Back in August of 2016, we wrote two articles (here about the DOJ decision and here about the DHS inquiry), highlighting additional risks in the for-profit prison industry following the decision by the Obama administration to phase out the use of for-profit prisons at the BOP. Since those articles were published, a lot has happened.

On the news of the BOP decision, GEO Group’s (GEO) stock plummeted. Then following Trump’s surprise election, the stock skyrocketed.

With a dividend yield of over 8% and a reasonable P/E of 18 (forward P/E of 15.6), GEO’s stock might look good at current levels. Despite the Trump administration’s decision to expand the use of for-profit prisons, we still think the company is a very risky bet.

GEO Group’s Problems Are Still Political

GEO Group’s biggest problems are still political. While Republicans – friendly to the private for-profit prison industry like the Trump administration – are in charge of the government now, they won’t be forever. The US political climate changes constantly. If Democrats regain control in 2020, it is not unreasonable to expect whoever wins to reenact the Obama-era BOP policy. In fact, many of the candidates in the 2020 presidential field are running to the left of where the Obama administration was in 2008-2016. Perhaps a reinstatement of the Obama BOP policy should be almost a given.

According to its latest financial filing, the GEO Group gets about 49% of its revenue from the federal government. All of the revenue comes from agencies (BOP and US Marshals under the DOJ and ICE under DHS) that fall under the purview of the executive branch and would be at risk if a Democrat wins in 2020.

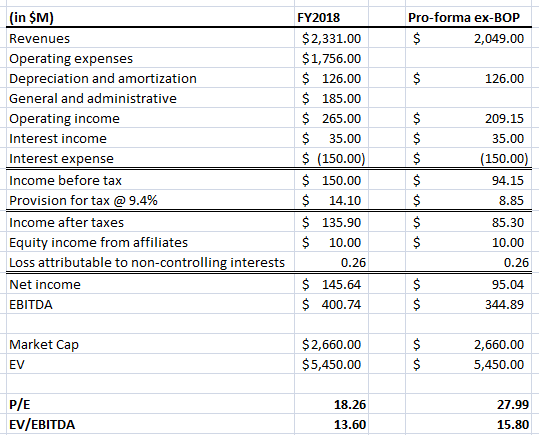

To understand just how big a financial impact there could be, let’s look at what might happen if the Obama-era BOP policy was implemented and GEO Group lost all its BOP revenue. While the policy was going to be implemented over time via non-renewals, it can still be instructive to look at GEO Group’s financials with and without the BOP.

The company gives us some idea of how empty beds affect its financials. In the 10-K, GEO discloses the following:

In the U.S. Corrections & Detention segment, we are currently marketing approximately 4,700 vacant beds at four of our idle facilities to potential customers. The annual carrying cost of these idle facilities in 2019 is estimated to be $17.3 million, including depreciation expense of $3.9 million. As of December 31, 2018, these facilities had a net book value of $126.0 million. We currently do not have any firm commitments or agreements in place to activate these facilities but have ongoing contact with several potential customers. The per diem rates that we charge our clients often vary by contract across our portfolio. However, if all of these idle facilities were to be activated using our U.S. Corrections & Detention average per diem rate in 2018, (calculated as the U.S. Corrections & Detention revenue divided by the number of U.S. Corrections & Detention mandays) and based on the average occupancy rate in our U.S. Corrections & Detention facilities for 2018, we would expect to receive annual incremental revenue of approximately $106 million and an increase in annual earnings per share of approximately $.15 to $.20 per share based on our average U.S. Corrections and Detention operating margin.

The midpoint of the EPS guidance converted to net income using the 120,241,000 average shares outstanding during the fiscal year comes out to a loss of around $21M on revenues of $106M or about a 19.4% net income margin. BOP contracts make up 12.1% of GEO’s FY2018 revenue. So, we can adjust the financials to show a pro-forma income statement without the BOP.

We can see that GEO Group goes from trading at 18 times earnings to a whopping 28 times earnings. It’s also interesting to note that net income would only be half of the $229M paid out in dividends in FY2018. Operating cash flow has been on average 43% greater than net income over the past three years, so even assuming the same net income to operating cash flow ratio, the dividend still may not be covered if the BOP contracts were to be lost.

It’s important to point out that the above analysis is meant to be a general guideline, not an exact prediction. The BOP contracts would likely be wound down with time, and the margin impact of a complete facility closure may (or will) be smaller than the margin impact of empty beds in existing facilities. However, the point remains that political changes could cause huge swings in GEO Group’s profits.

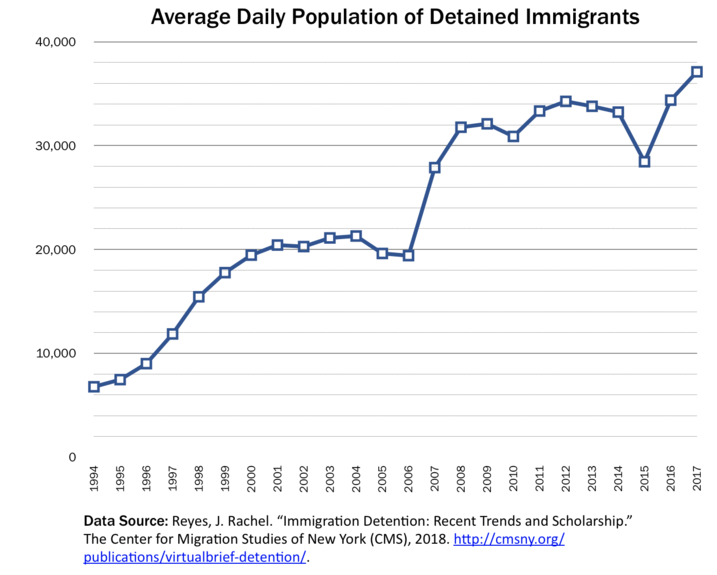

In fact, the ICE contracts may be an even bigger risk now that immigration issues have bubbled to the political forefront. Since 2001 (the earliest data is available), immigration detentions have steadily risen, culminating in a record 42,000 average daily detention in CY2018.

(Graphic source: Wikipedia via data from CMSNY)

The GEO Group gets 26% of its revenues from ICE contracts, its largest single “client”. If immigration detention levels returned to just their Bush-era levels, the financial consequences for the company could be significant.

Summary

The ever-changing political landscape makes GEO Group a risky stock to own. Every four years, there is the risk of a significant upheaval in the company’s business model. Even more discouraging is there is nothing the company or shareholders can really do about it. Even in other industries, such as consumer packaged goods, which are going through significant changes, at least troubled companies like Kraft (NASDAQ:KHC) or Kellogg (NYSE:K) can attempt to reinvent their products to appeal to a new generation of consumer tastes. GEO Group doesn’t have that flexibility. Prisons are good for imprisoning people and not much else. If Democrats take the presidency in 2020, GEO Group’s profits and dividend may be at risk.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment