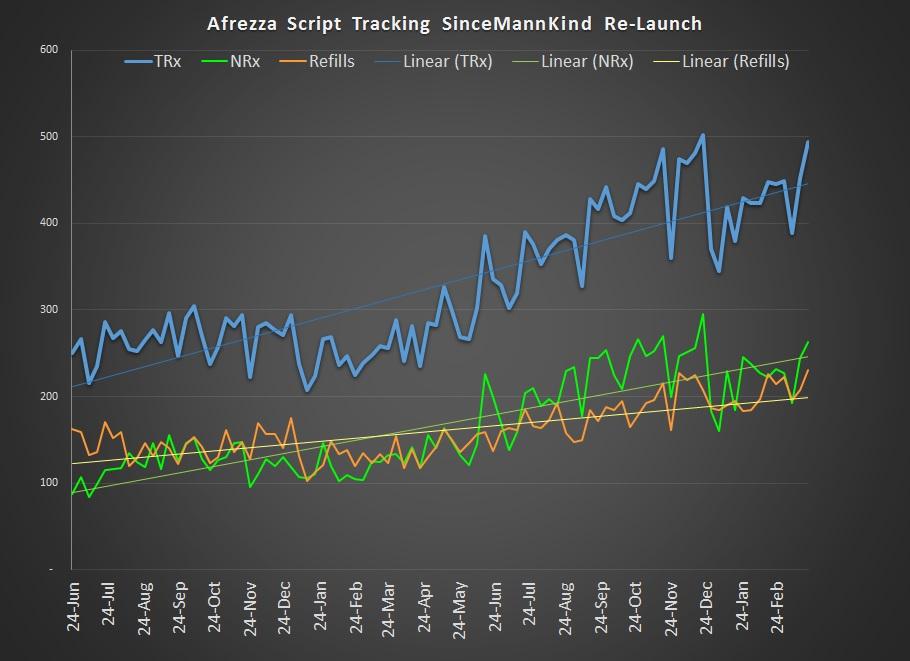

MannKind (MNKD) investor saw sales for Afrezza on the week ending march 23rd rise to a level just shy of 500, a level only eclipsed once since the company took back control nearly two years ago. With the exception of the second to last week of last quarter, the 500s have been uncharted territory for the company. Afrezza sales have been in the 400s (a couple of weeks in the 300s) for 28 weeks now.

{kind=link}

Chart Source – Spencer Osborne (based on Symphony Data)

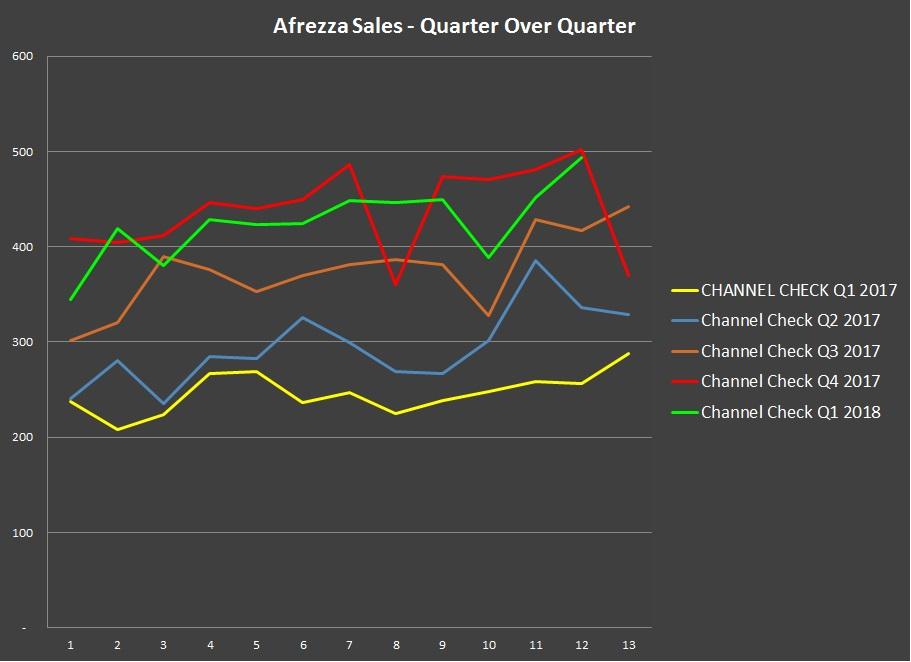

Quarter Over Quarter

Based on this latest sales report, it is apparent that scripts in Q1 of 2018 will come in below what was delivered in Q4 of 2018. With 12 out of 13 weeks reported, sales in the current quarter are pacing 4.41% lower. Q4 of 2017 delivered scripts sales of just over 5,700. Next week’s scripts would need to come in at 605 in order to match that number. Simply stated, it is unlikely.

Chart Source – Spencer Osborne (based on Symphony data)

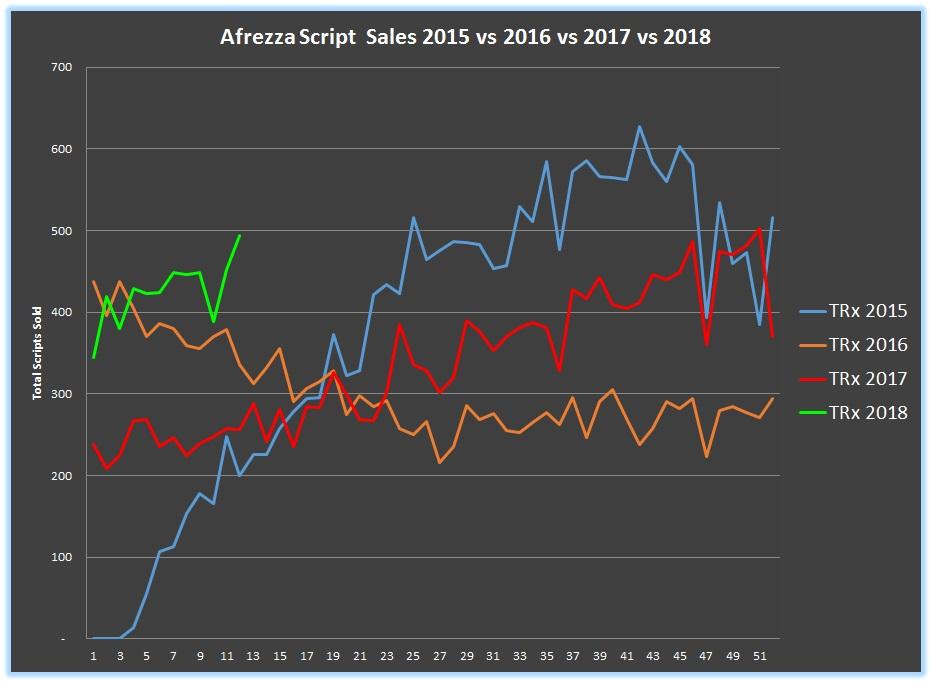

Year Over Year

The year-over-year numbers sound much more impressive. Sales in Q1 of 2018 are currently pacing 74.89% better than what was delivered a year ago. Readers should bear in mind that a year ago there was a sales force shake-up in Q1.

Chart Source – Spencer Osborne (based on Symphony data)

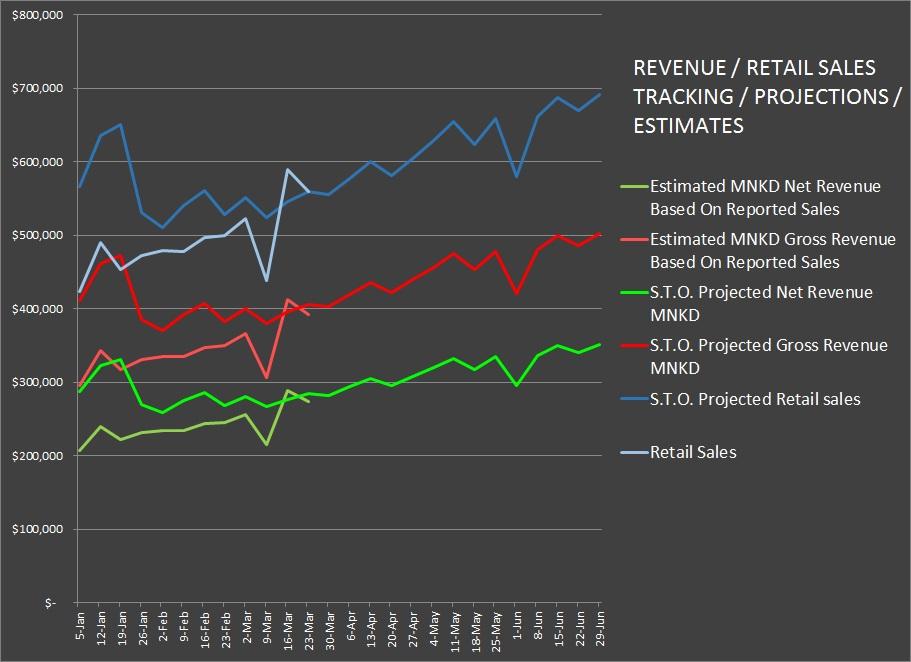

Revenue Related To Scripts

Script revenue has three components that are oft confused. There are retail sales, which is the amount of money the end user pays; gross sales, which is the amount of money wholesalers and distributors pay MannKind; and net revenue, which represents what is left after certain expenses are deducted. Retail sales last week were about $560,000. By my estimate, gross sales were about $392,000, while net sales tallied about $274,000. For the bulk of Q1, all three categories have been coming in a bit below what I had projected. Over the past two weeks, these numbers are falling in line with my projections. The good news is that the dollars are finally catching up. The bad news is that there is lost ground to make up, and my projections are well below what is actually needed to impress the Street and perhaps deliver equity appreciation.

Chart Source – Spencer Osborne (based in part on Symphony data)

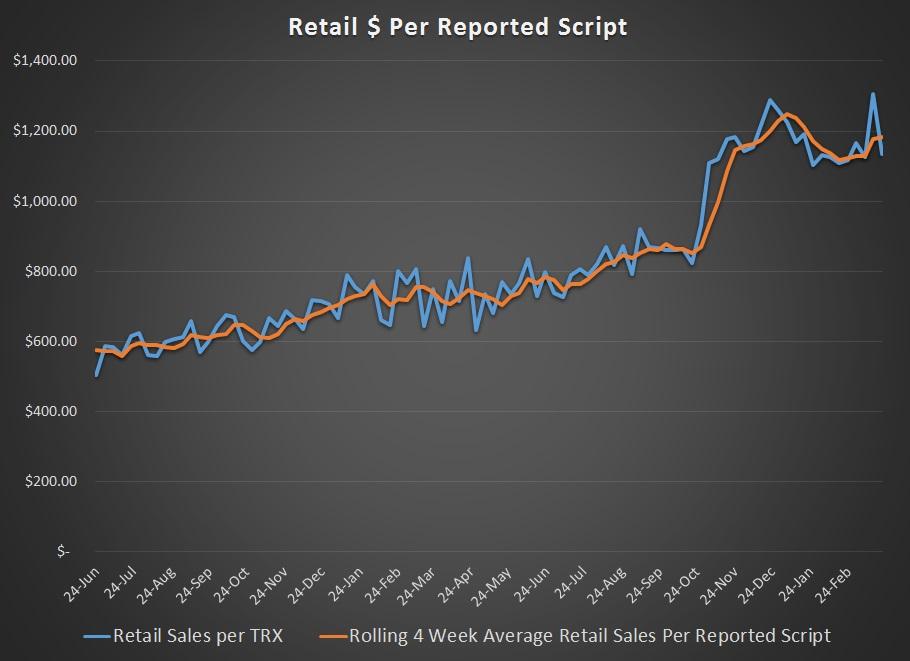

Looking at the retail sales per script allows investors to assess the level of money that MannKind brings in on a tracking basis via reasonable deductions for gross and then net respectively. This past week, the retail sales per reported script were about $1,133, while the four-week average is higher at $1,182. Swings in retail sales per script relate to the number of titration packs (which are bigger and more expensive) vs. the number of standard packs.

Chart Source – Spencer Osborne (based on Symphony data)

Projections

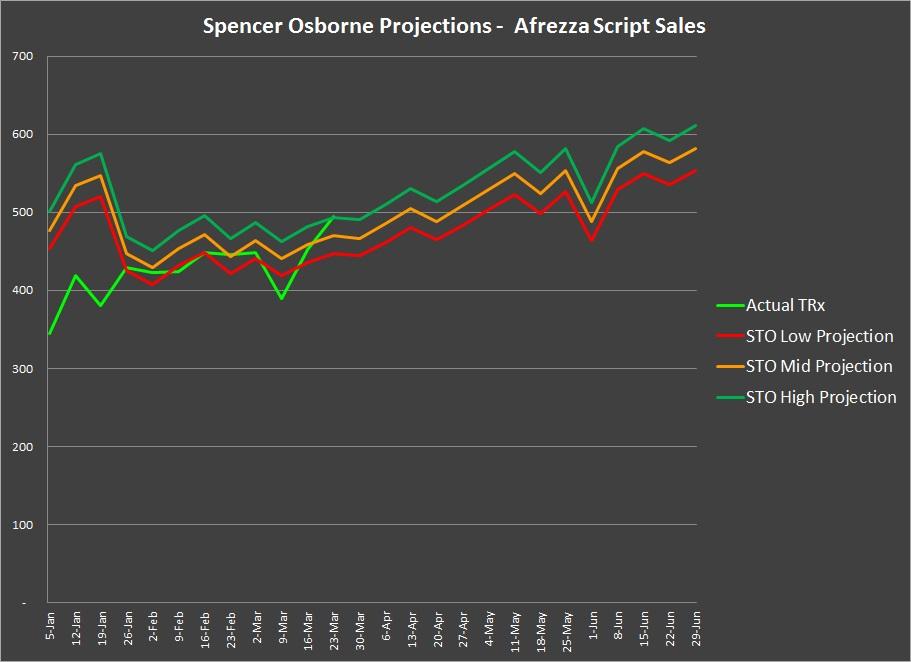

I outline projections for script sales and revenues in six-month intervals. Historically my projections have been quite accurate, and the more formal estimates I derive once data is collected get more accurate still. These days I get very little push-back on my projections. In terms of script projections, the data in the most recent week is presenting at the high end of my range. Next week’s data brings another month to a conclusion, and I will be assessing projections and assumptions once again.

Chart Source – Spencer Osborne (based in part on Symphony data)

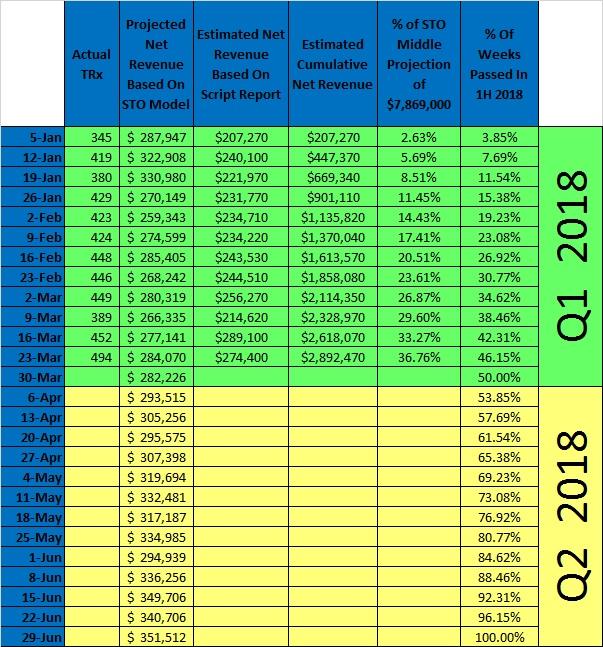

My revenue projections boil the numbers down to net revenue, which is the important metric for investors to follow. Based on my assessment, the last week’s worth of data brought the net revenue tally up to just under $2.9 million. This should mean that the full quarter will deliver just under $3.2 million in net revenue.

Chart Source – Spencer Osborne (based in part on Symphony data)

MannKind Guidance

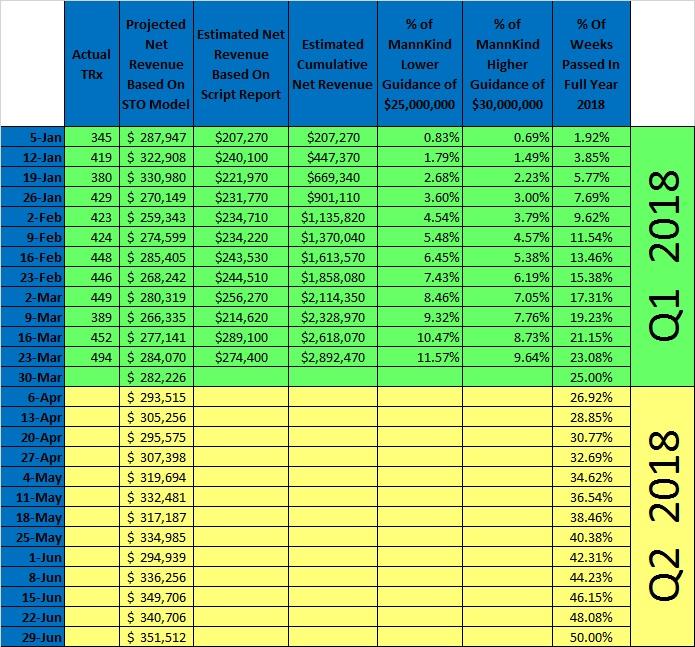

In February of this year, MannKind offered guidance related to net Afrezza revenue for 2018. The low end of that guidance was $25 million, while the upper end stands at $30 million. That guidance is a bit on the aggressive side when you consider that Q1 will bring in just 12.5% of what is needed with 25% of the time passed.

Chart Source – Spencer Osborne (based in part on Symphony data)

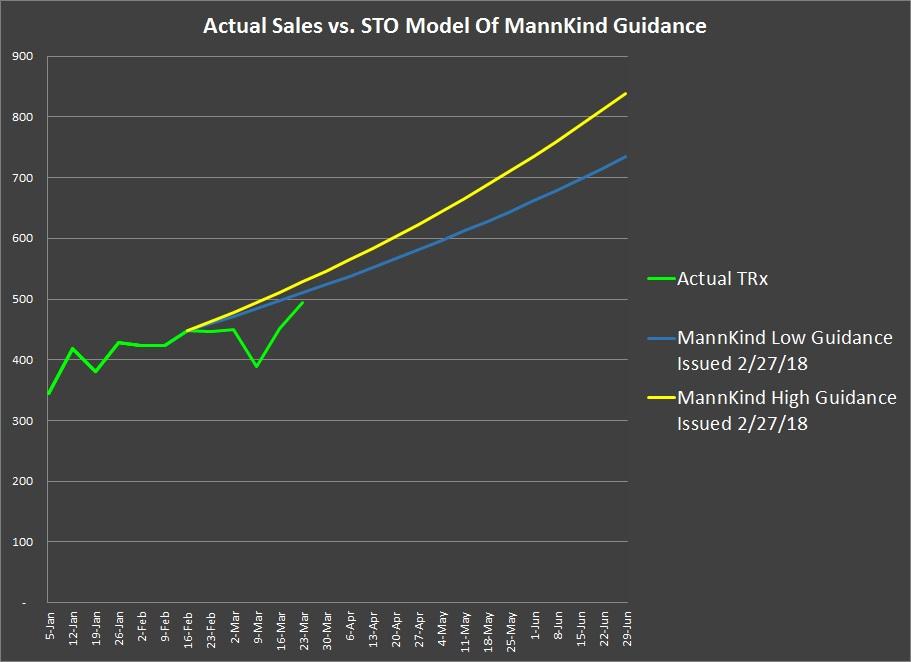

To illustrate the guidance MannKind offered its investors, I converted the dollars back into scripts. We all get to see scripts weekly, and this allows investors to better track progress. The chart below shows that MannKind is behind the needed pace. The most recent data could show promise, but there is something to bear in mind. Hitting guidance means that continued substantial growth is needed each week. Afrezza has spent 28 weeks in the 400s in terms of scripts. Hitting guidance requires it to spend just seven weeks in the 500s, six weeks in the 600s, five weeks in the 700s, four weeks in the 800s, and so on and so on.

Chart Source – Spencer Osborne (based in part on Symphony data)

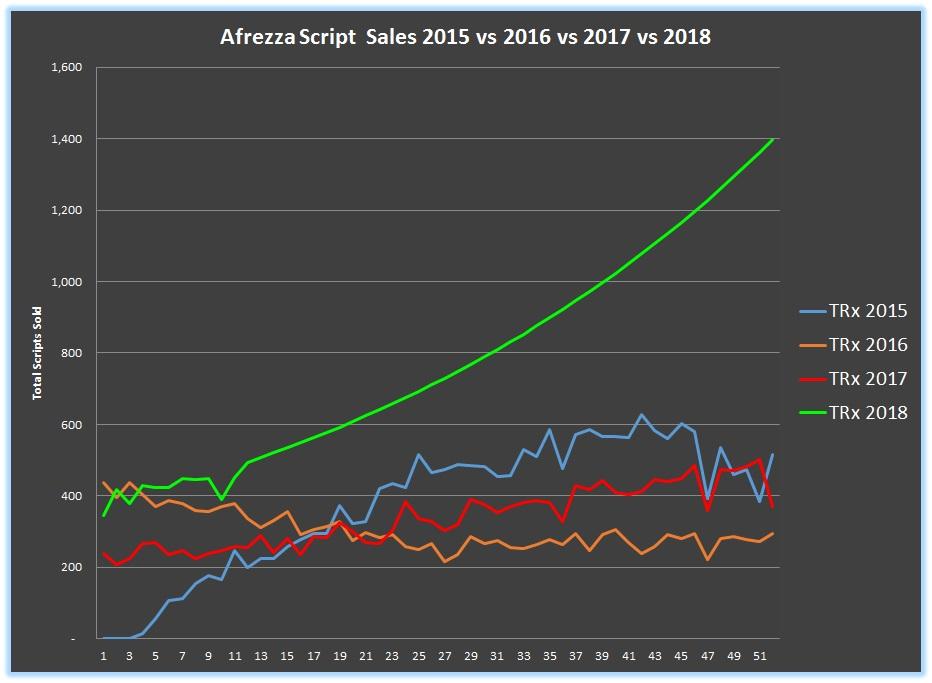

If you look at the data for the year, you can begin to see why I think that the guidance is aggressive. The chart below shows the sales track for previous years. The smooth part of the green line is what would be needed to hit the low end of guidance. As you can see, vast improvement is required in order to hit the numbers.

Chart Source – Spencer Osborne (based in part on Symphony data)

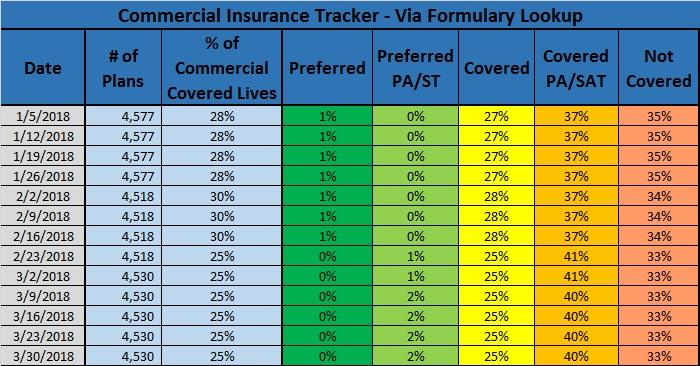

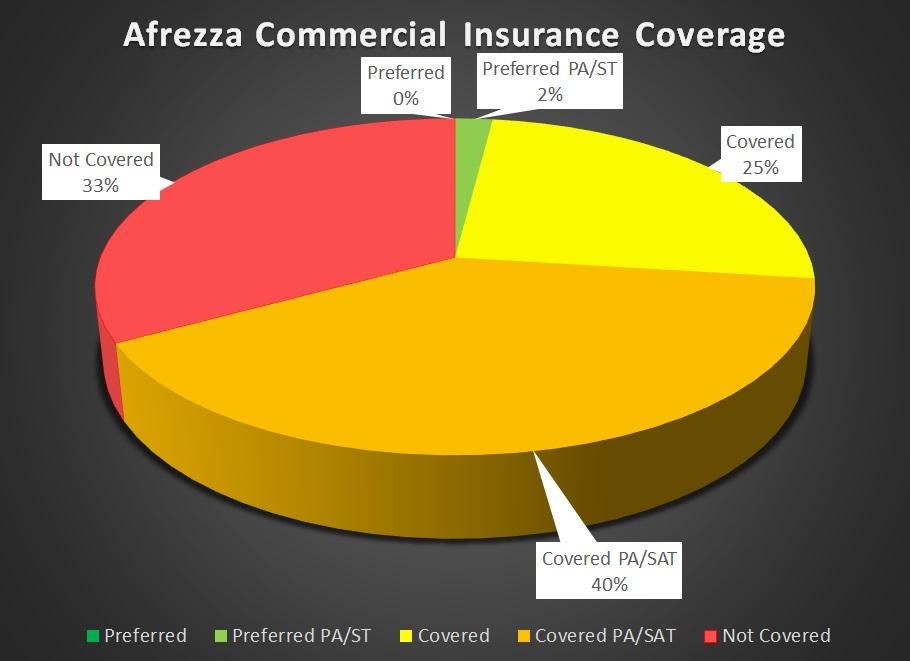

Insurance Tracker

A critical component to the sales relating to any drug is insurance. MannKind has been trying for years to deliver improvement in this area of its business. Afrezza, relatively speaking, has pretty poor coverage. It is mostly on unfavorable insurance tiers compared to other treatments. This means that out-of-pocket cost is more for Afrezza’s customers. The charts below track the insurance issue. In Q1 of 2018, MannKind made modest progress offset by modest setbacks.

Source of Charts – Spencer Osborne (based on Formulary Lookup)

Source of Charts – Spencer Osborne (based on Formulary Lookup)

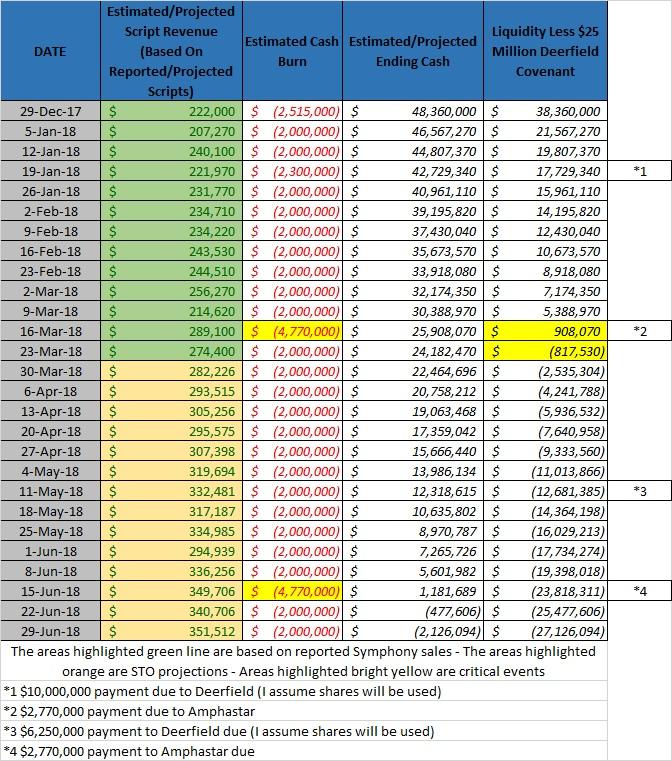

Cash

It is said that cash is king. I happen to believe that the cash situation at a speculative company is an important metric to track. A lack of cash means that a company is forced into making difficult decisions and may not be able to fund aspects of its business in a manner that can help to deliver growth. I estimate that MannKind finished the week of March 23rd with about $24.2 million in cash. This assumes a full contracted payment to Amphastar (AMPH) and that no use of the ATM facility has transpired. It also assumes that interest payments are made in cash. MannKind can use shares in lieu of cash, which is something additional that investors need to consider.

Management has stated that it will be in compliance with a Deerfield covenant that requires the company to finish each quarter with at least $25 million in cash. By my estimation, it will have missed. The explanation could be use of the ATM facility, extensive cost cutting, use of shares to handle debt interest, and a smaller payment to the insulin supplier than contracted. MannKind has already indicated to its insulin supplier that it would not meet the minimum purchase option in the contract. Investors should assume that MannKind will finish the quarter with between $25 million and $30 million in cash.

I estimate that unless a move is made, MannKind will be out of cash prior to the end of Q2. This means that some form of capital infusion is needed in the near term. In my opinion, it will get a small injection ($10 million to $20 million) from a proposed international deal that is in the term sheet phase but management indicates will happen in Q2. This would still mean that dilution will be required.

Chart Source – Spencer Osborne

Summary

MannKind remains a speculative play. The downward pressure this week took the stock down to $2.18 before a partial recovery to $2.30. This remains a great trading stock as it is volatile enough to deliver action in either direction. Further, some of the events that will happen are predicable. The timing of dilution can be anticipated, and the news around other events can be determined ahead of time. That predictability helps active traders. MannKind has yet to deliver compelling sales or compelling deals that can change the rules of the way the Street looks at this equity. The company has about 14 weeks to show it can hit its guidance, or yet another piece of data will become a weight on the shoulders of the shareholders. Stay Tuned!

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment