Celgene’s Long-Lasting Underperformance

If an average Joe invested $100 in Celgene’s (NASDAQ:CELG) stock in 2015, he would have lost $17 now. At the same time, if he invested in the S&P 500 (SPY) or the Nasdaq Biotech ETF (IBB), he would have gained $30 and $2 respectively.

Celgene clearly underperformed and missed investors’ expectations in the last three years. It has been and continues to be a Revlimid company that has not been yet able to substantially diversify its sales and define its future after Revlimid.

Mission and Vision

Recent appointment of Mark Alles, current CEO, as chairman of the Board is not a good practice. Executives need to have an independent oversight that will keep the management accountable.

On the other hand, CEO and chairman can be the same person when the leaders are “visionaries” – like Zuckerberg and Musk. But is Mark Alles a visionary? Let’s take a look at Celgene’s mission and vision statement.

Celgene states that its mission is to “seek to deliver truly innovative and life-changing drugs for our patients” while its vision is to “build a major global biopharmaceutical corporation while focusing on the discovery, the development, and the commercialization of products for the treatment of cancer and other severe, immune, inflammatory conditions”.

While we absolutely cheer Celgene’s mission, we completely don’t understand the company’s vision. So, the company’s goal is to become a major pharma? By sales? By profit? Wouldn’t it be more logical/appealing to mention societal goals rather than focusing in becoming bigger in size??

Just take a look at the mission and vision statements of some of the other pharma companies and see how different they are from those of Celgene’s:

Do you see the difference? The vision of the most successful companies is focused on the people the company is trying to serve, not on themselves. If one tries to build a successful company, first you need to think about the societal problem you are trying to solve, and if you are successful, then you will be well compensated… And it is not all the way around – “I want to be rich, let’s see how I can get there”.

While this may seem as a minor thing, we think it is subconsciously important for investors to understand whether the company is able to see 10+ years ahead of itself. Whether its CEO breathes with his/her visionary ideas and will not leave for political, personal or any other reasons.

Next, we wanted to take a closer look at each of Celgene’s revenues to understand where the company is headed.

Revlimid

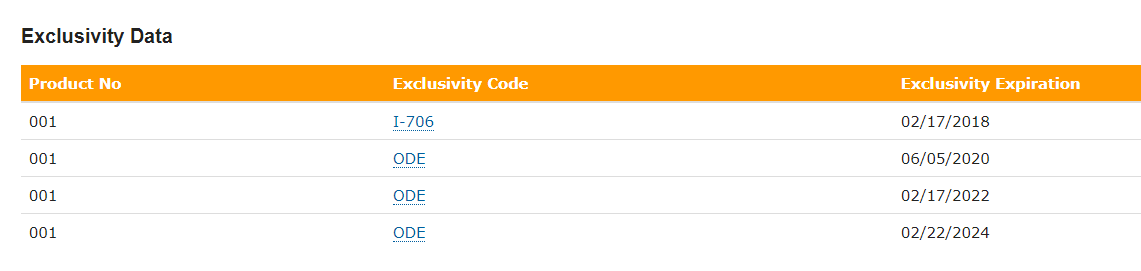

Revlimid has been a champion and a major contributor to Celgene’s success story. Celgene has managed to secure FDA exclusivity for Revlimid until 2024, which means that no other ANDA may be accepted until 2024.

As an exception, the company settled a dispute with Natco (Allergan’s (NYSE:AGN) subsidiary) that can file an ANDA in March 2022 with mid-single-digit volume with gradual increase going forward:

The volume limitation is expected to increase gradually each 12 months until March of 2025, and is not expected to exceed one-third of the total lenalidomide capsules dispensed in the U.S. in the final year of the volume-limited license under this agreement…

Celgene will permit entry of generic lenalidomide before the April 2027 expiration of Celgene’s last-to-expire patent.

Given the limited volume allocated to Natco (~5% initially with gradual increase to 33%), we don’t think it will be wise for Natco to aggressively compete on price. We modeled 0% growth rate for Revlimid 2022 sales as we assume the 5% loss in production volume will be compensated by a natural increase in duration of therapies and annual increase in price. The U.S. sales loss will accelerate starting in 2022 with “epic” 80% loss in sales in 2026. In 2024, based on EU Revlimid LOE, international sales may lose 70% as well:

Based on what we know now, 2022 will be a peak sales year for Revlimid ($13.4 bn) and it will still constitute around 60% of total Celgene sales.

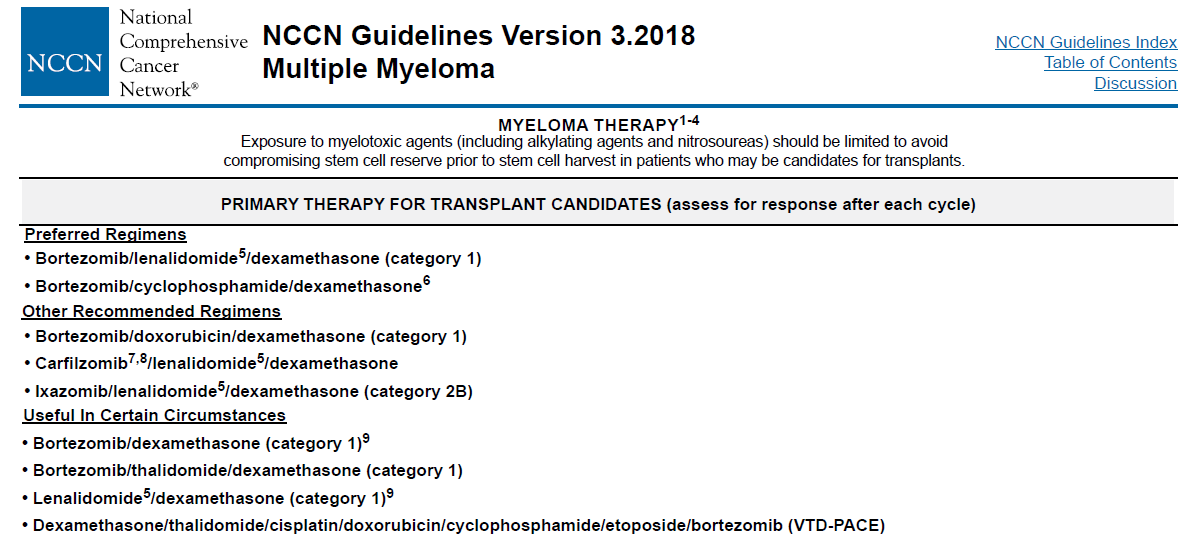

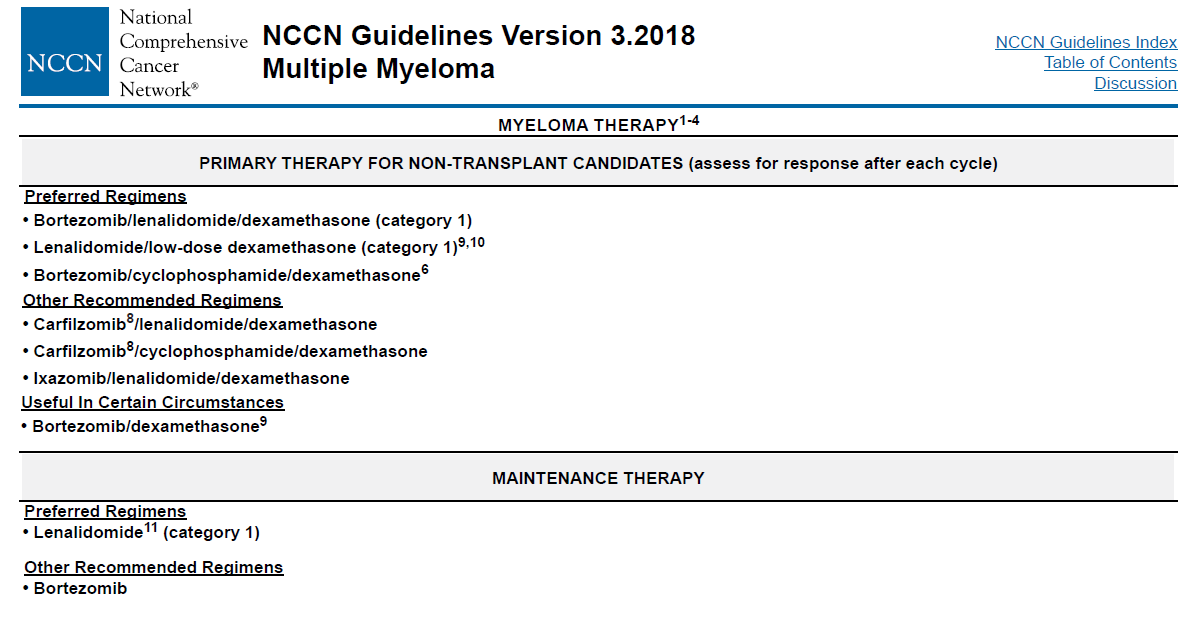

Many Revlimid skeptics may question Revlimid’s continuing success. But the reality is that Revlimid is the best drug for multiple myeloma, MM, the main indication with more than 100K commercially prevalent patients. MM NCCN guidelines, the main North Star of U.S. hem/oncs for making clinical decisions, have a priority Category 1 recommendation of lenalidomide (Revlimid) based regimens for transplant, non-transplant and maintenance patients:

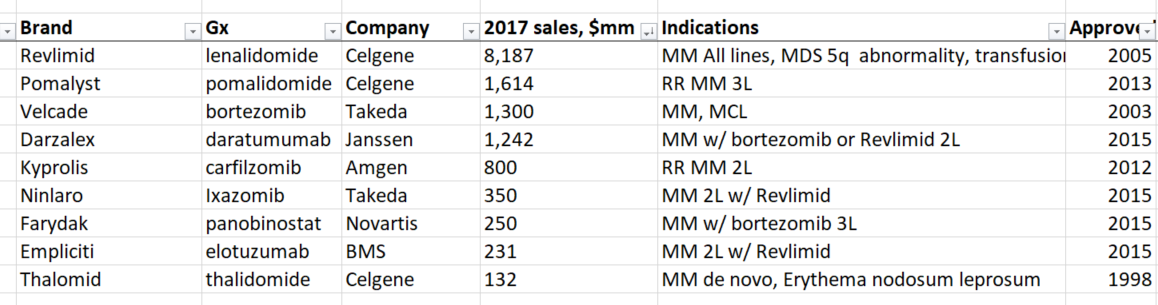

Many of the second line options (2L) that are recommended by NCCN are to be administered together with Revlimid. 2L options include Darzalex, Ninlaro, and Empliciti (Darzalex has an option to be administered with Revlimid or Velcade):

In other words, Revlimid’s additional sales are positively correlated with the increased use of 2L Darzalex, Ninlaro, and Empliciti that were all approved in 2015 and have a collective annual sales of $1.8 bn, and this is just the beginning of the lifecycle of these drugs. $1.8 bn of Darzalex + Ninlaro + Empliciti revenue means $1.8 bn revenue of Revlimid in addition to Revlimid use in the first line.

Some Celgene critics say that company drives the Revlimid sale by constantly increasing price. Here’s the official explanation in CELG’s 10-K 2017:

REVLIMID® net sales increased by approximately $1.2 billion, or 17.4%, to approximately $8.2 billion for 2017 compared to 2016, primarily due to increased sales in both U.S. and international markets. U.S. sales growth increased due to both price increases and, to a lesser extent, an increase in unit sales from market penetration and treatment duration of patients using REVLIMID®. In addition, unit sales increased across all international regions, primarily in Europe and Japan, driven by increased duration of use and market share gains. International volume growth was partially offset by net price decreases.

We think it is absolutely normal to increase the price of a drug as long as the magnitude of increase is within the 10-20% range. And in case of Revlimid, it’s not just a price increase that drives the revenue. Patients live longer, utilization is higher, and other 2L treatments drive the use of the drug.

Pomalyst

Pomalyst is pomalidomide used in 3L of MM. We expect it will peak at $3 bn in 2024, with LOE in EU in 2023 and in US in 2025, given no additional patent extensions will be filed.

Otezla

Otezla, a PDE4 inhibitor, was approved in 2014 to treat PsA. Psoriasis in general is an extremely competitive therapeutic area with a large number of pharmacological options. Simply said, it’s hard to make money on psoriasis only. While there are multiple ongoing studies to test Otezla in UC, Behçet’s disease and scalp psoriasis, it is unclear how successful Otezla will be in other indications. We are going with the conservative estimation based on PsA only and peak revenue at $2.9 bn in 2023:

Abraxane

It is obvious that Abraxane has tough times competing with others in MBC, NSCLC, and pancreatic cancer. In the U.S., the situation is not expected to improve:

ABRAXANE® net sales increased by $19 million, or 2.0%, to $992 million for 2017 compared to 2016, primarily due to increases in unit sales in international markets. The increase was partially offset by decreased unit sales in the U.S. The decrease in U.S. unit sales reflects the continuing competition in breast cancer and lung cancer indications.

Ozanimod

For Ozanimod, we will conservatively go with $1.5 bn in 2023 for MS alone:

Fedratinib

Fedratinib is basically a 2L myelofibrosis treatment:

The first line, Jakafi, made only about $1.2 bn six years after launch. Even if fedratinib is better than Jakafi (which is not the case based on what we know now), it would be unrealistic to expect more than that.

BCMA CAR-T (bb2121/bb21217)

bluebird’s (NASDAQ:BLUE) bb2121 is a very promising CAR-T treatment for MM. Potentially, it may substitute Revlimid after 2025, but the problem is the bb2121 ramp-up takes time and generic lenalidomide will be too good and too cheap to ignore it. In the best-case scenario, bb2121/7 may peak at $10+ bn sometime in 2030.

Juno’s (NASDAQ:JUNO) cellular immunotherapy

The company expects the launch in 2019 and reaching $3 bn sometime after 2020 (we think it’s 2026).

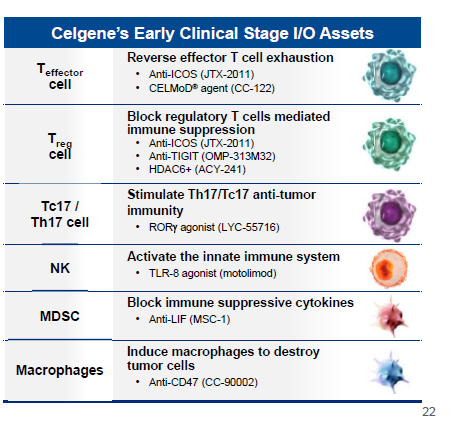

Celgene’s Early-Stage I/O assets

Too early to put a dollar sign on them.

Anti-PD1 (BGB-A317) for Solid Tumors

This is definitely an interesting asset that is currently being tested as a monotherapy and in combination for various solid-organ and blood-borne cancers. The only problem is that it might be too late for PD-1/PD-L1 asset with Opdivo and Keytruda dominating the market. We can’t forecast any numbers at this point, but we certainly think that BGB-A317 is a promising asset.

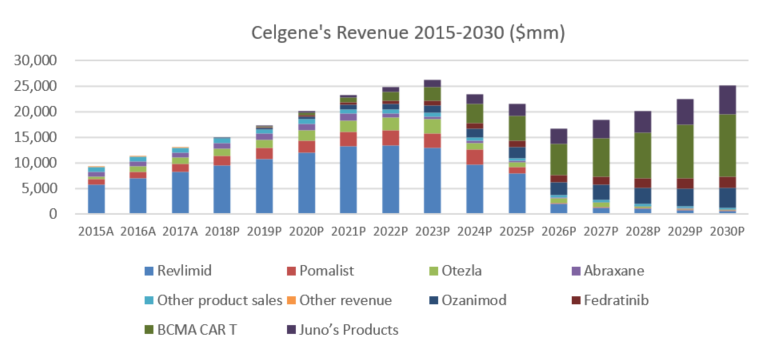

Celgene’s Revenue in 2015-2030

Now, to sum up all the revenue streams, this is what we get:

The most notable threat is that the revenue is going to drop in 2024. However, if we smoothen out 2018-2030 revenues, we still get 4.12% CAGR, which is a kind of long-term terminal growth.

It is obvious that investors are spooked by the revenue drop in several years. But if we look at the graph from the long-term point of view, the current 11x P/E of 2018 earnings resembles the P/E of a “boring” value company with low growth.

Conclusion

Celgene is traded at the level of low growth “value” companies (they may think of paying dividends to prove that?). Unless the company comes up with a plausible explanation of how it plans to fill the gap after 2023, the current trading level may persist at 10-14x of 2018 P/E or $90-120 per share.

Disclosure: I am/we are long CELG.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment