Despite a steep tradeoff such as interest rate sensitivity, a compelling argument can be made to invest in long-duration bonds. With exposure to high credit quality and long maturities, investors can earn a respectable yield of 4-6% without having to take on highly leveraged junk bond CEFs. Furthermore, there are plenty of low-cost ETF options out there (i.e. Vanguard, iShares, etc.), so you don’t have to worry about fees eroding your returns.

The challenge, as we know, is rising bond yields. It can be hard to justify long-term bonds if you expect the Fed to continue raising short-term rates the yield curve to potentially invert. Notwithstanding this big hurdle, I wanted to explore some bond fund options and how to protect yourself from rising yields and an uncertain macroeconomic future.

Why You Should Consider Long-term Bonds

(Source: Vanguard Funds)

With still low interest rates, it can be very difficult to earn an acceptable yield from a traditional fixed income portfolio. Perhaps that’s why equities and closed-end funds have done so well in the last 9 years. The historically low interest rates have encouraged investors to eschew fixed income in favor of equities and yield chasing to earn income. There are a few reasons to opt for long-term bonds:

- You want to avoid the risk of investing in equities;

- You want the stability of bonds with hedges against rising yields;

- And seek to create a diversified income stream.

With these in mind, it can make sense to consider an ETF such as the Vanguard Long-term Corporate Bond Fund (VCLT). While I would like to see more sector diversification, the fund is one of the largest bond funds in terms of assets and is invested in companies with high credit quality.

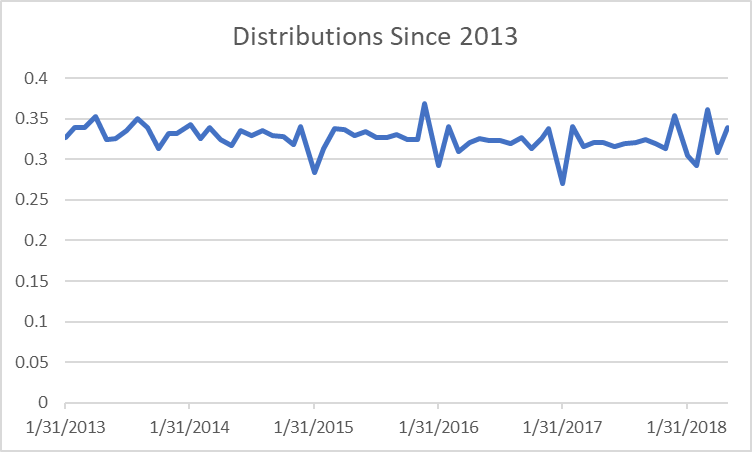

Investing For Income

(Source: Original Image – Data from Yahoo Finance)

For income investors such as retirees, high-quality corporate bonds can make a lot of sense. If you’re relying on your portfolio for living expenses, you should want to minimize risk of default. While extending the duration of bonds will expose your portfolio to greater interest rate sensitivity, the underlying securities will at least be more resilient to credit risk. The fund is made of bonds rated Baa and above and is diversified across 1,800 bonds. Furthermore, you can see that VCLT’s historical distributions have been very stable. Granted it has offered a relatively modest 12-month trailing yield of 4.18%, the low payout is a small sacrifice if you seek capital preservation. There is also the benefit of tax-efficiency as the fund managers typically pay out long-term capital gains at the end of the year.

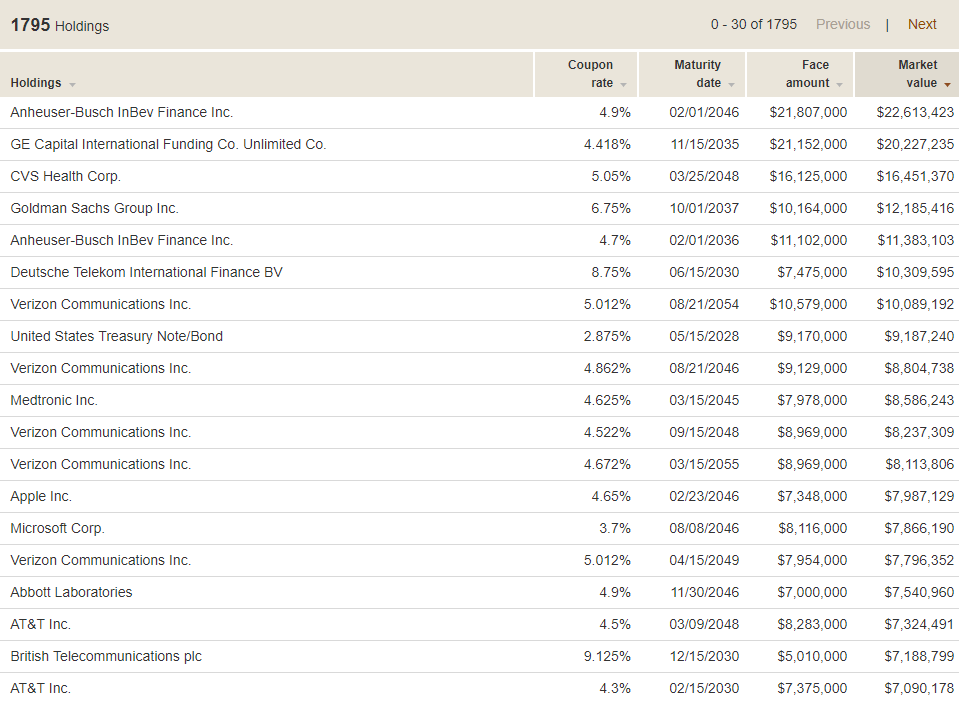

(Source: 2018 Semi-Annual Report)

Compared to CEFs that generally charge high expense ratios, this ETF is very low cost. While that can be beneficial to shareholders concerned about fees eroding performance, it can hinder the fund if it cannot generate sufficient Investment Income to cover the monthly distributions. That hasn’t been an issue with this Vanguard fund as they have had the distribution well covered and have a positive undistributed net investment income (UNII) balance.

Granted the underlying bonds are of high credit quality and boast names such as Apple (AAPL), Verizon (VZ), and AT&T (T), the fund is not exempt from default risk. Furthermore, there is growing concern about a U.S. recession with a potential trade war, rising inflation, and elevated debt levels. Looking back at charts of long-term bonds in the wake of the last financial crisis, even high quality fixed income experienced significant drawdowns. The longer the duration, the more potential those drawdowns are going forward. Compared to more risky fixed income investments like bank loans, however, VCLT can shield investors from losses in a diversified income portfolio.

(Source: Vanguard Funds)

So, What Hedges Are Most Effective?

(Source: Yahoo Finance)

Perhaps because of their growth potential in being converted to equities, convertible bonds have been touted as a good pairing to corporate bonds. The charts, however, beg to differ. While the above sample size is only six years, I think there were enough significant events affecting fixed income to demonstrate my point. After notable events such as the taper tantrum in 2013 and increase in defaults in 2016, you can see that convertibles have had high correlation to long-term bonds. Except for brief periods in the last two years, the asset class hasn’t really provided any diversification benefits. Adding equity REITs would have added some capital growth but no diversification because of the same issue.

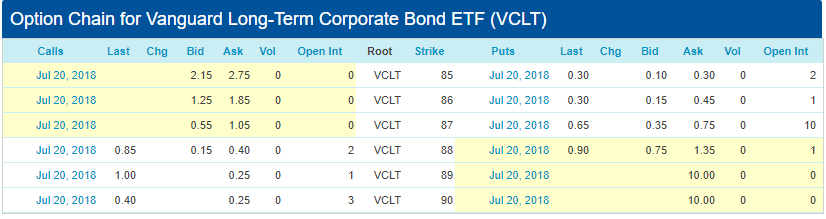

As such, a very simple solution is to purchase a put option either a treasury with similar duration (VGLT) or on the ETF itself. According to VCLT’s option chain, it is very cheap to purchase insurance with monthly put options costing $.30-.75 per share. While you have to pay for the privilege to hedge against rising yields, based on the correlations between fixed income asset classes, it seems that this is the most effective option to protect your downside risk.

(Source: NASDAQ Option Chain)

Conclusion

In summation, investors should consider high-quality bonds with extended duration if they can hedge their bets. With put options, investors need not worry about rising bond yields eating away at their principal investment. Furthermore, long-term bonds present an opportunity for conservative buy and hold investors to pick up a 4% yield without taking on equity risk.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment