The Home Depot (HD) stock has slid nearly 17% from their high in January, despite posting solid results for the year. The company continues to perform very well, with a growing top line and expanding margins.

{kind=link}

Looking forward, 2018 is set to be another good year for the retailer – yet concerns regarding industry sales have placed pressure on the stock lately. We feel these fears are overstated, as the company holds unique characteristics distancing it from any substantial e-commerce threats.

As the company continues its push into the home decor space, we believe this moat will only widen. Looking at valuation, Home Depot trades on the low end when considering their wide moat and superior performance metrics compared to its peers.

Financial Overview

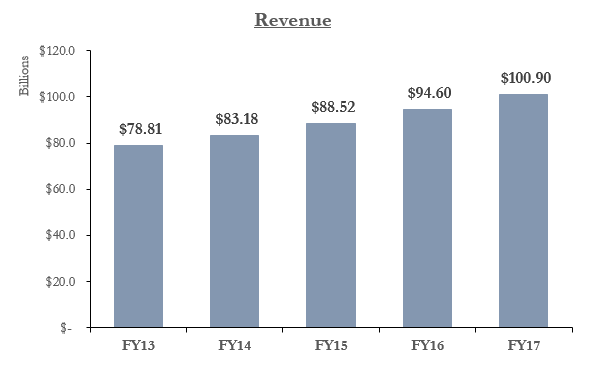

2017 was yet another great year for Home Depot, with sales seeing growth of ~6.7% y/y. The company has maintained a strong growth rate over the last several years, boasting a five year CAGR of over 6%.

Source: Morningstar

The outlook for the company’s top line remains bright, and well protected against the increasing threat of e-commerce giants such as Amazon (AMZN). We believe Home Depot has found itself in a unique position, as it sells products which individuals typically do not look for online. These products are also quite expensive to ship, making it in the best interest of the customer to visit the actual store. This also does not take into account the heavy services business Home Depot offers customers.

Source: Morningstar

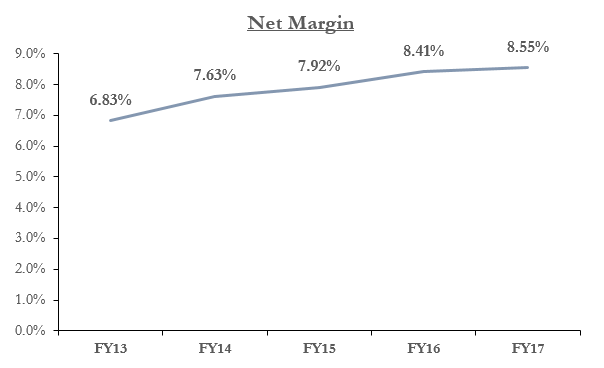

Margins continue to perform very well, with an overall growing bottom line. Although gross margins saw a decrease of 11 bps, lower OpEx more than offset this, resulting in a net margin increase ~14 bps y/y.

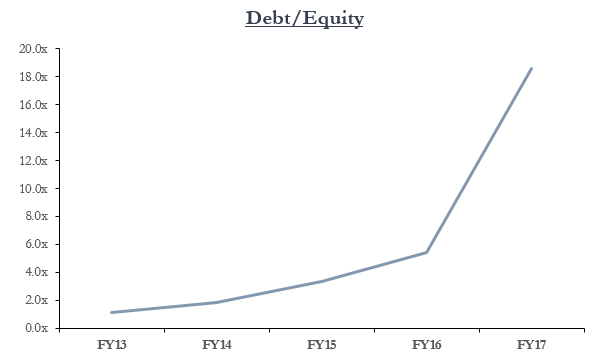

Looking at the balance sheet, Home Depot ended the year with roughly $3.6 billion in cash, up over $1 billion from the previous year. On the other hand, their total debt also saw an increase of about $2.8 billion y/y, resulting in total debt of just over $25.8 billion.

Source: Morningstar

The company remains highly levered, with a high debt-equity ratio of nearly 20x. Some investors may feel concerned regarding the leverage, but from what we see, Home Depot has proven to be wise with debt.

Source: Morningstar

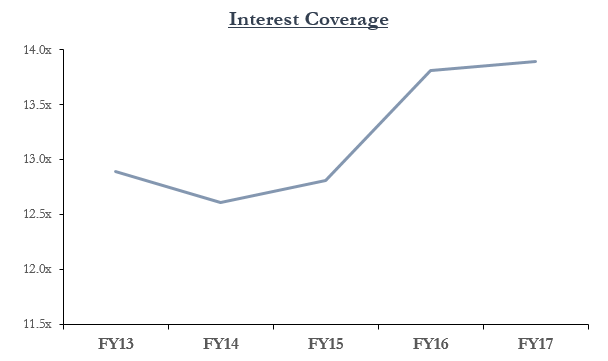

The company’s EBIT is more than enough to cover the interest expense on debt, with a coverage ratio of nearly 14x. The improving financials only increase Home Depot’s coverage ratio, placing them in a better position to manage their debt.

Home Depot & Pinterest

We see further room for growth in the recent “Shop The Look” venture with Pinterest, with the potential to change the way customers shop at the store. They have recently announced intentions to expand this with over 100,000 home decor products, which can certainly garner interest from consumers, driving traffic to stores.

{kind=link}

This goes hand-in-hand with the “Built In Pins” video campaign, which gave Pinterest users insight into the work behind home interior photos (showing before, during, and after shots of the project). This compliments their recent acquisition of The Company Store back in December of 2017 (terms not disclosed), certainly showing a softer side of Home Depot. Home decor-related products make up ~ 25% of Home Depot’s sales according to Credit Suisse, with only 3% attributable to pure decor products. As the company zeroes in on the pure decor segment, the upside is substantial.

The way customers shop at Home Depot may soon change, as customers cover their home improvement and styling needs – all in one location. Ticket size may see an increase with due time, as products are paired with their decor counterpart.

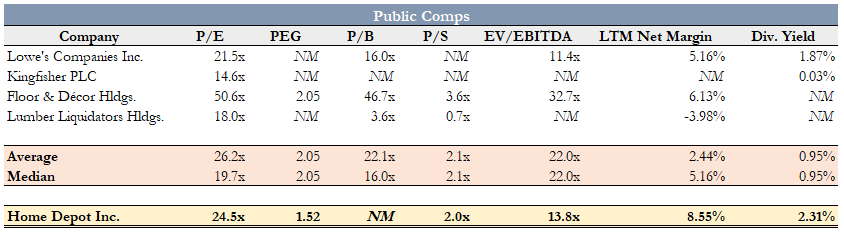

Relative Valuation

When comparing the company to industry peers, Home Depot trades just below the peer average LTM earnings multiple.

Source: S&P Capital IQ

Home Depot trades at ~25x LTM earnings, below the industry average of ~26x earnings. This is more than reasonable given an LTM net margin of ~8.6%, which is higher than the industry median of ~5%.

Other factors which we believe justify Home Depot’s current valuation is its dividend; management has been consistent with dividend increases, and with a healthy track record comes some added value. That being said, we feel the valuation for Home Depot is fair at these levels. While it many not be a screaming buy, the stock is not expensive.

Conclusion

Home Depot continues to turn up impressive results, posting solid FY’17 results. The company saw revenue growth year-over-year above 6%, as well as expanding margins.

The future looks bright as well, as Home Depot pushes into the home decor space via M&A (The Company Store) and pursues a “Shop The Look” expansion with Pinterest. We believe this market won’t be difficult for Home Depot to thrive in, and see home decor playing a role in future revenue growth.

Valuation-wise, the company trades in-line with industry comps, and is not expensive in our eyes. We believe the current valuation is more than justifiable.

We believe the pressure the stock has faced is largely unwarranted, and a result of industry-wide concerns. With the company well-positioned against competition, we foresee Home Depot continuing to impress shareholders through 2018.

We maintain our buy rating, and $210 PT, reflecting a ~22x earnings multiple on Bloomberg’s 2018 EPS estimate of $9.43.

Disclosure: I/we have no positions in any stocks mentioned, but may initiate a long position in HD over the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment