Plains All American Pipeline (PAA) has growth projects coming in the coming quarters that will bail out the struggling E&P industry, which is suffering from widening differentials, and will also keep dividend coverage of the company’s stock strong.

In addition, leverage is on the high side for PAA but is coming down and, more importantly, the company will be relying on cash flow to at least fund a portion of future work, and therefore, no dilution to shareholders will be necessary.

As a result, I continue to remain long pipeline players like PAA and continue to add to shares on market weakness.

PAA Has Growth Projects To Boost Revenue

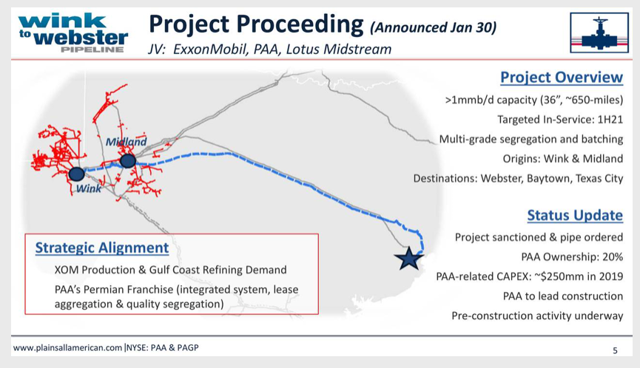

Plains All American has multiple catalysts to drive future earnings such as the 36″, 650-mile long Wink to Webster Pipeline, which is an LLC Joint Venture with Exxon Mobil (XOM) and Lotus Midstream, that will take one million barrels of oil per day from the Permian to the Gulf Coast. Source: Plains All American Pipeline

This event could lead to a significant improvement in differentials for E&Ps in the Permian, as relieving one million barrels from takeaway constraints accounts for a significant amount of production in the area. The pipeline is currently under construction and is expected to be in service by 2021.

PAA has other projects in the works, including the Cactus II pipeline, which will begin coming online in late 2019, Red River Expansion, which will add 100,000 barrels per day of takeaway capacity in Cushing, the Capline reversal, which will help in taking more volumes from Cushing to St. James, and Sunrise Expansion, which actually just came into service and will add another 300,000 plus barrels per day of takeaway capacity.

PAA even has some more gathering and terminal expansion projects taking place in the Permian that will be online in mid-2019. All of these measures will help further alleviate bottlenecks in the Permian.

Financials Remain Strong

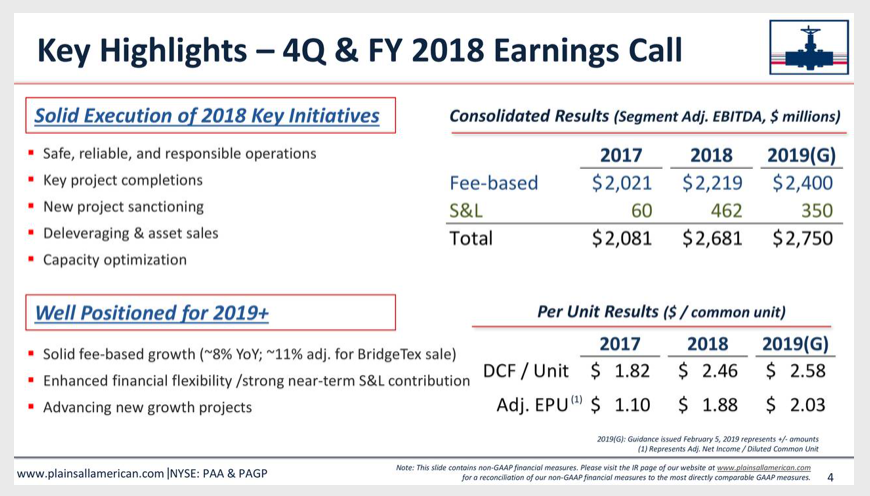

PAA reported solid fourth quarter and full year results for 2018. EBITDA was $949 million for the quarter, and $2.68 million for the year, which was $380 million higher than the previous estimates provided at the beginning of the year.

Additionally, net income per common unit of $1.88 vs. $.078 per unit at the beginning of the year, represented a 71% increase yoy for the company. Much of this growth in earnings was attributable to favorable differentials seen in North America, as well as the steady income that PAA’s fee-based business generates.

PAA also has numerous growth projects, as stated above, that will drive additional fee-based revenue going forward. Not only is a fee-based revenue model something income-oriented investors should applaud, but such an earnings model gives investors better visibility into future earnings as well.

Source: Plains All American

Distributable cash flow per common unit of $2.46 came in strong as well (seen above), and even exceeded guidance by 21%. 2019 should be an even stronger year, as the company expects to generate distributable cash flow per common unit of $2.58. DCF per unit should still rise looking past 2019, especially once the Wink to Webster pipeline comes online in 2021

For the record, instead of using coverage ratios like Energy Transfer (ET) or MPLX LP (MPLX) traditionally do, PAA prefers to use DCF because they feel it gives a better representation of their dividend coverage. Leverage remains high at 3.4 times, but I expect this number to come down once new projects are put into commission.

Dividend Coverage Risks Seen Mitigated

The risks facing PAA are environmental regulations, delayed court rulings, and lower oil prices from a slowing economy, which could lead to less volumes transported through their pipelines.

The bigger risk for PAA investors would be for the company to struggle from any of the above reasons, and therefore, have to cut their dividend at some point. Thankfully for PAA, the company has enough fee-based revenues coming from current and future projects that should provide the stability needed to sustain its dividend.

More importantly, because PAA is funding a portion of their operations through cash flow, debt should remain manageable, and having access to capital shouldn’t be a problem. Therefore, the company will no longer need to do any share offerings to raise capital, preventing further stock dilution from occurring.

Conclusion

Plains All American is bailing out E&P players who desperately need more takeaway capacity to come so that differentials can tighten again. This would allow margins to be sustained for E&Ps which, in turn, allows for more production and volumes to flow through midstream player’s pipelines.

This symbiotic relationship is truly a win-win for E&Ps, PAA, and the oil & gas industry as a whole. Furthermore, the work that Plains All American is doing for E&Ps will ensure stable cash flows for the foreseeable future, keeping their dividend coverage strong.

As a result, the bear market that energy stocks have been in since 2014 is presenting an attractive entry point for investors to go long, and PAA, due to its strong dividend coverage and stock appreciation potential, is a more prudent way to play an energy recovery.

Disclosure: I am/we are long AMZA. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment