In my previous article Teva Pharmaceutical: Generidiculous!, I highlighted the generic giant’s growth avenues and valuation metrics, which I concluded to be undervalued. Since the release of the article, even though it wasn’t all that long ago, Teva’s (TEVA) share price appreciated just over 53% from $13.00 per share to $20.00 per share as a new $3 billion investment was announced, dividend was suspended, workforce reduced, an Allergan (NYSE:AGN) settlement and most recently, a stake from Warren Buffett’s Berkshire Hathaway (BRK.A) (BRK.B).

I previously focused on its generics pipeline and valuation metrics, which I believed were undervalued due to potential growth in generics sales. As the company continues to launch new drugs in developed and emerging markets with more than 600 generic solutions awaiting in final approval stages, the company has a significant opportunity to diversify its product portfolio which relied heavily on sales of its blockbuster drug Copaxone, which since has drawn immense competition from generic versions of Mylan (MYL) and others.

As both revenues and EPS are expected to decline in 2018 before stabilizing through 2020, headwinds do exist; but as I expressed previously – the company’s current trading ranges are fairly conservative given the aforementioned factors.

Debt

One of the key worries, and a key aspect I left out of my previous article, was the company’s high debt load. The company currently holds $28.8 billion in long-term debt which was reduced from its peak holding of $33.8 billion two quarters ago. However, the company has recently announced a plan to issue $5 billion in new debt to finance its turnaround efforts, which will bring total LT debt back to around $34 billion.

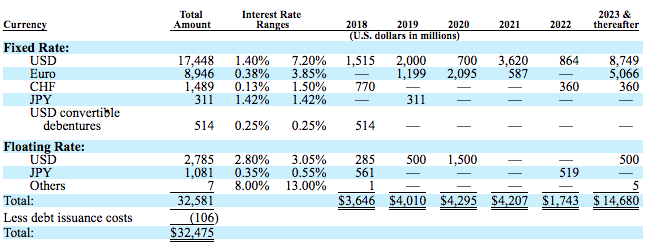

Teva has significant debt maturities in the upcoming years with $3.6 billion due in 2018 alone. As it doesn’t expect much net income growth until 2019 and 2020, the company’s $3.5 billion in operating cash flows for 2017 is set to decrease as new drug launches take some of the heat from the loss of revenues from Copaxone but not cover the entirety of it.

{kind=link}

(Source: Company 10K)

As European interest rates remain fairly low and the company continues to hold foreign exchange swaps, alongside some debt downgrades by Moody’s (MCO), I believe the company’s $5 billion in debt to cover corporate turnaround programs and pay back 2018’s debt maturities bodes well as it sets to utilize this new debt to reduce corporate spending by around $3 billion throughout the year. Without worrying about this year’s debt maturities, the company can use its 2018 cash flows to continue and launch more generic drugs and raise operational efficiency.

Debt remains a weight on the company’s performance as it is both limited in issuing new debt since it was downgraded and as it uses a significant amount of the newly issued debt to cover maturities, leaving future cash flows to fund its turnaround and limiting R&D expenses. I expect the company to operate on the edge of debt and financing activities, but remain well solvent through its massive cost-cutting measures.

On behalf of the company’s debt, it paid $875 million in interest expense in 2017 alone, which is expected to remain flat in 2018 with debt reduction and issuance, respectively. As it remains on target to cut around $3 billion in expenses through 2019, as it decreased over $400 million in 2017, this expense remains well within the range of sustainability and will decrease by around $90 million as it pays down around $3.6 billion throughout 2018.

Growth: Supporting Cash Flow

Although a lot of investors tend to focus on the company’s Copaxone sales decline, which produces the highest margins, the majority of Teva’s sales came from its generics business where it generated over $12.3 billion in 2017 compared to just under $8 billion in the specialty medicines where Copaxone is classified. As generic sales grew 2% (or 10% in local currency terms), it accounted for the majority of growth in overall revenues for the year as the other segment reported a 9% decrease due to Copaxone’s generic competition.

As the company’s guidance points to a reduction in 2018 sales to $18.6 billion, based on an aggregate of estimates, the company’s generics business is expected to continue and grow solidly as it launches new drugs. Notably, in 2018, the company launched QVAR RediHaler for Asthma, Syperin for Wilson’s disease, Korlym generic for Cushing’s syndrome, Fremanezumab (A CGRP) and TRIENOX for APL, to name a few, with a >$150 million US market share each. These launches should aid the generic business growth for the time being, offsetting some of the $1 billion a year loss from Copaxone, which is expected to increase in 2018 as more companies release generic version of the drug.

By The Numbers

Reduced from previous estimates, analysts in aggregate expect Teva to report $18.6 billion in sales in 2018 and $17.9 billion in 2019. This assumes no major drug sales from newly launched generics but assumes all the losses from Copaxone revenue declines. I do believe, however, that these numbers reflect a slightly too pessimistic view of the company’s generics potential and that these numbers, unless revised, are easily ‘beatable’ by Teva.

EPS is expected to remain fairly stagnant with the company’s high cost-cutting measures after falling from $4.01 in 2017 to $2.43 in 2018, based on analyst estimates compiled by Bloomberg. With cost cutting of around $3 billion in 2019 offsetting some losses, EPS is expected to rise to $2.87 in 2019 and remain on a ~5% annual growth rate thereafter, without taking into account any further generic or specialty medicines blockbuster launches.

Conclusion

In my previous article, I presented a >$25.00 per share price target for Teva Pharmaceutical based on growth expectations throughout 2019 and 2020. As share price approached that figure earlier on in the year following some key events, I believe that range remains fair value for the company until it can concretely show evidence of the turnaround phase working and meet its $3 billion cost reduction target.

As debt remains high, it also remains highly executable and sustainable as the company funds paying down $3.6 billion this year through a combination of new debt issuance and cash flows. As analysts expect Teva to generate around $2 billion (range) this year, I believe it remains highly solvent through 2019 as it continues to launch new generic drugs to offset the catastrophic loss of exclusivity of Copaxone. I remain bullish on Teva and believe it is undervalued in the long run.

Disclosure: I am/we are long TEVA.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment