In a blog post I wrote about six months ago, I informed my readers that I had started a long position on Cray Inc. (NASDAQ:CRAY).

The company’s shares were exchanged at around $21 in those days and they have performed quite well since then, passing through the stormy fourth quarter of 2018 with little or no turbulence and outperforming their market of reference.

Source: Yahoo Finance

The positive trend was in part due to the introduction, in the late October of last year, of “Shasta”: CRAY’s first exascale-class supercomputer and one of the first exascale projects in the supercomputers’ worldwide market. The U.S. Department of Energy already signed a program contract for the installation of Shasta’s technology that is valued around $150M (one of the largest contracts in CRAY’s history).

The firm posted its FY 2018 results a couple of weeks ago, reporting a growing top line that reached $456M (+16% YoY) and a stable gross profit at $130M, that means gross margin declined YoY of around 480 BPS from 34% to 29%.

This happened for two main reasons:

1. Only product revenue grew (+25% YoY) whereas service segment was flat and services have usually much higher margins (~ 50%).

2. Inside the products sold, the “cluster” portion was higher than usual and these systems, being more commoditized, tend to carry lower gross margins.

Net loss narrowed to $71M against $134M in 2017. Yet the improvement is only optical, because of a one-time huge tax expense of roughly $81M which occurred last year: without this item, net loss would have increased by 34% in 2018.

In fact, whereas total revenue registered healthy growth this year, gross profit did not move at all in comparison with 2017, staying flattish at $130M. At the same time, operating expenses grew. More specifically, G&A declined by 13% and only R&D and Marketing expenses increased, so overall we have an acceptable performance on the expense side, considering that the costs declined where it counts.

All in all, there are several positive developments on CRAY’s latest operations, as well as various worrisome signs: I will try to provide a short list of both.

Positives

Let’s start with the good news:

1. Customers’ orders are clearly accelerating. Leaving aside the DOE’s big contract previously mentioned, there have been other several new announcements, like this one, released straight after the Q4/2018 conference call. In fact total backlog strongly increased to more than $600M at the time of writing this: six months ago they were in the range of $460M. Shasta systems will hopefully add even more contracts in the quarters to come and we should also remember the “icing on the cake” (using CEO Peter Ungaro’s own words), aka the Coral-2project: another exascale contract sponsored by DOE. This is an upgrade of a previous contract named Coral-1, that CRAY and Intel (NASDAQ: INTC) had already won together. A confirmation of that win would easily mark another record among the company’s contract history.

2. Another positive development is the strong growing trend of the commercial market business that, as P. Ungaro reported, should stand now at roughly 20% of the company’s total sales ( an impressive high double digit yearly growth). This segment could be boosted even more by the “super computer as a service” initiative that CRAY started in 2017, consisting in providing access to supercomputing capabilities in a cost effective way, thought mostly for the smaller private clients, through the Microsoft (NASDAQ:MSFT)’s Azure Cloud network.

3. From the financial viewpoint CRAY looks healthy: free cash flow turned positive to $96M, primarily driven by a decrease in inventory and in receivables. Although that led to a decrease in the working capital (the most meaningful metric to valuate CRAY’s performance in generating cash) to $291M at December 31, 2018. The company has no debt and the current portion of its assets outpaces its total liabilities by more than two times.

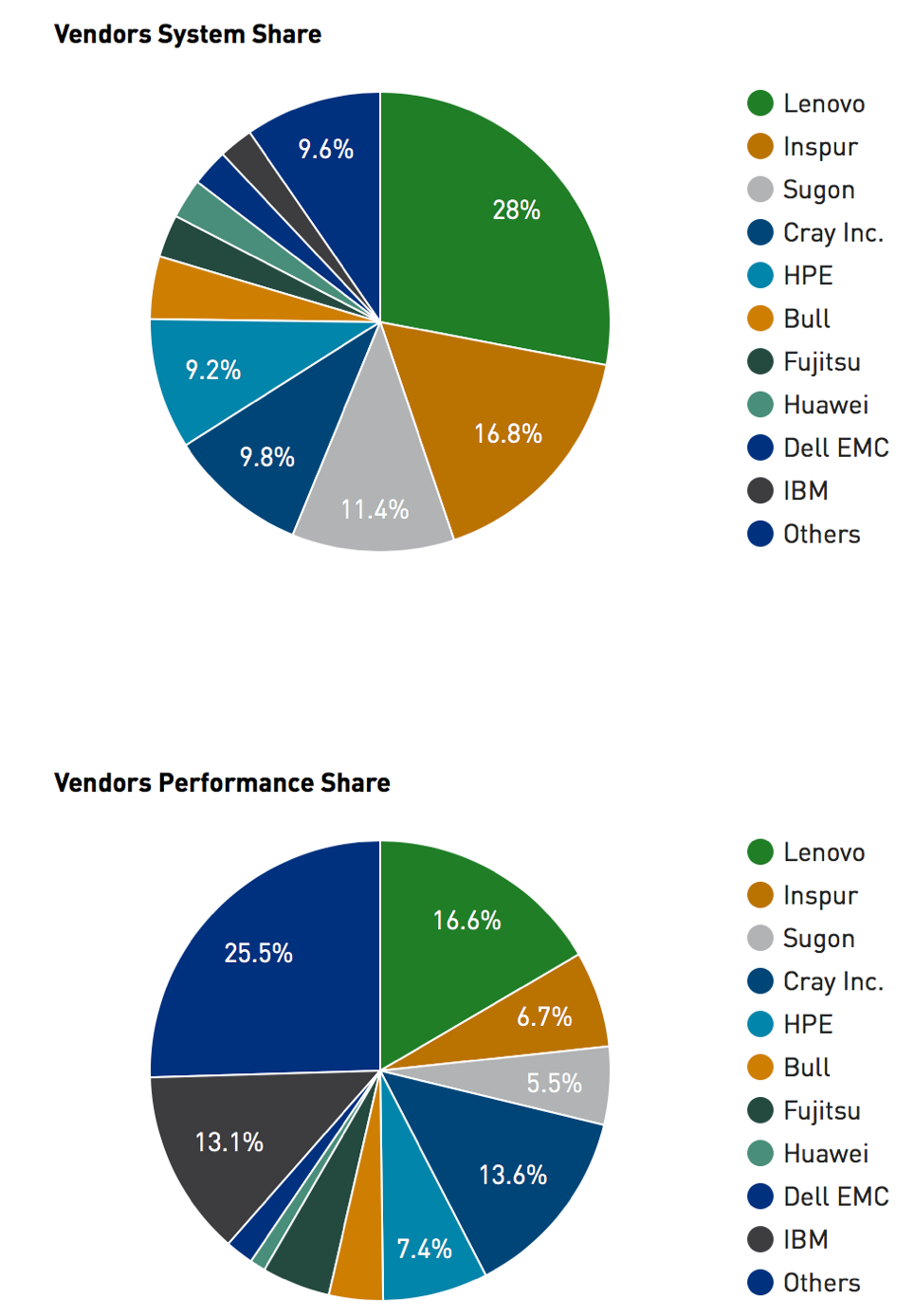

4. Moreover: the last November’s report of TOP500, that tracks the supercomputer market, shows how Cray stands at the fourth place if we consider the system share (9.8% of the total) and at the second place considering the performance share (13.6% of the total). It is a very competitive market but CRAY manages to defend its position every year among big competitors. This, given CRAY’s relatively small size (less than $1B at the moment), enhances the chances to be acquired by a much bigger company, interested in increasing its market share or willing to enter in the super computer arena.

Source: Top55.org

Negatives

1. As previously mentioned, CRAY collected a significant net loss in 2018. Even if we adjust the official number for a lot of non-cash items, we still remain with a cash net loss of $41.4M (source: CRAY’s form 10-K Annual Report). The working capital has been declining four years in a row, slowly but constantly (-7% yearly). And 2019 guidance is not calling for any robust inversion of this trend: overall this year is expected to be a transitional year with modest growth, as the company plans to begin shipping its Shasta systems. Probably there will be modest growth for total sales VS a strong booking activity. A lot will depend from the level of gross margin that means, in turn, the level of product revenue mix and the level of service revenue.

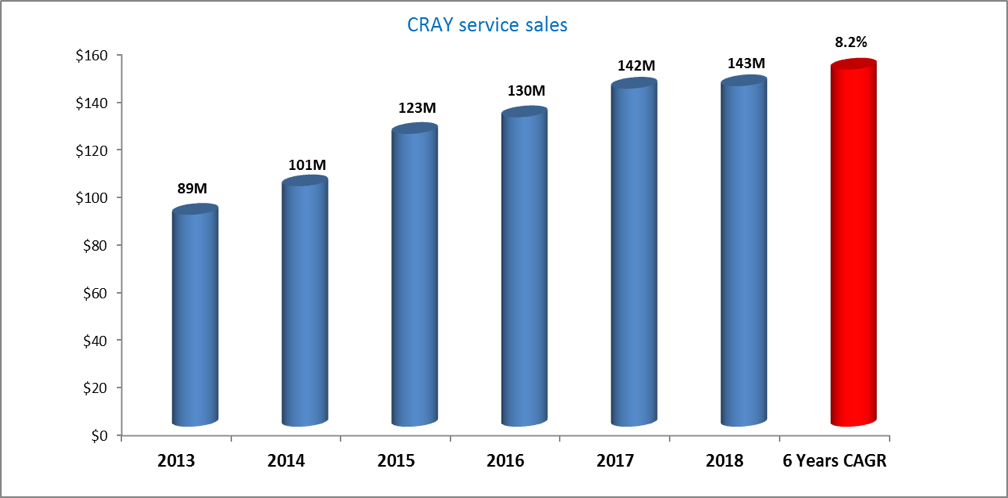

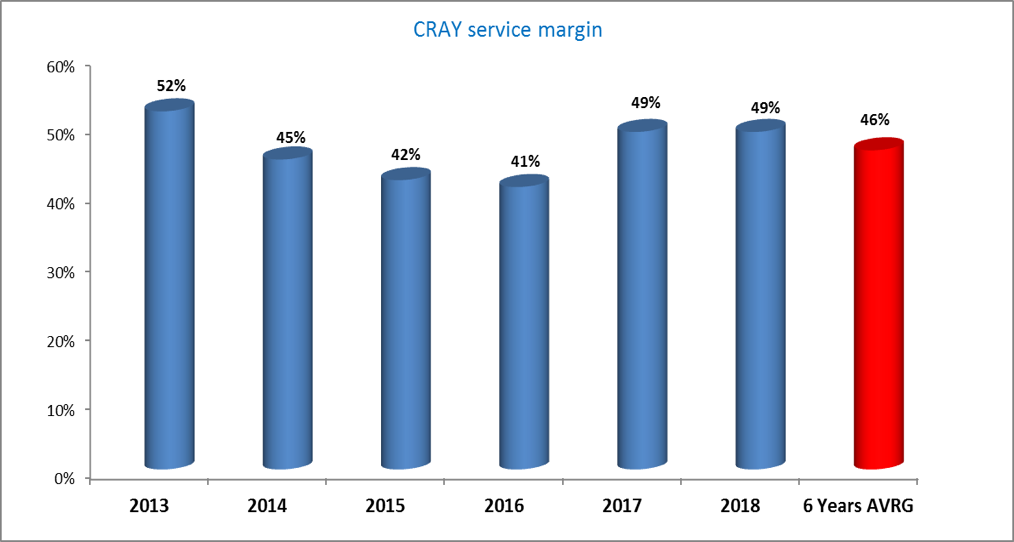

2. The Service segment has been particularly disappointing in 2018. In fact, one of the main reasons I am bullish on the long-term perspective of this company is the steady growth of its service segment, which brings higher margins and is structurally less volatile. Yet this year service stopped growing:

Source: Company report – Author’s elaboration. Data in Million dollars

Source: Company report – Author’s elaboration

Source: Company report – Author’s elaboration

3. Management will find it challenging to raise the gross margin without at least a double-digit growth of the service segment. And if margins remain low, how much should the company boost its top line in order to be profitable again?

According to its historical track record, in 2016 CRAY managed to report an operating income with total revenue of around $600M. Yet gross margin was around 35% that year, 600 BPS more than the firm’s poor performance in 2018.

P. Ungaro seems to confirm this line:

Aaron Rakers

Pete, I’m just curious as you kind of look at the model and understanding the variables in play here right now, but how do you define healthy profitability?

Peter Ungaro

…in quarter for us to really start to grow and become profitable again, we have to get our revenues up into the range that — where we left, I mean, the $700-plus million range. And we think that we can do that with the technology that we have and grow from there.

Thus, I think we may assume a conservative break-even top line of roughly $650M.

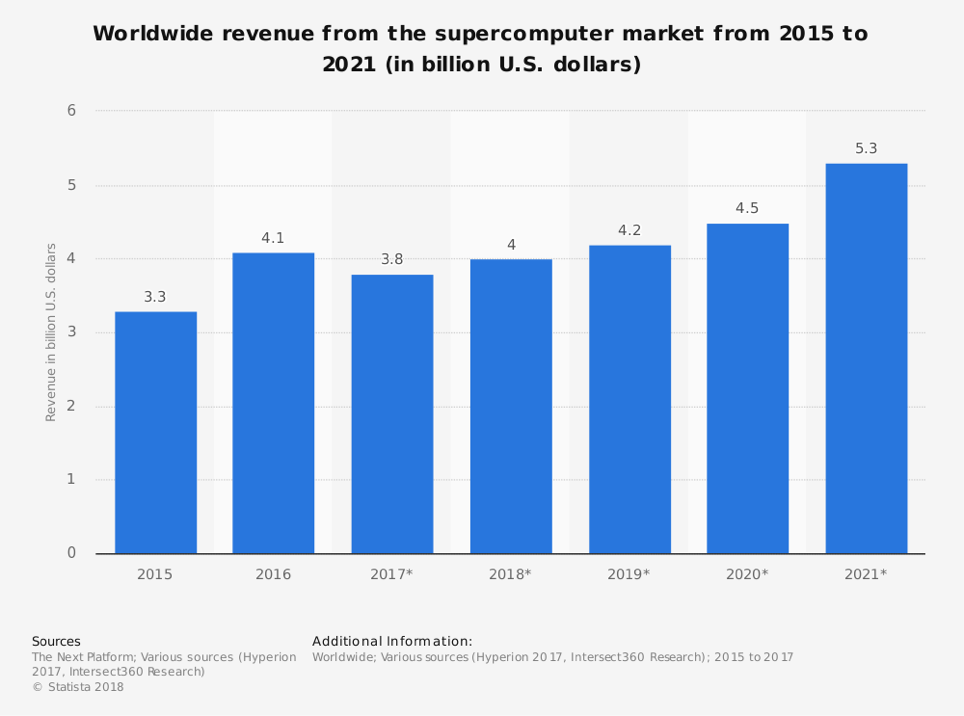

Even if CRAY’s CEO looks quite sure to achieve it, future is always uncertain and the present reality is that in FY2018 total sales missed that $650M target by more than 30%. This implies that the Seattle’s company must manage to outperform the supercomputer market in the next two years, when forecasts call for a 12% comprehensive growth. Otherwise we should wait until FY2021 to see a profit, according to this line of thoughts.

Source: Statista

Source: Statista

Takeaway for investors

Cray Inc. is an interesting company with solid long-term perspectives.

I suggested buying CRAY six months ago, when shares were traded at around $21: since then the stock performed considerably better than its benchmark.

Yet 2019 will be a transitional year for this firm and Mr. Market will probably provide better entry points, with lower prices for the ones who want to start a position on CRAY.

Anyway, I do not intend to sell my shares: I will rather hold and let other quarters roll on.

Disclosure: I am/we are long CRAY. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment