Penn Virginia’s (PVAC) deal to be acquired by Denbury Resources (NYSE:DNR) was mutually terminated recently in the face of opposition from major shareholders. This leaves Penn Virginia as a standalone company that appears able to generate a modest amount of positive cash flow at current strip prices while also growing average 2019 production by around 9% from Q4 2018 levels. The company appears to be undervalued at the moment, with an enterprise value of only 3.1x estimated 2019 EBITDAX at current strip prices. An improvement to 3.5x would increase its share price to $57.50, which would still be slightly lower than its estimated PV-10 at $59 oil.

2019 Outlook

Denbury’s Q4 2018 presentation indicated that Penn Virginia expects to average approximately 28,000 BOEPD in 2019 with a two-rig program. This production level would result in it generating approximately $504 million in oil and gas revenue at current strip prices (roughly $58 WTI oil). Penn Virginia’s swaps have slightly negative value as they are at prices that are a few dollars below current strip. After hedges, the company is expected to deliver around $488 million in revenue during 2019.

| Barrels/Mcf | $ Per Barrel/Mcf (Realized) | $ Million | |

| Oil | 7,767,200 | $59.00 | $458 |

| NGLs | 1,277,500 | $20.00 | $26 |

| Natural Gas | 7,051,800 | $2.90 | $20 |

| Hedge Value | -$16 | ||

| Total Revenue | $488 |

Capital expenditures are expected to be approximately $325 million, resulting in total cash expenditures of approximately $475 million. Thus, Penn Virginia would be expected to generate around $13 million in positive cash flow in 2019 in this situation.

| $ Million | $ Million |

| Lease Operating Expense | $43 |

| Production and Ad Valorem Taxes | $27 |

| Gathering, Processing and Transportation | $25 |

| Cash G&A | $17 |

| Cash Interest | $38 |

| Capital Expenditures | $325 |

| Total Expenses | $475 |

Production Growth And Breakeven Point

The two-rig drilling program in 2019 is expected to result in daily production in 2019 averaging around 9% higher than in Q4 2018 and around 29% higher than in 2018.

If Penn Virginia wanted to maintain production at Q4 2018 levels instead, it may be able to do so with a $250 million capital expenditure budget. This would lead to an estimated unhedged breakeven point being in the high-$40s for WTI oil at the moment. Due to its rapid recent production growth (with Q4 2018 production up 108% from Q4 2017), the base decline rate is pretty high right now. Its breakeven point would likely drop to the mid-$40s as its production growth slows and its base decline rate lessens.

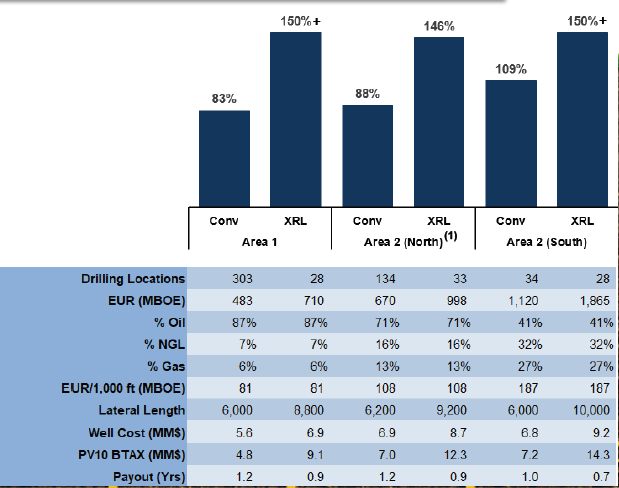

Penn Virginia benefits from having very strong returns, with most of its drilling locations delivering RORs in the 80% to 90% range at $60 WTI oil and $3 natural gas, and around 22% of its locations potentially delivering over 100% RORs at $60 WTI oil. Penn Virginia’s Eagle Ford production sees favorable oil and gas differentials due to its location.

Source: Penn Virginia

Inventory

The company’s main weakness is that it has a relatively modest amount of inventory. It had around 560 gross locations (461 net locations) as of August 2018. This represents approximately 10 years’ worth of inventory at 2018’s drilling pace, although activity is expected to be a bit lower in 2019.

Penn Virginia also indicated it was spudding around 20 XRLs in the second half of 2018, and it only has around 100 of those high-return, longer-lateral locations.

The relatively modest amount of inventory may result in Penn Virginia continuing to look for deals (either to be acquired or to acquire additional properties) going forward.

Valuation

PVAC is currently valued at approximately 3.1x its estimated 2019 unhedged EBITDAX at strip prices ($58 WTI oil). It probably deserves a relatively low multiple due to its relatively modest amount of inventory, but even with just a 3.5x multiple, shares would be worth around $57.50.

Penn Virginia is also currently valued at around 0.68x PV-10 at 2018 SEC pricing, although that includes a significant amount of value for its PUDs (which represent 42% of its total PV-10 at 2018 SEC pricing). The company noted that a 10% decline in commodity prices would reduce its PV-10 to $1.444 billion. This would be pretty close to forward-year strip prices, although longer-term oil and gas prices appear to be modestly lower still. Penn Virginia is trading at around 0.83x this lower $1.444 billion PV-10.

At $57.50 per share, the company would be valued at approximately 0.95x the $1.444 billion PV-10 number (which is based on roughly $59 oil and $2.80 natural gas).

Conclusion

The mutual termination of the acquisition by Denbury reduces Penn Virginia’s debt-related risk as it won’t be exposed to Denbury’s upcoming debt refinancing issues now. However, it does also leave the company needing to figure out a longer-term plan once its inventory starts dwindling. It still has around 10 years of inventory at 2018’s drilling pace, although that tends to be on the lower end for upstream producers.

Penn Virginia does seem undervalued with its recent decline in price, and could be worth 25% more if it rebounds to $57.50 per share. This would still be a relatively low 3.5x multiple to 2019 EBITDAX at current strip prices, as well as less than PV-10 based on $59 oil.

Free Trial Offer

We are currently offering a free two-week trial to Distressed Value Investing. Join our community to receive exclusive research about various energy companies and other opportunities along with full access to my portfolio of historic research that now includes over 1,000 reports on over 100 companies.

Disclosure: I/we have no positions in any stocks mentioned, but may initiate a long position in PVAC over the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment