A few years ago we recommended Orchid Island Capital (NYSE:ORC) as a high-yielding mortgage real estate investment trust. In retrospect, the stock quickly became one of the sector’s biggest losers, but began to see strength from 2016 into 2017. With shares at a 52-week low of $6.80, we want to check back on the stock following its recently reported results. It is our belief that the stock can be traded, but you should avoid this name. To demonstrate, we will discuss the critical metrics and assess the dividend coverage of the underlying company. Moreover, we will discuss our take on the stock going forward.

Table 1. Key Metrics of Orchid Island Capital In Q4 2017

|

Key Metric |

Most Recent Data* |

|

Q4 2017 book value and % change from Q3 2017 |

$8.71 (-4.8%) |

|

Net interest rate spread in Q4 2017 |

2.68% |

|

Dividend (yield) |

$0.42 (24.7%)** |

|

Q4 Net income per share |

$0.42 |

|

Q4 Adjusted income per share |

$0.49 |

|

Dividend covered? |

Yes |

|

52-week share price range |

$6.77-$12.60 |

Source: Orchid Island Capital Q4 Results

*as of 12/31/17

**dividend paid monthly at $0.14

Addressing the dividend and earnings

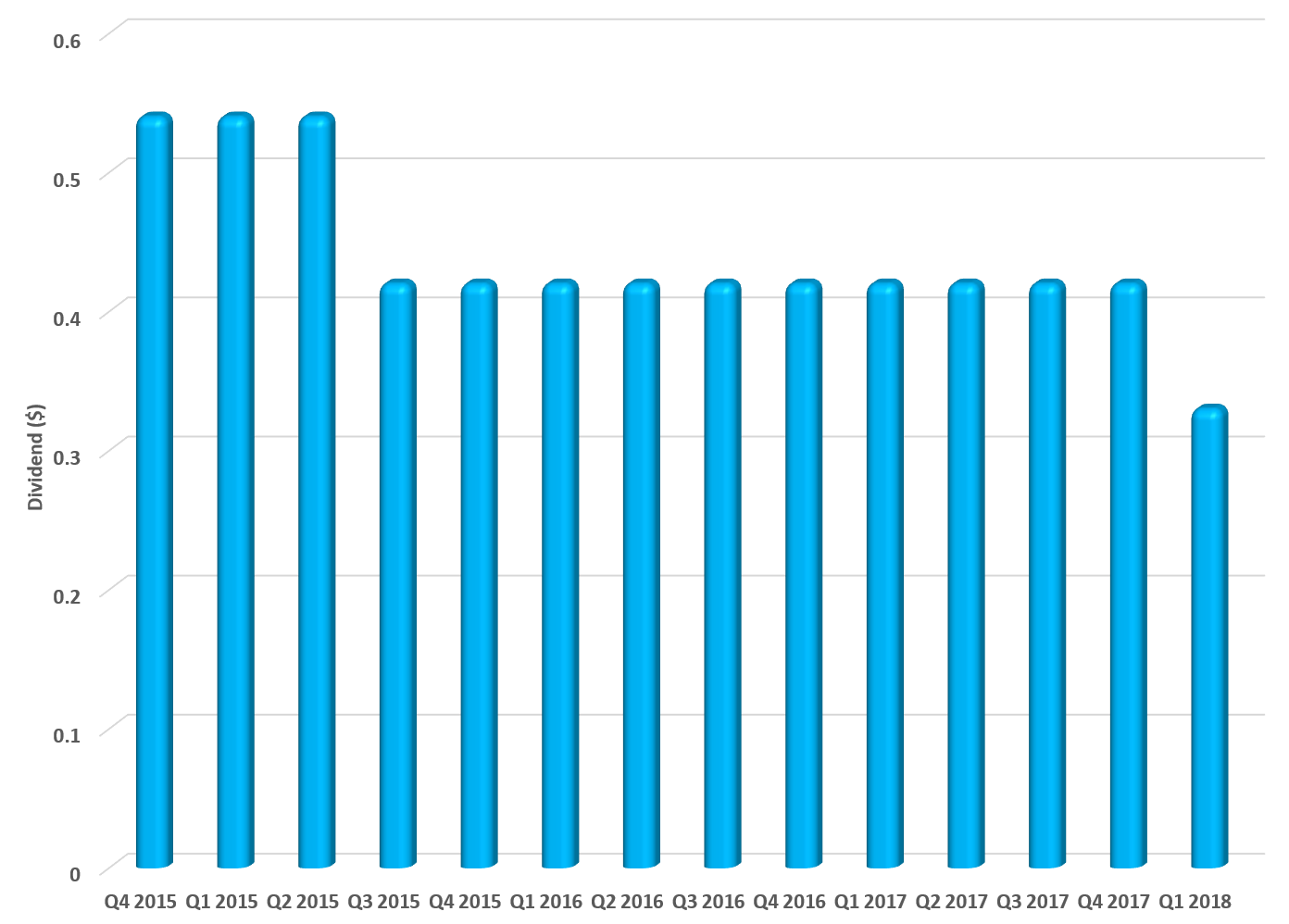

Considering that we buy names like this for the dividend, the recently announced dividend cut hurts. Unfortunately, the $0.14 per month payment was unsustainable given the performance of the company which we will discuss. However, based on a share price of $6.80, the payout of $0.42 in the quarter translated to a 24.7% annualized yield. With the new cut to $0.11 monthly, at $6.80 per share, the yield is still a bountiful 19.4% annualized. However, this cut continues a history of a declining dividend:

{kind=link}

Source: SEC filings

As you can see, this most recent 21% cut to the dividend is hardly the first time we have seen a cut. The reason the dividend was cut again was due to earnings and funds from operations failing to cover the dividend.

Orchid Island Capital saw a loss of $6.0 million or $0.12 compared to a loss of $20.4 million last year. Losing less money is a positive, we suppose. However, one way to measure the ability of the company to pay its dividend is to make adjustments for unrealized losses/gains on mortgage backed securities and net interest expense on swaps. These earnings were $0.49 per share. In addition, net investment income was $0.55 per share. However, the losses from net income are quite clear.

The real reason the dividend has continued to be paid out despite heavy losses (aside from financial adjustments to show adjusted coverage) is the company’s ongoing aggressive issuance of new shares, which dilute shareholders. In addition, the adjusted earnings of the company and the finances raised from share issuance was not enough to continue the payout. We actually believe the cut would be more drastic than down to $0.11. Let us consider some of the other metrics.

Funds from operations

As many of you know, we believe it also can be helpful to examine a company’s funds from operations. This is a bit more telling of the situation at Orchid Island Capital. That said, Orchid Island Capital’s most recent available funds from operations show that the funds from operations have really been on the decline the last few quarters. The most recent data show funds from operations coming in $3.86 million and $23.7 million. That said, with a $0.42 dividend per quarter, and roughly 48 million shares out there, you are looking at approximately $20.2 million in dividends paid. The funds from operations compared to these payouts demonstrate the shortfall. After factoring in returns and the dividend, book value took a hit.

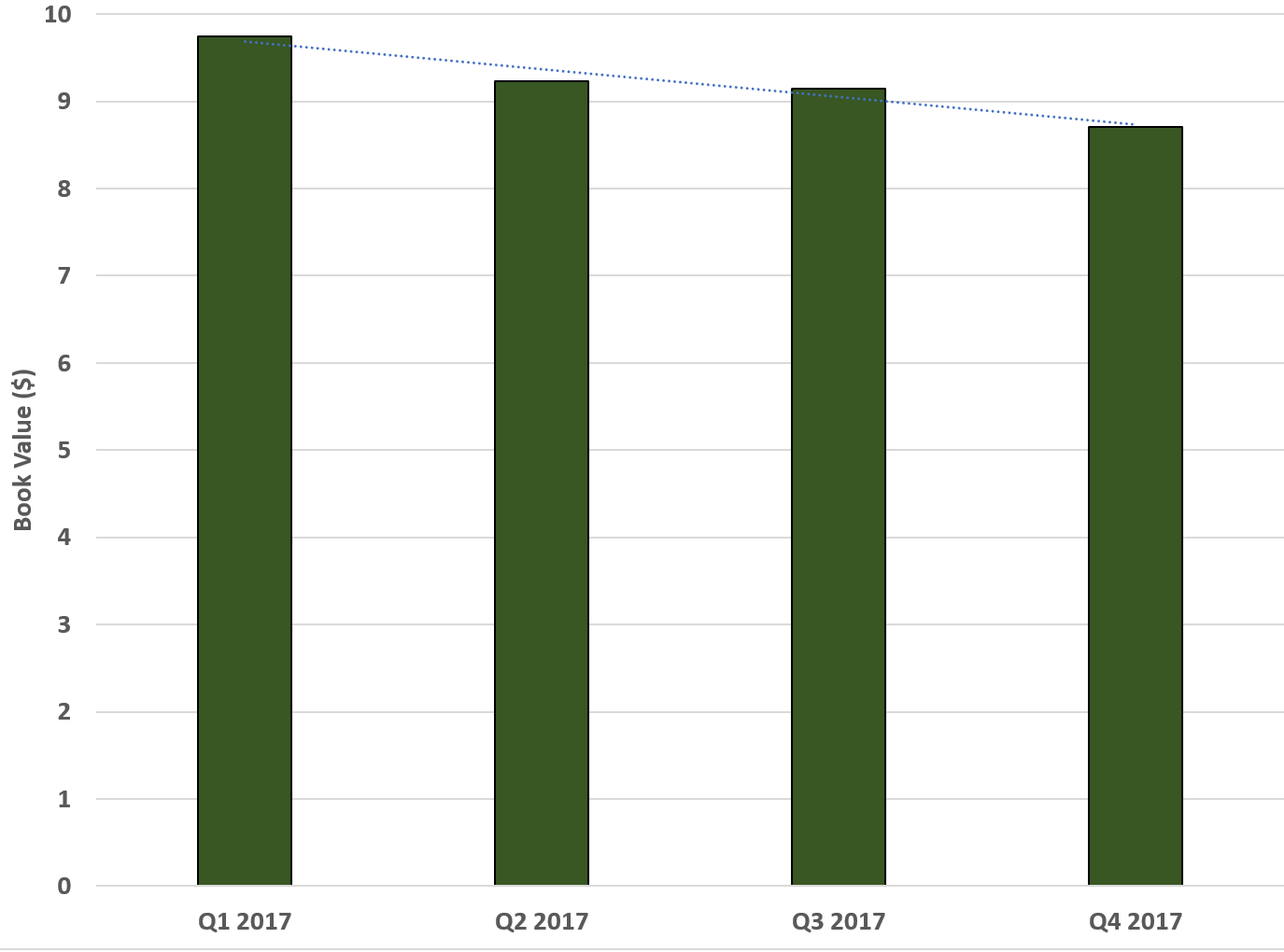

Book value and share repurchases

When valuing an mREIT, we need to know what we are paying relative to what the company’s assets are roughly worth. Book value has been falling over the last few quarters. Just look at the recent trends:

Source: SEC filings

Here in Q4 book value fell another 4.8% to $8.71. The reason it fell so much was due to pressure in some of the holdings, notable a constant prepayment rate that led to yield pressure and a narrowed spread. That said, the company is trading below book value once again. At $6.80 the stock trades at a $1.89 or 21.6% discount to book.

One promising event that could help offset some of the capital raises and book value hits we keep seeing is that management has announced an additional stock repurchase authorization. Through December 31, 2017, Orchid bought back a total of 1,216,243 shares for $10.8 million, including commissions and fees, for a weighted average price of $8.92 per share. The Board has now authorized an additional 4,522,822 shares of common stock for repurchasing, which results in a total authorization under the repurchase program for up to 5,306,579 shares, or approximately 10% of outstanding shares. Let us turn to more portfolio specific metrics that help inform us as to why we are seeing performance declines.

Constant prepayment rate

One surprisingly good piece of news for the company which helped contribute to net interest income of $0.55 was that the constant prepayment rate is the lowest it has been in the last seven quarters:

We saw the constant prepayment rate spike for the company in Q3, but have returned to levels that are the lowest of the year. Even though prepayments are higher than we would like they are still slightly below sector average. Of course, comparing across the sector we have to realize that prepayments vary based on holdings, but it is undeniable that high levels of prepayments lead to lower yields and returns for net interest income, on average. In the present quarter prepayments were at 9.1%. This had a positive impact on yields, but costs were an issue.

Net interest rate spread

Orchid saw its average asset yield on its RMBS investment portfolio come in at 4.18%, up nicely from 3.63% as a result of lower prepayments and movement in interest rates. However, this same interest rate movement caused a significant spike in costs of funds to 1.50% from 0.78%. As a result, Orchid’s net interest rate spread narrowed slightly. Doing the math, the spread came in at 2.68%, down from 2.85%. This explains the decline in net interest income from $0.58 to $0.55 per share.

Looking ahead, rates are set to rise. As such we will see pressure on costs but Orchid’s hedging strategies should come into play successfully and offset some of this pain.

Conclusion

Orchid Island Capital remains a bit of an under the radar name. Another dividend cut has occurred because the payout was unsustainable. We thought the cut would be more drastic as evidenced by the funds from operations. Moving forward, we like the share repurchase plan so long as there are not future equity issuances. This company issues equity a lot to help keep the party going, which is why dividends were not cut sooner.

At present levels, there is a nice discount-to-book which can probably be bought for a quick trade, but we would not buy the name here. We think this name is best to be avoided given the volatility, and would instead prefer you in more stable mREITs that we have covered previously. It was a bad call in the past. While the dividend offset much of the losses, it has not been enough. Those still holding should wait for a spike to liquidate.

Quad 7 Capital has been a leading contributor with Seeking Alpha since early 2012. If you like the material and want to see more, scroll to the top of the article and hit “follow.” Quad 7 Capital also writes a lot of “breaking” articles that are time sensitive. If you would like to be among the first to be updated, be sure to check the box for “email alerts” under “Follow.”

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment