Key highlights from Q4

PVH (PVH) has been a gem in a troubled retail industry for a long time, posting excellent growth rates in both its main divisions (Tommy Hilfiger and Calvin Klein) while the majority of its competitors where dealing with declining foot traffic in their stores, declining demand and increasing promotional activity in the wholesale channel. Last quarter’s results gave us another confirmation of PVH’s solid fundamentals, as the company’s performance exceeded even the management’s expectations.

Let’s start from revenue, which grew 19% driven by the ongoing strength of the Tommy Hilfiger and Calvin Klein businesses, with a particularly solid performance in the international business, which now accounts for more than 50% and over 60% of the company’s EBIT.

Tommy Hilfiger reported a 22% increase in sales and a 6% increase in comps during Q4, coupled with a 50% increase in operating earnings, which is absolutely outstanding. Although the strong performance was mainly driven by a 37% increase in the international segment, North America continued to show signs of improvement after the business bottomed last summer, as revenue was up 5% and comps increased 10% showing a significant gap between the wholesale and retail businesses but confirming a positive trend and another quarter of outperformance compared with the majority of the company’s peers.

The Calvin Klein business was very strong as well, with revenues growing 23% for the fourth quarter, driven by a 30% increase coming from the international business. Comps grew 4% in both the international segment and North America. Besides the outstanding performance of Q4, it’s worth highlighting that the management has mentioned further strength in the first quarter. In particular, the environment continues to improve in North America, with comps up mid-single digits for Calvin Klein and high single digits for Tommy Hilfiger. Moreover, the international business continues to grow at an excellent pace, with Tommy Hilfiger growing mid-single digits and Calvin Klein International up high single digits.

I think it’s worth focusing a bit more on these items since they tell us something important. We have to keep in mind that, although the company has performed exceptionally well while peers’ performance was lagging, the outperformance was almost exclusively a result of strength in the international business, with a particularly strong momentum in Europe, China and Japan in particular. The company was not immune to the difficult retail environment in the United States, which was affected by a series of negative factors, such as declining spending from tourists, declining foot traffic, increasing promotions (especially at third-party retailers) and unfavorable consumer spending trends due to a shift of spending preferences from goods to services and experiences, such as in the leisure and entertainment areas. PVH’s performance, especially in its own store network was very weak but offset by a growing wholesale business and the strong international momentum.

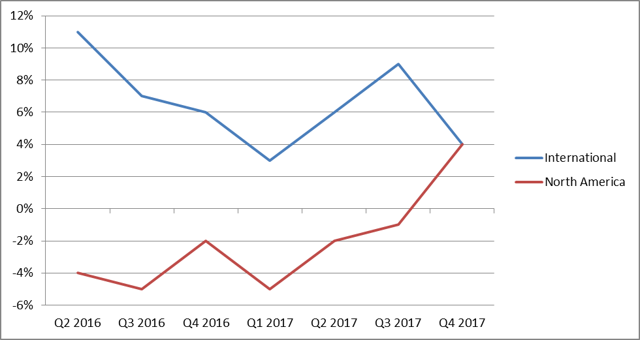

In Q4, the situation has completely changed, with Calvin Klein North America performing in line with the international business and reporting the highest quarterly increase in comps in years. The chart below shows how the performance of the international and North American segments converged this quarter:

Author’s elaboration based on data from filings and Sentieo.com

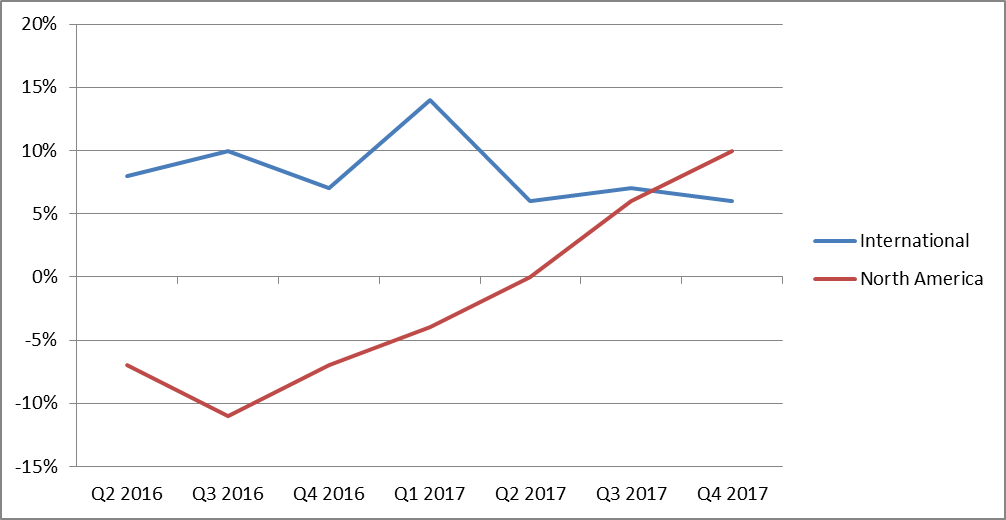

This is a very positive sign, considering how troubled the retail industry in North America has been in the past two years. This improvement is even more evident in the Tommy Hilfiger business, where the North American segment is even outperforming the international business, something that would have been difficult to believe just one year ago.

Author’s elaboration based on data from filings and Sentieo.com

Margin Trends and Future Prospects

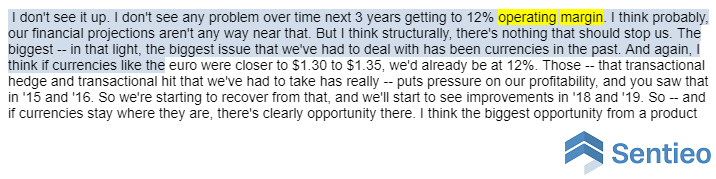

The relatively disappointing part of the performance in Q4 was in the margins trend. While gross margin expanded 80bps to 54.8%, mainly reflecting lower promotions and a better environment in North America, operating margin contracted 500bps to 2.3%, although it was down only 10bps on an adjusted basis. I am bit disappointed to see another quarter of flattish margins, in line with the previous three quarters, despite a solid top-line growth and a strong recovery in North America. This suggests the company may be having problems of operating leverage and makes me more prudent when assessing the direction of margins going forward. The management seems to be very positive on this theme, seeing a 240bps expansion in EBIT margin in the next three years:

Source: Q4 earnings call

Source: Q4 earnings call

I would consider the expansion to a 12% EBIT margin as a best-case scenario and I would definitely take the management’s words with a grain of salt, especially because they are forecasting only a 20bps increase in EBIT margin next year. Let’s consider also the negative trend in operating margin, which declined every year since 2013 despite the solid revenue growth. I definitely believe the 10.7% operating margin the market is forecasting may be a more reasonable target than the management’s ambitious goal.

In general, I think the company’s prospects remain solid despite the natural volatility that changes in consumers’ taste may bring to the business. Both Tommy Hilfiger and Calvin Klein have reported many quarters of solid growth across geographies and distribution channels. The relatively high level of diversification in terms of geographies and channels is one of PVH’s strength. Although the direct-to-consumer digital business accounts for just 10% of sales, the company has been very active in the third-party segment, implementing important strategic measures such as collaborations with eCommerce giants such as Amazon. On one side, these characteristics of PVH’s business mean the company can take advantage of growth wherever it may be. On the other side, the management stated that the eCommerce channels’ profitability is more or less in line with the traditional business and expected to grow as a result of a larger scale, which makes PVH’s growth channel-agnostic in terms of margins. In general, brands tend to benefit from the expansion of their DTC businesses (including the eCommerce platforms) as it allows them to cut middle-men costs they would face in the wholesale segment. Nonetheless, it’s always necessary to take into account the company’s specific economics, as the overall profitability of the eCommerce channel may vary significantly from one company to another. In this case, it’s good to see an equivalence between the physical and digital businesses, with the potential to see a slight margin accretion if the eCommerce channel’s profitability improved as the management is suggesting.

Risks and Final Thoughts

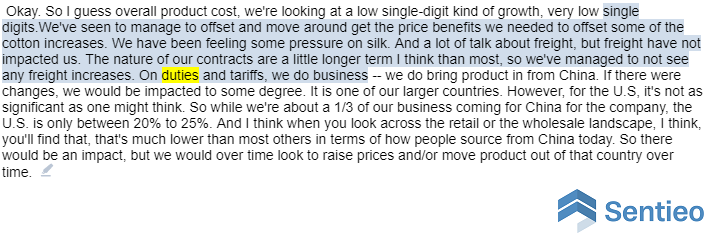

Every investment has its risks. PVH has performed exceptionally well in the recent past but is not immune to the volatility that characterizes fashion-related businesses, as any of its brand’s attractiveness may start to decline if consumer tastes change. Moreover, we have to consider that the company, like many peers in the industry, would be exposed to the risk of rising costs if the government decided to expand tariffs to more types of imports from China or other countries where PVH outsources part of its activities.

This problem has been discussed during the earnings call, as the management said:

Source: Q4 earnings call

Source: Q4 earnings call

In the end, I don’t think we will see tariffs in these areas of the consumer goods industry and I don’t think it’s necessary to adjust the stock’s risk to take into account this possibility. As opposed to the steel industry and similar ones, I think the problems related to the declining profitability and rising prices may be higher than the benefits of increasing employment in the area.

Based on the current price of $151 and EPS guidance of $9.00-$9.10 for 2018, which includes the effects of $200-$250 million of stock repurchases, PVH is currently trading at 16.6x 2018 EPS and a PEG multiple of 1.1. These multiples still look absolutely reasonable for a company with PVH’s top-line growth, especially now that some operating leverage should start to help the bottom-line as well. Even excluding the positive $0.35 effect of currency advantage, the $8.70 expected in adjusted EPS would translate into a P/E multiple of 17.4, which is reasonable as well.

In conclusion, PVH remains a good hold in a diversified portfolio, as the solid top-line growth in every market, the channel-agnostic characteristics, the prospects of a slight operating leverage and the reasonable valuation make it a good stock to maintain exposure to the underlying recovery in the retail industry.

Thanks for taking the time to read the article. If you liked it, click on the follow button at the top of the page. You will get my articles as soon as they are published. I am available to further discuss the topics of this article in the comments section. If you are interested in having access to long and short ideas in the consumer and tech areas or want to know when PVH will be a strong buy or short, please consider joining Consumer Alpha. A 2-week free trial is currently available.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment