Note: All dollar figures herein are in Canadian dollars.

Executive Summary

Aphria (NYSE:APHA) will release its earnings from Q2/19 (ending Nov. 30, 2018) on Jan. 11th at 7:00 am ET. This article is intended to provide a bit of a lens through which those earnings may be viewed.

I was on the fence about projecting this at all, because it’s so speculative, and this projection is, therefore, based on really limited information. The error range in this projection is extremely high, and I’d take this with a grain of salt.

The most important thing in Aphria’s earnings is going to be their recreational cannabis sales – both quantity and revenue. Other metrics still matter, but those metrics are presumably going to be roughly in line with the trends over the past few quarters. Meanwhile, recreational cannabis is an entirely new sector, and the sector that has made cannabis hot. Aphria’s market share in recreational cannabis, both now and even more so in the future, is extremely important for the value of the company.

Therefore, I will focus on recreational cannabis particularly. Other numbers are still important, but they are of secondary importance.

This projection takes quite a bit of calculation to get to, but is a very rough result. In the end, I project that:

- Aphria will sell ~2,800 kilogram equivalents of recreational cannabis in their November quarter.

- Aphria will sell ~4,600 kilogram equivalents total, including medical cannabis.

- Aphria will generate ~$26 million in net revenue during the quarter.

First, a bit of background on Aphria’s operating metrics and their past results.

Aphria’s Operating Metrics

Source: Aphria Q1/19 Earnings Release.

Last quarter, Aphria’s earnings release included the above table showing a variety of financial and operating metrics. All of these metrics are important, to varying degrees.

However, the notable thing about Q2/19 is that it will be Aphria’s first quarter that includes recreational cannabis sales. Cannabis was legalized in Canada on Oct. 17th, and Aphria will announce a quarter which ends on Nov. 30th.

Aphria’s Q2/19 revenue will include all sales that the company made to provincial wholesalers and other distributors prior to Nov. 30th. Thus, results will include both 1.5 months of retail sales (although Aphria only gets the wholesale revenue) and also sales for the cannabis that was still in wholesale or retail inventory at the end of Nov. 30th. As a result, the results will show revenue higher than “just” 1.5 months of retail sales, since results also include cannabis inventory at stores and distributors – both of which began the quarter without any inventory.

Aphria’s earnings will be only the second major cannabis earnings that include time when adult-use cannabis was legal in Canada. The first such earnings were from Hexo (OTCPK:HYYDF), whose earnings included two weeks of legal cannabis. As I described in Hexo: The First Two Weeks Of Recreational Cannabis – What We Learned, Hexo sold six times as much recreational cannabis as they had sold medical cannabis in the prior quarter and their revenue quadrupled. And that was only with two weeks of legality and three provinces of supply deals – Aphria will have six weeks of legality and has supply deals with all ten provinces and one territory.

With that in mind, the key sales metrics here, in my view, will be those that reflect how well Aphria is doing in recreational cannabis. I will primarily focus on Aphria recreational cannabis sales – both in dollars and weight. Other metrics are of relatively secondary importance.

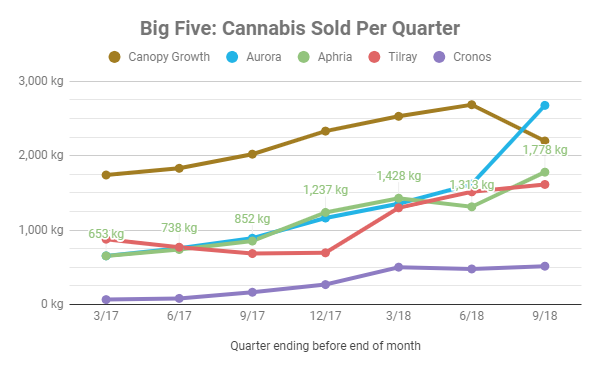

Past Results

Source: Author based on company filings

Cannabis sales: Last quarter, Aphria sold 1,778 kg of cannabis, good for third place among the top Canadian cannabis producers, behind Aurora Cannabis (OTC:ACB) and Canopy Growth (OTC:CGC). Notably, Aphria’s quarters end one month prior to the quarters of each of the other companies listed above – which is why Aphria’s earnings are arriving before its peers.

All of Aphria’s existing cannabis sales are medical cannabis. That will change in the coming quarter. Medical cannabis sales are likely to be ~flat while recreational cannabis sales are likely to be much higher than medical sales. Hexo’s cannabis sales are the best guide here. In the July 2018 quarter, Hexo sold 152 kg of medical cannabis. In the Oct. 2018 quarter, with two weeks of legality, Hexo sold 952 kg of recreational cannabis (and 158 kg of medical cannabis).

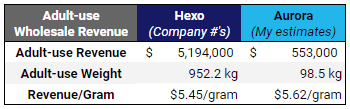

Cannabis revenue/gram: Here, I am specifically interested in Aphria’s recreational cannabis revenue/gram. Given that Aphria hasn’t previously sold recreational cannabis, it’s a bit of an unknown. In the above interview in Sept. 2018, CEO Vic Neufeld suggested that Aphria might realize revenue in the range of $5/gram for recreational cannabis.

This is slightly lower than the gross revenue earned by Hexo and Aurora, whose earnings report from Sept. 2018 included a tiny sliver of recreational sales:

Source: Author based on company filings; Aurora results based on tiny recreational sales in September quarter.

Notably, Hexo’s figures are gross revenue and include the cannabis excise tax. I discussed this excise tax in my recent article on Aurora, Aurora Lowers The Market’s Expectations, so I won’t repeat that discussion here. Suffice to say that Hexo’s net revenue is about $1/gram lower than that listed above.

Other Estimates: $21 to $40 Million

First, let’s look at projections from analysts and observers:

| Estimate From | Estimated Revenue | Via |

| Cornerstone Investments | $40 million | Seeking Alpha (Jan. 9th) |

| Analyst 1 | $20.7 million | Yahoo Finance (Jan. 9th) |

| Analyst 2 | $29.2 million | Yahoo Finance (Jan. 9th) |

| Analyst 3 | $35.7 million | Yahoo Finance (Jan. 9th) |

Source: Middle estimate from Yahoo Finance is inferred based 3 estimates with a known high, low, and average estimate.

There are three analyst estimates listed on Yahoo Finance, as of Jan. 9th, with a high of $35.68M, a low of $20.68M, and an average of $28.52M. Trivially, we can deduce that the third estimate is $29.2M based on the average. Meanwhile, my fellow contributor Cornerstone Investments has published a revenue estimate of $40 million on Seeking Alpha on Jan. 9.

I have also seen an estimate from GMP Securities, dated Dec. 28th, that Aphria will have revenue of $27.5 million in the coming quarter on 3,969 kg of cannabis sales. However, I am unsure if that estimate is still current, or if an updated GMP Securities estimate is one of the three estimates above. Thus, I didn’t include that estimate in the table, fearing that it might be outdated and duplicative information.

I Estimate Revenue of $26 Million on Sales of 4,600 kg

Projections are far more art than science. There will be a tremendous amount of hand-waving going on in this section. If my projections are anywhere near actual results, I will be pleasantly surprised and attribute it to luck.

My method for estimating here incorporates a lot of data points, and I’ll do the best I can to explain them. That said, it’s basically just a lot of trying to make sense from various information sources, many of which are often at odds with one another and point in opposite directions. But here we go.

Let’s start by looking at Aphria’s most recent quarter and comparing it to quarters from Aurora (OTC:ACB) and Hexo (OTCPK:HYYDF). The former is useful because they just provided us with revenue guidance and the latter is useful because they have announced results from a quarter that included legalization. Thus, both can provide a little insight into post-legalization Canadian cannabis results.

| Last Q (Pre-Legalization) | Aphria | Aurora | Hexo |

| Revenue (in $000s) | $ 13,292 | $ 35,800 | $ 1,410.7 |

| Cannabis Sales (medical) | 1,778.2 kg | 3,063 kg | 152.3 kg |

Source: Author based on company filings; Aurora’s revenue and sales are pro forma with the latter being inferred by the author and the former being announced by the company.

Above are results from the last quarter prior to legalization from all three companies. Not that Aurora’s cannabis sales listed here are my inferred pro forma results. Aurora’s reported sales were 2,676 kg equivalents of cannabis (equivalents because part of each company’s sales are cannabis oil and not dried cannabis). However, Aurora’s results only included a partial-quarter of MedReleaf results, as the MedReleaf deal closed in late July, and Aurora’s quarter began July 1st. Here, I am inferring additional sales based on past MedReleaf sales – which were 1,425 kg/quarter in MedReleaf’s last announced quarter prior to the purchase by Aurora.

A note on my coloring scheme here: Yellow cells in the table mean that I’m estimating or guessing at a figure rather than using company data.

Next, let’s take a look at the first post-recreational quarter for each company, and make a few inferences.

| First Q Post-Legalization | Aphria | Aurora | Hexo |

| Weeks of legalization | 6.43 | 10.86 | 2.14 |

| Total Revenue | $50M-$55M | $ 5,615.52 | |

| Rec Revenue | $ 18,200 | $ 4,242 | |

| Rec Sales | 4,086 kg | 952.2 kg | |

| Med Revenue | $ 13,292 | $ 35,800 | $ 1,421 |

| Med Sales | 1,778.2 kg | 3,063.0 kg | 157.5 kg |

Source: Author’s estimates based on company filings.

Each of Aphria, Aurora, and Hexo have quarters that end on a different day, with quarters ending on the last day of November, December, and October, respectively.

Hexo has already reported earning $5.6 million for its October quarter with recreational sales of 952 kg and medical sales of 157.5 kg. Medical sales rose slightly from the prior quarter. Hexo’s recreational versus medical revenue here is estimated because Hexo did not break down the proportion of excise tax paid on medical cannabis versus recreational cannabis. My estimate here is simply $1/gram of tax on recreational cannabis, which is probably marginally too high. My previous article on Aurora’s upcoming earnings goes into a bit more depth on excise taxes.

Aurora has provided guidance of $50 to $55 million of revenue for their December quarter. If we assume that medical sales will be approximately flat from last quarter, this implies $14 to $19 million in recreational cannabis revenue. The former assumption is a source of error – medical sales could go either up or down. Here, I have estimated Aurora’s revenue to be within their guided range, but towards the higher end of that range at $54 million.

Assuming that Aurora’s recreational cannabis sales are at ~the same unit price as Hexo, this implies that Aurora would sell 4,086 kg of cannabis in order to generate $18.2 million of recreational cannabis revenue.

I have similarly assumed here that Aphria’s medical cannabis sales and revenue will be ~flat from last quarter. As with Aurora, this estimate is a potential source of error, as sales are unlikely to be flat. Notably, Aphria’s medical cannabis sales grew a lot last quarter (from 1,313 kg to 1,778 kg), but revenue rose slower than volume due to a decline in prices (revenue rose from $12.0 million to $13.3 million).

Reminder: Inventories Needed to be Filled, too

The task here is simple: Estimate Aphria’s recreational cannabis revenue and sales volume.

To do that, I would first like to estimate how much cannabis Aurora is selling to end users each week. That might sound simple at first – wouldn’t that just be 4,086 kg divided by 10.86 weeks? The answer to that is no, at least as I mean the question.

At the start of the first post-legalization quarter, provincial distributors and cannabis stores had zero inventory. Those businesses were not open yet and had nothing in stock.

Meanwhile, cannabis companies recognize revenue when they sell their product to distributors or wholesalers. When that product is sold to end users isn’t especially relevant because recreational sales are not directly between the cannabis company and an end user.

Thus, cannabis sales for each company will include two components: (1) cannabis that is sold to consumers during the quarter, and (2) cannabis that is in the inventory of cannabis stores and cannabis distributors at the end of the quarter.

Thus, Hexo didn’t sell 952 kilograms of cannabis for only 15 days of use. Instead, some of that cannabis was still in inventory at the end of October. This means that Hexo’s run-rate sales will be lower than 952 kg per 15 days – their run rate sales won’t need to fill an inventory, but only to replace cannabis that is sold to end users. This is a slight oversimplification, given that proliferation of stores (each of which will need more inventory), but let’s roll with it.

Inventory Estimates

We will ultimately estimate Aphria’s recreational sales by estimating both their weekly cannabis sales to consumers and the amount of cannabis that will be in inventory (in cannabis stores and distributors – not Aphria’s own inventory) at the end of Aphria’s quarter.

Thus, I’d like to estimate weekly sales from Hexo and Aurora first, and then to estimate Aphria based on those weekly sales.

To do that, I will use the Government of Canada’s sales data from October 2018:

| October Inventory | October Sales | |

| Kilogram equivalents | 6,627.8 kg | 4,680.3 kg |

| Percentage of total cannabis sold | 59% | 41% |

Source: Author based on Government of Canada data with cannabis oil equivalent estimates as in my previous Aurora article.

The data I am using here is the same as I used in my previous Aurora Cannabis article – I recommend readers review that article if they want a bit more depth on this data. Notably, I am converting cannabis oil at a rate of 10 mL = 1 gram of cannabis and adding that to both the inventory levels or stores/distributors (as of Oct. 31st) and to the sales to consumers as of the same date.

Cannabis company sales for October (if they released such figures) would include both the 4,700 kg bought by consumers and the 6,600 kg sitting in inventories in stores and provincial distributors.

Thus, we can infer that Hexo did not sell its entire 952 kg of cannabis to end consumers. Instead, at first glance, we could estimate they only sold 41% this much to end consumers, and the remainder was used to stock stores.

However, I’m going to put my finger on the scale a bit here. Many provinces did not have supply shortages – they had reasonable supplies of cannabis, and so there was plenty of cannabis in inventory at the end of October. However, the 90% of Hexo’s sales were in Quebec. Quebec had such bad supply shortages that they were forced to close their stores three days/week – and that occurred in the October period we’re looking at.

Given Quebec’s terrible supply shortages, it is probable that Quebec sold more than 41% of the cannabis they purchased in the month of October. Otherwise, they wouldn’t have had to close stores, since other provinces didn’t have to close stores in the same way. Other provinces had some hiccups – but not nearly as severe.

Basically, this means that I think Hexo had less than 59% of their cannabis still in provincial inventory at the end of October. To pull a number from thin air, I will suggest that perhaps Hexo had 45% of their sold product still in inventory at the end of October. This estimate could be too high or too low. (If I lower this figure, it would push my estimate for Aphria’s sales up, and if I raise this number, it pushes my Aphria estimate down.)

|

Est. Inventory Levels and Sales |

Aphria | Aurora | Hexo |

|

October Inventory (stores and distributors) |

59% | ||

| Hexo’s est. inventory | 45% | ||

| Est. weekly sales | 308 kg | 244 kg | |

| Est. inventory at end of period | 740 kg | 429 kg | |

| Market Share | 13.5% | 10.2% |

Source: Author’s estimates.

At 45% in inventory, this suggests Hexo sold cannabis to consumers at a rate of 244 kg/week and that 429 kg of Hexo cannabis was in store/distributor inventory at the end of October. This, in turn, implies that Hexo has a Canadian market share of ~10%, based on my fourth quarter Canada-wide cannabis sales estimate (~30,300 kg in the calendar fourth quarter). Meanwhile, Aurora would have a market share of 13.5%, based on the same estimate (4,086 kg/30,341 kg).

Next, I assume that Aurora’s inventory (in stores/distributors) is proportionate to their market share (versus Hexo) but adjusted upwards by a factor of (59%/45%) because Aurora was not operating primarily in a low-inventory province. That is, I am assuming Aurora’s products will have an “average” inventory level at the end of their quarter whereas I was assuming that Hexo’s products would have a “below average” inventory level.

After estimating Aurora’s end-of-quarter inventory level, their weekly sales are then just all the remaining cannabis they sold divided by the weeks in the quarter, (3,346 kg/10.86 weeks). This results in weekly sales of 308 kilogram equivalents.

Estimating Aphria Sales Based on Aurora and Hexo Sales

I estimated to-consumer weekly sales here because Aphria’s quarter includes a different amount of legal cannabis sales than either Aurora or Hexo. Aphria’s sales will include both inventory levels at the end of November and to-consumer sales for 6.43 weeks of the quarter.

Given my estimates of weekly sales from Hexo and Aurora (244 kg/week and 308 kg/week), I can now estimate Aphria’s sales based on those figures. To estimate Aphria’s sales compared to those two peers, I will consider a few data points:

Source: Author based on various sources.

Here are a few data points we can use to determine the relative recreational sales between Aphria and Aurora and Hexo.

Aurora has provincial supply deals (between both Aurora and MedReleaf) which cover 89% of Canadians. Of those deals, deals covering 54.5% of Canadians do not describe a quantity of cannabis while the deals covering the other 35% of Canadians suggest annual sales of 71,000 kilogram equivalents. Aphria’s provincial deals (excluding private deals) suggest sales of 22,250 kg/year, with deals covering nearly every Canadian. This metric perhaps suggests that Aphria’s sales will fall between those of Hexo and Aurora.

I have previously conducted a study of “shelf space” market share. This is basically a population-weighted count of how many different products each supplier had in the most populous Canadian provinces. There, I found that Hexo had a 7.4% share, Aurora a 10.5% share, and Aphria a 9.5% share. This metric again suggests that Aphria’s sales will fall between those of Hexo and Aurora.

BNN Bloomberg has published data on cannabis market share in both Nova Scotia and Prince Edward Island over the first month of legalization. In that data, Aphria slightly outsold Aurora in both provinces. These are both small provinces, however. Hexo does not have supply deals in either province – their products are not on sale in Nova Scotia or Prince Edward Island. This metric suggests Aphria’s sales may be slightly higher than those of Aurora.

I have previously published research on Ontario cannabis sales from Ontario’s online cannabis platform. This data spanned a period in late October and early November, before the province removed the ability to access this data (which was available via an API on their Shopify-powered (NYSE:SHOP) platform). In that data, Aurora had massive market share in Canada’s largest province – and the province that purchased the most cannabis in October. This metric suggests Aurora’s sales may be much higher than those of Aphria.

Finally, I have also included analyst estimates from Yahoo Finance. The estimates on Aurora are already dated, given Aurora’s updated guidance. That said, I have included that data here because analysts’ Aphria estimates are likely based on the same data set as their Aurora estimates. That is, if the Aurora estimates are systematically too high, it’s likely their Aphria estimates are also too high. As shown in the estimates, analysts expect Aurora to sell roughly twice as much recreational cannabis as Aphria.

Now Some Hand-Waving

As shown, our various data points on Aphria and two of its peers point in different directions. Some factors suggest Aphria might outsell Aurora (Sales in NS and PEI) while others suggest Aurora could outsell Aphria (ON sales and shelf space market share).

To guess which factors might mean the most, I singled out two specific factors that did a reasonable job at “predicting” the sales proportions between Aurora and Hexo: Provincial supply deals as a percentage of Canadians and shelf space market share.

Notably, each metric provides a “national” figure – making it a useful predictive device. Further, the ratio between Aurora and Hexo approximated their estimated sales fairly well.

The former metric describes the potential market size for each cannabis company. Consumers in a given province can only buy a company’s cannabis if that company has a supply deal in their province. The latter metric describes how “visible” each company will be to a random Canadian, based on product availability and population distribution. The ratio between both metrics correlate well with my estimates of market share and weekly sales for Aurora/Hexo.

Thus, I’ll use the same metrics to estimate Aphria’s sales.

| As a percentage of Hexo’s Figures | Aphria | Aurora |

| Estimated Weekly Sales | 131% | 126% |

| Estimated Market Share | 133% | |

| Supply Deals covering % of Canadians | 134% | 119% |

| Shelf-space market share | 128% | 142% |

Source: Author’s estimates based on the above data, with 131% being what seeds my Aphria estimates below.

Singling out these two factors, Aurora’s supply deals cover 119% as many Canadians as those of Hexo (89.1%/74.7%). Aurora’s shelf space market share, meanwhile, is 142% as high as that of Hexo (10.5%/7.4%).

These two estimates were relatively close to Aurora’s weekly sales estimate compared to Hexo of 126% (308 kg/244 kg) and to Aurora’s market share compared to Hexo of 133% (13.5%/10.2%).

Averaging the same two metrics for Aphria – still as a percentage of Hexo – I estimate that Aphria’s weekly cannabis sales to consumers will be 1.3x as high as those of Hexo. I then further assume that Aphria’s inventory levels (compared to weekly sales) will be about the same as Aurora’s. That is, both Aurora and Aphria will end their respective quarters with an “average” amount of product on store shelves and at provincial distributors.

Putting it all together

|

Est. Inventory Levels and Sales: |

Aphria | Aurora | Hexo |

|

October Inventory (in stores and distributors) |

59% | ||

| Hexo’s est. inventory | 45% | ||

| Est. weekly sales | 320 kg | 308 kg | 244 kg |

| Est. inventory at end of period | 769 kg | 740 kg | 429 kg |

| Market Share | 14.0% | 13.5% | 10.2% |

Source: Author’s estimates based on the above data.

This is the same table as above, but with Aphria’s estimates filled in. Market share here is based on the 30,341 kg equivalents in the calendar fourth quarter, with Aphria’s sales estimated based on the weekly sales and their ending inventory level.

Notably, this estimate implies that Aphria will have a higher market share than Aurora. That is, in my view, a very aggressive estimate.

| First Q Post-Legalization | Aphria | Aurora | Hexo |

| Weeks of legalization | 6.43 | 10.86 | 2.14 |

| Total Revenue ($000s) | $ 25,884 | $50M-$55M | $ 5,616 |

| Recreational Revenue | $ 12,592 | $ 18,200 | $ 4,242 |

| Recreational Sales | 2,827 kg | 4,086 kg | 952.2 kg |

| Medical Revenue | $ 13,292 | $ 35,800 | $ 1,421 |

| Medical Sales | 1,778 kg | 3,063 kg | 157.5 kg |

Source: Author’s estimates in yellow.

Based on Aphria’s estimated weekly sales of 320 kg/week and an estimate end-state inventory level of 769 kg, along with a quarter that includes 6.43 weeks of recreational cannabis sales, I estimate that Aphria will sell ~$13 million of recreational cannabis, selling ~2,800 kilogram equivalents.

If we assume flat medical cannabis sales and revenue, this implies total revenue of ~$26 million and total cannabis sales of ~4,600 kilogram equivalents.

Thoughts

As I said before, this estimate is extremely speculative. If it’s close to correct, I will be pleasantly surprised.

Nearly everything about this estimate could be questioned and alternative estimates could be used. For example, I have estimates Hexo’s end-of-October inventory level (in stores and distributors) from thin air at 45%. If I had used 30%, my revenue estimate for Aphria – all else equal – would be $28.5 million, and if I’d used 60%, my revenue estimate would be $23.2 million. That single, seemingly-inconsequential change alters a lot.

Similarly, I am estimating national inventory levels based on very little information. Specifically, Aphria and Aurora are both likely to have much larger inventories in stores and provinces than Hexo. Both brands are available far more broadly than Hexo’s products, which are really only sold in Quebec with scant few products available in Ontario or British Columbia. (Although Hexo’s investor relations recently told me that more products may come to Ontario soon.) Here, a higher required inventory level would mean more sales for Aphria – they’d need to stock that inventory in this quarter and future quarters.

Virtually, everything else I said above is also open to speculation as well in much the same manner. Changing small variables can have a large impact on the model. Take it with a grain of salt.

All that aside, I estimate that Aphria’s revenue this quarter could total ~$25 million and that Aphria may sell ~2,800 kg of recreational cannabis.

We will find out on Jan. 11th at 7:00 am ET.

Happy investing!

Members of The Growth Operation, my cannabis newsletter community, receive:

- Daily run-downs of breaking cannabis news – including news on both U.S. and Canadian cannabis producers.

- Exclusive access to my in-depth research articles cannabis companies and the cannabis market in the United States and Canada.

- Access all my past Seeking Alpha articles – even back-articles that are no longer free.

- Free trials are available all month.

Disclosure: I am/we are long APHA, CGC, HEXO. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment