With the advancement of healthcare technology, there is abundant opportunity for medical science companies to grow as products are designed and developed with each passing year. Despite a dividend streak of 46 years, Becton, Dickinson and Company (BDX) has made some large moves that has put the company in a position to generate excellent growth in an industry that will only see worldwide demand for medical solutions grow larger in the years to come.

source: Becton, Dickinson and Company

A New Look Becton, Dickinson

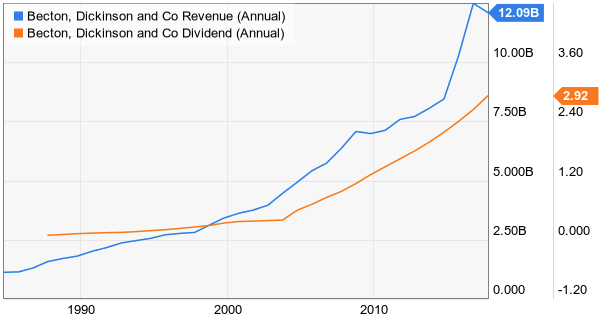

Becton Dickinson sports a storied history that features excellent top line growth, and a dividend streak that currently sits at 46 years.

source: Ycharts

source: Ycharts

With how much has changed over the past several years, it makes more sense to breakdown what the new Becton, Dickinson looks like rather than hone in on the past. Over the past four years, Becton Dickinson has dramatically shifted the structure of its company with two major deals. The first taking place in 2014 for CareFusion, worth $12.2B. The other deal being the 2017 deal to acquire C.R. Bard for $24B.

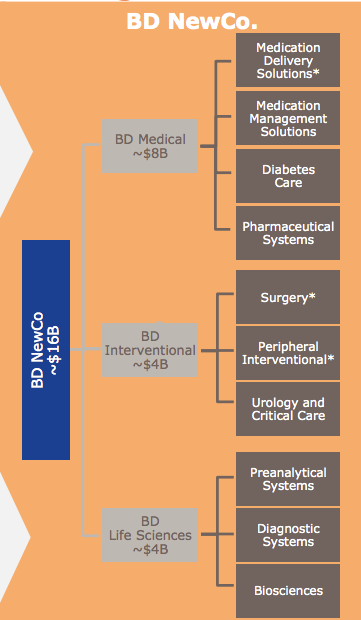

These changes shifted Becton, Dickinson from a product based company to a healthcare technology company with a broader depth of offerings to the healthcare industry. Today, the company is broken up into three segments.

source: Becton, Dickinson and Company

source: Becton, Dickinson and Company

With 2018 being the flagship year of the “new” Becton, Dickinson, there is a lot to be excited about. The company is projecting approximately $16B in revenues broken up as roughly two parts Medical to one part each of Life Science and Interventional. The company is a global enterprise with a US to International revenue split of approximately 55-45.

Status Of Dividend & Debt

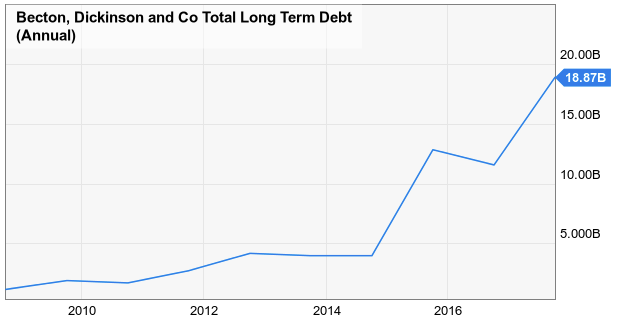

As previously noted, Becton, Dickinson has a storied dividend history that includes 46 years of consecutive increases. The dividend has grown at a snappy CAGR of 11.6% over the past 10 years. However, the most recent dividend increase was for only 2.7%. This is because Becton, Dickinson has taken on a lot of debt in order to get the Bard deal done.

The Bard deal tacked on approximately $10B of new debt onto the balance sheet, and pushed leverage ratios through the roof. With the closing of the Bard deal, the balance sheet was sitting at approximately 4.7X LTM adjusted EBITDA. Moody’s has since downgraded Becton, Dickinson to a credit rating of Ba1 or “junk bond” status.

source: Ycharts

source: Ycharts

Management has a goal to pay down the balance sheet enough to get its debt load to less than 3X LTM adjusted EBITDA by 2020. The $3 annual dividend is well covered by cash flows (operating cash flows projected at approximately $13 per share this year), and is a priority for management so the dividend is easily safe. With that said, the dividend will likely grow at a rate close to inflation for a few more years before moving higher to faster growth. Becton, Dickinson needs to dig itself out of this highly leveraged balance sheet mess as soon as possible.

Growth Will Be Abundent

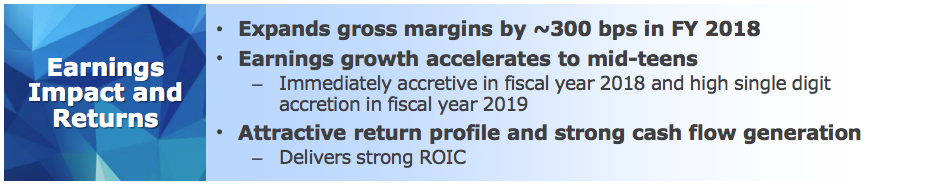

The good news, is that the company is set to enjoy a very strong growth trajectory. Management is projecting both an increase in revenue growth and margins which will only provide a further boost to cash flows and earnings.

source: Becton, Dickinson and Company

source: Becton, Dickinson and Company

The exact results of the newly structured company are still unknown to some degree. Management has already raised fiscal guidance after just its first quarter reporting under the new structure.

There are a lot of growth catalysts to like for Becton, Dickinson and the company seems to have a solid grasp on both understanding and benefiting from them.

source: Becton, Dickinson and Company

source: Becton, Dickinson and Company

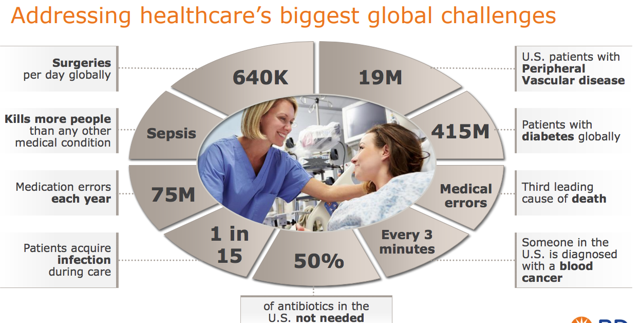

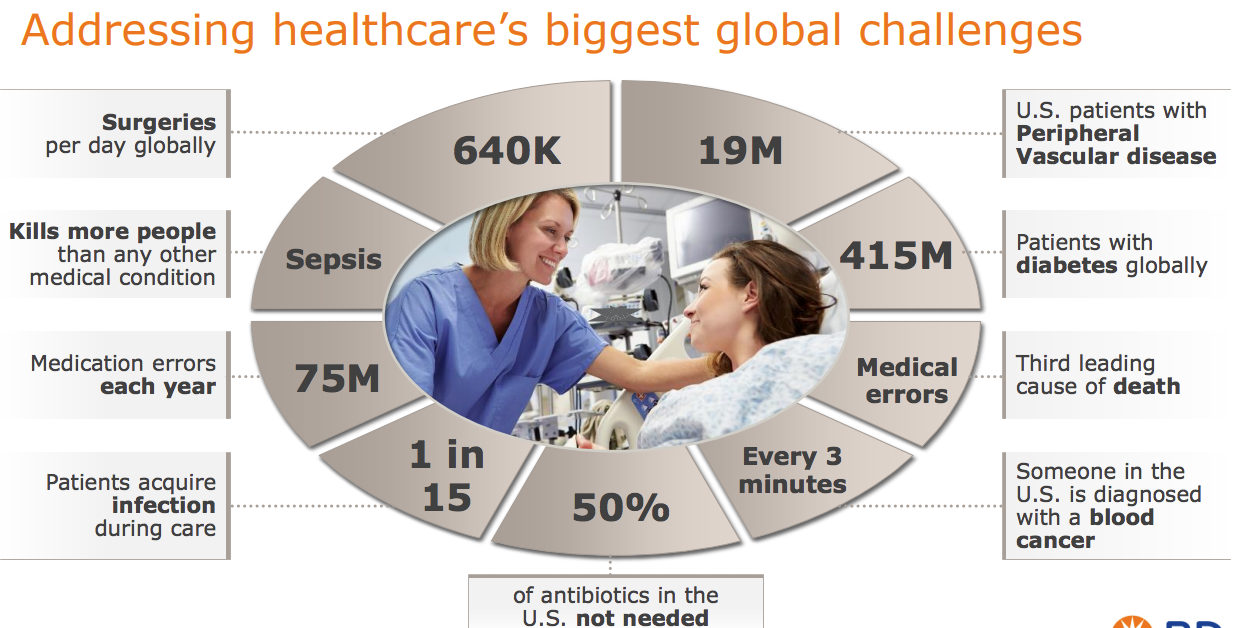

Many of Becton, Dickinson’s products and services are aimed at improving efficiency within the healthcare industry. Every year thousands of people die from in hospital complications such as Sepsis and hospital acquired infections. Becton, Dickinson designs products and medication delivery systems that helps prevent these types of deaths by treating high risk areas and applications such as surgical wounds, stents, catheters and more.

Meanwhile, Diabetes is one of the most expensive diseases in the world because of its prevalence throughout the globe.

source: Statista

source: Statista

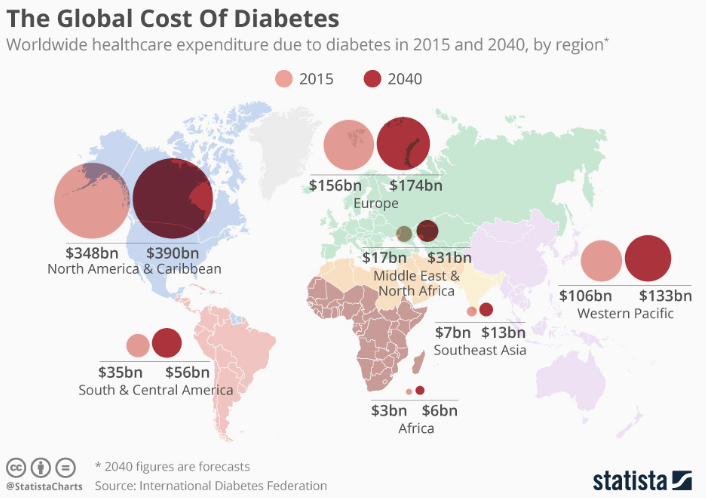

Becton, Dickinson manufactures various diabetes treatment products from syringes to insulin management systems. Unfortunately Diabetes is going to be a long term problem with global care costs projected to increase through 2040. Developed countries remain very reliant on processed foods and sugary drinks which over time can cause the development of Type II Diabetes in adults. This epidemic will cause demand for these types of product to increase between now and 2040.

Year to date, the largest jumps in revenue growth has come from sales of medical delivery solutions, pharmaceutical systems, diagnostic systems, and peripheral intervention products.

Becton, Dickinson has a presence in virtually all industries because of its strong presence in high amounts of in-hospital applications. That is why its biggest opportunity for growth is in the globalization of Becton, Dickinson. Emerging markets and developing health care networks are key for Becton, Dickinson.

source: Becton, Dickinson and Company

source: Becton, Dickinson and Company

China is the largest example of this. Despite China accounting for 20% of the entire global population, the company maintains a presence there of only about $1B in sales. Year to date, sales in China are already up 36.1%. Other emerging markets such as the continent of Africa are only $2.5B. Year to date, sales in these markets are up 25.1%. In all, international sales are up 26% year to date. Bard had a strong international channel presence, and pipeline. This may end up being Becton, Dickinson’s largest benefit from the acquisition when we look back years from now.

Valuation

With such an uptick in growth, the market is viewing Becton, Dickinson as a growth stock. The company raised guidance off of a strong Q2 in May, and is currently pushing up against 52 week highs.

source: Ycharts

source: Ycharts

Becton, Dickinson is anticipating earning approximately $11 per share this year, which would place the stock at a valuation of approximately 22X earnings. While not a bargain multiple, the valuation is actually quite reasonable for a company that is expecting earnings growth rates in the mid teens over the next several years. The dividend yield is a tad lower than its decade average (1.23% versus average of 1.77%). But if you buy Becton, Dickinson, you are not in it for the dividend income. Despite the dividend champion label, this is a total returns play.

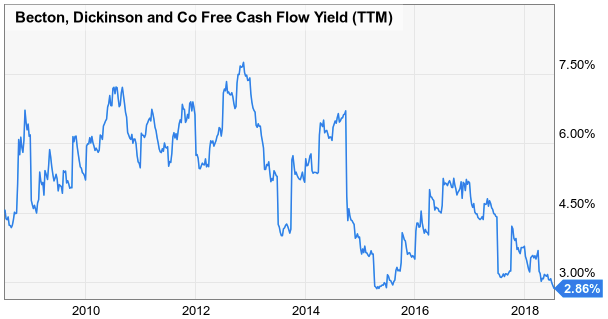

If I plot free cash flow yield, we get another sense of value. I cannot graph it because the company’s new structure would throw the graph out of whack. However, I can calculate it and compare it to historical data. If we take expected 2018 operating cash of $3.5B and subtract the $900M in anticipated 2018 CAPEX, our expected 2018 FCF of $2.6B would yield just a hair under 4%.

source: Ycharts

source: Ycharts

Looking at how much the “old” Becton, Dickinson yielded on FCF, we can see that the current yield of 4% is the lowest in a year, but isn’t necessarily a great value at this point in time. Again, I must emphasize that the “picture” will change over the next couple of years because management is getting a pulse on the performance of the new businesses, while expecting several hundred million of synergies to take place in the next few years. These savings will help boost profitability even further.

To sum up the valuation of shares, I have to say that the stock is certainly no bargain at 52 week highs. Yet, the valuation isn’t outrageous considering the growth you are getting. If an investor wanted to buy here and forget about it for five years, you still will likely have made a lot of money down the road. On the other hand, I like to “get a deal” because I prefer a margin of safety. I currently wouldn’t expect Becton, Dickinson to drop very far unless we see some serious market movement to the downside. If shares were to fall to 19X earnings, I would see that as a pretty lucrative opportunity. Remember – despite the company’s growth upside here, the balance sheet is loaded so the company will be on a cash diet while it pays off debt. This means limited dividend growth, and probably little to no share buybacks.

Wrapping Up

Healthcare is a fantastic investment opportunity for investors because the sad reality is that we live in a world where illness and disease necessitates continual investments into healthcare. Becton, Dickinson has a storied 46 year dividend growth history as a healthcare blue chip, whose recent “make over” has the company poised to grow earnings at a double digit rate moving forward. A newer, more globalized presence in hospital care technology, diabetes, diagnostics, and medicine delivery has the company in a lucrative position in the coming decades.

While the debt load is really high, the company’s revenue growth and strong cash flow generation will enable it to dig out over the next few years. We still don’t know the full picture as Becton, Dickinson continues to integrate Bard but things are looking promising thus far with recently raised guidance.

With a stock that is trading near 52 week highs, I wouldn’t be a buyer here. However, investors should keep this one on the watch list. Buying at a lower level (19X earnings sounds about right) and holding for the long term could prove very lucrative.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment