2000 organizations have paid versions of TENB’s products. This includes enterprise platform customers in 30 of the Fortune 500 and 58 of the Global 2000 organizations (Source: Company Filings).

Source: Company Filings

Source: Company Filings

Revenue grew 51% and 33% in F17 and F16, respectively. That’s an impressive 18 percentage points acceleration in revenue growth yoy, a very impressive feat for a company who generated nearly $200 million in revenue last year. Through Q1, which ended in March, TENB demonstrated a 46% top line growth. Billings have remain impressive, with growth rates of 49% and 37% in F17 and F16, respectively. Billings also grew 47% in Q1. It is very impressive to see Billings grow at near identical rates as revenues, thus demonstrating the company’s ability to continue generating future revenue streams. Source: Company Filings

Source: Company Filings

Non-GAAP operating margins have remained relatively consistent, yet are showing signs of improvement. Non-GAAP operating margin was (27%) in F16, which improved to (17%) in F17. However, TENB had a (17%) margin in Q1’17 which slightly decreased to (20%) in Q1’18. The main difference here was stock-based compensation, likely a side effect from the company preparing to go public this year.

Valuation

Valuation is always tricky with IPO’s since their shares tend to trade with increased volatility as early insiders are looking to capitalize on their presume large capital gains.

TENB originally priced 10.9 million shares at $23 this past Wednesday, which quickly jumped to close at $30.25, up nearly 32% on the first day of trading. At Friday’s close, TENB closed at $30.50, a decent 33% gain for the opening few days.

Recent cybersecurity IPO’s ZS and CBLK also recorded significant share gains in the opening days. The more impressive ZS opened at $16 and closed up 106% for the day. This is more of an anomaly as they have traded over 20x revenue for a large portion of their public life, though they have recently “settled” down to mid-teens. This is another story to be discussed a different day. CBLK had a similar, though not as impressive story. They continue to trade at a revenue just shy of 10x.

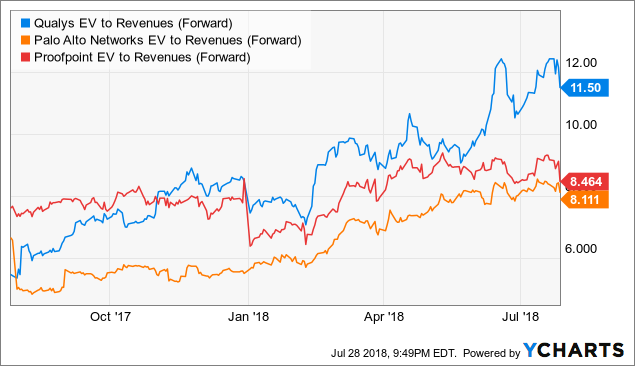

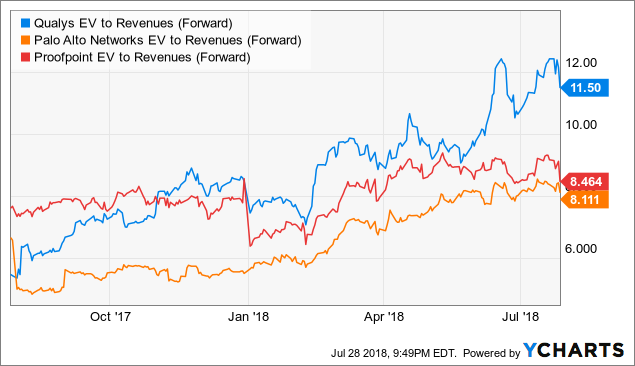

The below peer group includes some top cybersecurity names in the industry, including Qualys (QLYS), Palo Alto (PANW), and Proofpoint (PFPT). All of these names are relatively high revenue multiple names with significant potential to disrupt and lead their respective industries. QLYS is especially a close name to follow because they specialize in vulnerability management. In fact, they have a product tool named Vulnerability Management. QLYS and TENB are likely to become intense competitors as this industry further develops.

QLYS EV to Revenues (Forward) data by YCharts

QLYS EV to Revenues (Forward) data by YCharts

TENB has a similar potential as these companies and because of their SaaS based operations, should be valued at a premium revenue multiple. As a reminder, TENB had $187.7 million of revenue in F17 and recorded $59.1 million through Q1 (a 46% growth compared to last year). Rather than assuming a run-rate revenue based on Q1’18 (because this would essentially flatline sequential growth and give TENB no credit for annual growth), I will simply use the 46% quarterly growth rate for the remainder of the year.

At a 46% annualized growth rate, F18 revenues would be $274 million. As of this past Friday, TENB had 91.1 million shares outstanding. Using Friday’s closing price of $30.50, TENB has a current market cap of $2.78 billion and including net cash of $26.4 million, TENB has an EV of ~$2.76 billion, giving them a current EV/forward revenue multiple of ~10x.

Because of the close competitiveness between TENB and QLYS, if we assume TENB trades at a 11.5x revenue multiple they would trade around $35, a 14% upside to Friday’s close. For now, this is a bit of a stretch because TENB is a new public company and will continue to trade with volatility as investor look to right size their holdings.

Yes, this is an expensive multiple based on the broad market, however, TENB’s SaaS offerings are highly competitive to QLYS, who is considered the market leader in the vulnerability management market. TENB trades at ~1.5 turn discount to the market leader. Both of these companies offer SaaS based platforms which enable them to have a more predictable revenue stream with greater margins and ability to generate future cash flows.

For now, TENB is a great stock for those who got in at the IPO price. If I had shares I would absolutely hold onto them a look for any further divergence between the multiples of TENB and QLYS as signs to buy more. If I didn’t have shares, I would slowly build up a position as TENB inevitably experiences post-IPO volatility dips.

Disclosure: I/we have no positions in any stocks mentioned, but may initiate a long position in TENB over the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment