If you were to tell me that you are a perfect investor who never makes mistakes, I wouldn’t believe you. That simply does not exist. While most people can hide behind an anonymous brokerage account and only discuss their Top Winners at cocktail parties, I do not have that luxury. All my calls are made public to readers on Seeking Alpha, and while it is tempting to forget about my losers and showboat my victories, it would be dishonest to my followers.

In today’s article, we take a look at my biggest losers and most importantly, we seek for ways to avoid making the same mistakes again. Learn from my costly mistakes, so you don’t have to make them too!

Mistake #1: Class B Mall Investments

The US retail real estate market is oversupplied and the growth of Amazon (NASDAQ:AMZN)-like companies is posing a severe treat to traditional malls. Yet, I still had the genius idea of investing in Class B malls back in 2016.

How could I have been so stupid you ask?

Well, back in 2016, the major Class B mall REITs, CBL (CBL) and WPG (WPG), were still posting positive NOI and FFO growth while paying a double-digit dividend yield and trading at just around 5x FFO!

The market was telling us that the end was near, but given the positive fundamentals (back then), I came to the conclusion that investors were overreacting and overly pessimistic on the retail space. After all, people are social human beings, and being a millennial myself, I know that malls remain very popular to even the younger generation. Moreover, as lower-quality mall REITs keep removing undesirable retailers such as Sears (OTCPK:SHLDQ) and J.C. Penney (JCP) from their properties and replace them with new, exciting stores and restaurants, the sales and traffic are set to improve, right?

Performance of CBL since publishing my first bullish article on the company

(To be fair, in the article, I noted that I prefer WPG and that I am not invested in CBL. Nonetheless, I was bullish and both have been big losers, one more than the other).

Ouch! Yes, Ouch!

What went wrong?

The thesis was very simple. We had a diversified portfolio of malls that had produced very decent results thus far, and it was on sale at a very high cash flow yield due to a negative market sentiment.

Unfortunately for me, the market was correct to be so negative. Six months after my initial investment, the positive NOI growth turned negative, an avalanche of store closures hit the market and the share price tumbled. Eventually, the dividend was cut as increased capex was needed to improve the properties and fight the increasing vacancy rate.

The lessons:

- Look into the future, not in the past. Until 2016, the performance of these properties had been overwhelmingly positive, and therefore, I quickly came to the conclusion that the market was overreacting to headline risk. I should have instead focused more on the future. Maybe I could have anticipated some of the major retail bankruptcies which caused NOI to suffer very shortly after my initial investment.

- Generally speaking, it is preferable to stick with quality names in challenging sectors. All retail REITs, including high-quality ones such as Simon (SPG), were relatively cheap back then, and there was no need to pick the more speculative companies to play our underlying thesis.

Mistake #2: Doubling Down on Speculative Names

The second mistake is very much linked in to the first one. It is important to recognize the difference between investing and speculating. In my mind, an investment has a much greater sense of certainty in that we can rely on consistent and predictable cash flow and long-term property appreciation.

Speculation, on the other hand, especially in real estate, has a “question mark” factor that remains unsolved. Something is out of our control and can cause great losses if things turn south.

Class B malls are a great example of investments with a high speculative nature. This is especially true when you add leverage to the mix.

They may turn around and provide great rewards, but it is far from being a certainty, and a big portion of the risks are out of our control. Will tenants default at the worst time? Will banks continue to work with CBL? Will the management do what is right for investors or try to milk the assets for hefty salaries until an inevitable bankruptcy? …

As minority shareholders, we have very little influence over these risk factors that could make or break an investment and therefore it is important to recognize the speculative nature and set limits when it comes to averaging down on a losing position. In hindsight, it is easy to say that it was a mistake to average down on CBL since I lost money on it, but even if CBL had recovered, this would have been a mistake because I failed to recognize that I was speculating, not investing.

It is fine to hold some speculative positions as part of a well-diversified portfolio, but I should have been more reluctant to averaging down on them.

The Lessons:

- If you are in the hole, you need to stop digging!

- There is a massive difference between averaging down on a high-quality REIT like Brookfield Property (BPR) as we did during the sell-off in late December and doubling down on a highly speculative name like CBL.

- Differentiate speculative investments from the rest and set higher requirements to justify additional capital in case of losses. Throwing more capital to a losing position is rarely the solution when dealing with speculative names.

Mistake #3: New REIT IPOs

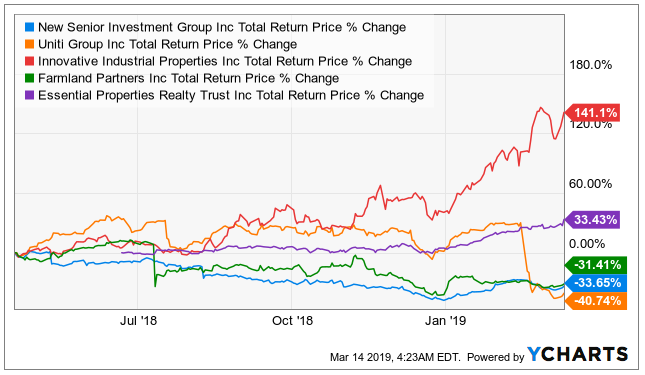

Our track record with freshly IPOed REIT investment opportunities has been poor, very poor! We have had a few victories including Innovative Properties (IIPR) and Essential Properties (EPRT), but the profits are not enough to justify the losses in Farmland Partners (FPI), Uniti (UNIT), and New Senior (SNR).

Fresh IPOs are highly volatile, and the businesses (and management) are yet to prove themselves at successfully running a public company.

Looking back, Essential Properties was a no-brainer (net lease assets, consistent growth, low leverage, and big discount), but all the other picks were too risky so early on in their operating history and simply ignoring them could have saved us a lot of money.

The Lessons:

- There is no need to rush into the new and exciting REITs. It can pay off big sometimes (IIPR up over 300% since IPO in 2016), but it is much riskier and more often than not (at least in our case) the results have been rather disappointing.

- IPOs have on average performed poorly, irrespective of market sector, and REITs do not appear to be an exception. An easy way to avoid the underperformance of the average IPO is to simply skip these companies and let them run for ~5 years before reconsidering again.

Takeaway

- The quality of companies matters

- The difference between speculating and investing matters

- And finally, the honesty with yourself matters

It is very tempting for many authors to hide their losers while showing off their latest winners. The truth is that no one bats a 100, and literally every author on Seeking Alpha has made some bad calls on certain investments. Hey, I heard a well-known investor (arguably the GOAT) made a mistake and taken a bath with Heinz (NASDAQ:KHC).

What matters more than the mistake itself is to learn from these mistakes to grow as an investor. To achieve this growth, we must be brutally honest with ourselves, and this is what we seek to do here. What investment mistakes have you made in the past? Share in the comment section below!

High Yield Landlord, The #1 Service for Real Estate Investors

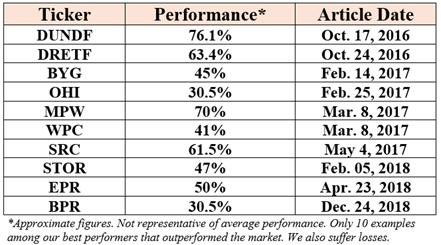

We focused on my losers in this article, but if you read this far, you deserve to also know about our biggest winners and most importantly, our future predictions.

Want to Know Our Next Top 10 Picks?

Join us today on a 2-week free trial and find out why over 300 investors follow the “High Yield Landlord” approach to real estate investing.

We are ranked #1 in real estate for a reason: we put our money where our mouth is and show perfect transparency with our members.

Disclosure: I am/we are long WPG; UNIT; SNR; CBL; EPRT; BPR. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment