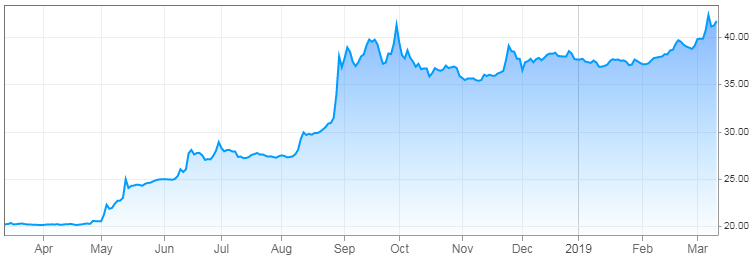

One of the market’s biggest winners during the past couple of months has been Mercadolibre (MELI). Often called the Amazon (AMZN) of Central and South America, the online retailer has seen its shares nearly double from its 52-week low seen back in December 2018. As the chart below shows, the stock broke $500 on Wednesday, but perhaps it’s time for investors to sell into this massive rally.

(Source: Yahoo Finance)

The first thing that concerns me is that the company just announced a large share offering, of which the $1 billion portion priced at $480 per share. This will help provide funds for future growth, but it dilutes investors a little bit and there’s a secondary portion to it. Some will argue that if the company is selling shares at $480, investors shouldn’t be buying more than $500.

Another curious item was a curious set of analyst notes out this week. Research firm BTIG reiterated its Buy rating on the stock on Tuesday, but had a price target of $450 on the name. That makes no sense, because the analyst was telling you to buy a stock that was expected to drop. However, the analyst then came out on Wednesday and raised the target to $535. Now the Buy rating makes sense, but it’s a strange set of events.

The second worry I have is with regard to the company’s second-largest market, Argentina. As you can see in the chart below, the US dollar has basically doubled against that country’s currency over the past year. Argentina is Mercadolibre’s second-largest market, representing more than a quarter of the company’s revenues last year. The more the dollar rallies, the worse the company’s reported results will be when translated into US dollars. The dollar also is up a bit against the Brazilian Real over the past year, which further hurts the situation. With the US economy doing fairly well now, emerging market currencies could weaken even more.

(Source: cnbc.com)

The other item that worries me is valuation. Mercadolibre is currently trading at roughly 8.4 times expected 2020 sales and more than 195 times next year’s earnings. Since the company is often compared to Amazon, the US giant currently goes for about 2.6 times next year’s sales and 42.8 times expected EPS. Yes, currently Mercadolibre is projected for higher revenue growth, but you are paying tremendously for that growth.

Amazon also just started direct sales of merchandise in Brazil in January, so competition is going to soar in 2019 for Mercadolibre. Since this year started, analysts have raised this year’s revenue estimate on MELI from $1.99 billion to $2.06 billion, which means expected growth of 43%. That could be tough to achieve with Amazon making its big push along with the dollar’s strength. At the same time, the average EPS estimate has gone from $0.50 to $0.30. When more revenues means significantly less profits, that means a hit to margins. EPS estimates may come down another tick in the coming weeks thanks to the secondary offering diluting investors, which lowers EPS.

With shares of Mercadolibre nearly doubling in the past couple of months, I think it’s time for investors to pump the brakes a bit. The company just sold stock below where shares currently trade, and why was an analyst reiterating a buy rating with a $450 target that was then raised a day later? With the Argentine Peso weakening against the dollar, 2019 results will be pressured, and Amazon has started its big move into Brazil. With a lofty valuation, those buying a bit above $500 might not have the best returns moving forward.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: Author’s additional disclosure: Investors are always reminded that before making any investment, you should do your own proper due diligence on any name directly or indirectly mentioned in this article. Investors should also consider seeking advice from a broker or financial adviser before making any investment decisions. Any material in this article should be considered general information, and not relied on as a formal investment recommendation.

Be the first to comment