Investment Thesis

In my last article titled, Generating Income And Limiting Risk – Strategies To Create A Balanced Portfolio And Boost Income, I discussed a couple of methods for assessing risk in a dividend growth investor’s (DGI) portfolio. In the comments section, it was brought to my attention that a few retirees were interested in discussing the impact of Required Minimum Distributions (RMDs) on their Traditional IRAs and whether or not a DGI portfolio would be compatible with these requirements.

The purpose of this article is to discuss why retirees need to avoid costly mistakes when it comes to forgetting or miscalculating their RMD. Additionally, I want to explore a few scenarios where we look at how a bear, flat, or bull market can impact a retiree’s RMD and why a DGI portfolio provides an advantage that retirees should consider.

Why RMDs Matter

In the past, I have always explained RMDs on Traditional IRAs, 401Ks, SEP IRAs, and 403Bs as the government collecting their paycheck providing years of relief on tax returns. Because these types of accounts are tax-deferred, the government wants to make sure that it is getting its taste, because if there was no RMD provision, it is likely that a number of investors would continue to sit on that money in an effort to avoid paying taxes.

RMDs are becoming more common because the baby-boomer generation was the first to begin shifting from a pension-based system to one that is primarily made of Traditional IRAs and 401Ks. It should also be noted that Roth IRAs are not subject to an RMD because the retiree who holds these accounts have already paid taxes on the money they put into it. Roth IRAs are much less common due to the fact that they weren’t established until 1997 and have income limitations whereas Traditional IRAs have no income limitations.

The first RMD calculation begins for anyone who hits the age of 70.5 before April 15. There are a few exceptions to this rule:

- Anyone who continues to work beyond the age of 70.5 is able to continue deferring RMDs until the year in which they retire.

- Anyone who turns 70.5 and has a spouse or beneficiary that is more than 10 years younger than they are may be qualified for reduced RMDs.

- If the person in question is 5% or more owner in the business sponsoring the retirement plan, then they must begin making RMDs at the normal age of 70.5.

For those interested in seeing how the government calculates an RMD, I would recommend the following link for the IRS website. I will be providing several examples later in the article that explores how these calculations might impact your IRA.

The penalties for failing to make an RMD is extremely harsh and far exceeds anything that the retiree would have paid in taxes if they had made the withdrawal. Currently, retirees who fail to meet their RMD is hit with a 50% penalty on the total amount of the RMD. For example, an RMD at age 70.5 on $250,000 is approximately $9,124.09, which means that if a retiree failed to meet this requirement, they would be assessed with the penalty of $4,562.05.

The same penalty applies to retirees who withdraw funds from their Traditional IRA but fail to meet the minimum amount. Let’s assume a retiree withdrew $5,000 and all other variables remain the same as the previous paragraph. A retiree would be assessed with a 50% penalty on the difference between their distribution and the RMD amount. Therefore, the IRS would say that the retiree in question is subject to a penalty of $2,062.05 since that is 50% of the difference (($9,124.09-$5,000.00)*.5).

Simply put, the government makes it worth your while to take your RMD because if you don’t the penalty will be significantly more than any tax bracket you fall into.

Calculating An RMD

As a retiree gets older, the IRS increases the RMD and this calculation is based on life expectancy (their goal is to limit the total amount you will have in these tax-sheltered accounts by the time you die). The RMD is calculated based on the account balance on the final market value on December 31st.

To calculate the RMD amount, you will also need to know what the IRS Distribution Factor (DF) is for your age. For instance, at age 70.5, the IRS DF is 27.4 for all individuals (unless you qualify for reduced or deferred distributions that meet the IRS exception criteria). This means that you will divide your total market value on December 31 by 27.4 in order to calculate your RMD. Here is an example of what this looks like at for different year-end balances.

| Age | IRS Distribution Factor | Amount | RMD |

| 70.5 | 27.4 | $ 100,000 | $ 3,649.64 |

| 70.5 | 27.4 | $ 150,000 | $ 5,474.45 |

| 70.5 | 27.4 | $ 200,000 | $ 7,299.27 |

| 70.5 | 27.4 | $ 250,000 | $ 9,124.09 |

| 70.5 | 27.4 | $ 300,000 | $ 10,948.91 |

Source: Consistent Dividend Investor, LLC.

Advantages of A DGI Portfolio On RMDs

My primary issue with RMDs is when retirees attempt to satisfy this amount by selling shares of stock (since selling shares for less than what they were purchased for can have a major impact on their portfolio). By the same token, this can have a tremendous benefit for retirees in the event of a bull market since it offers the opportunity to sell shares for more than they were purchased for. In my last article, I discussed that one of the risks I want to avoid at all costs is being forced to sell stock at the worst possible time to satisfy my distribution/RMD. A DGI portfolio is a way to compromise between generating enough dividend income to cover all (or at least most of the RMD) for the first two decades of retirement. By covering the RMD via cash flow from investments (dividends and distributions), we are able to better protect our investment capital.

I have created a few scenarios to explore the potential implications of creating a Traditional IRA that is primarily focused on DGI stocks. I am attempting to answer the following questions:

- How many years can the dividend income satisfy the RMD amount?

- What is the minimum yield we would need to cover the RMD starting at age 70.5?

- What dividend growth rate would we need to achieve in order to maintain pace with increasing RMDs?

Because I can only control for so many factors, I’m going to make the following assumptions:

- The value of the portfolio remains static (except for the bear/bull market scenarios) for the entirety of this exercise and only grows if the RMD is less than the dividend income produced (all dividends collected as cash).

- We are assuming a retiree is only withdrawing the exact amount of the RMD (unless specifically stated otherwise).

- Since dividends are not reinvested, the only growth in dividend income comes from increased dividend payouts.

I have decided that a $250,000 portfolio is a reasonable size (any portfolios larger/smaller will scale from here since the reduced RMD will be comparable to the reduced dividend yield).

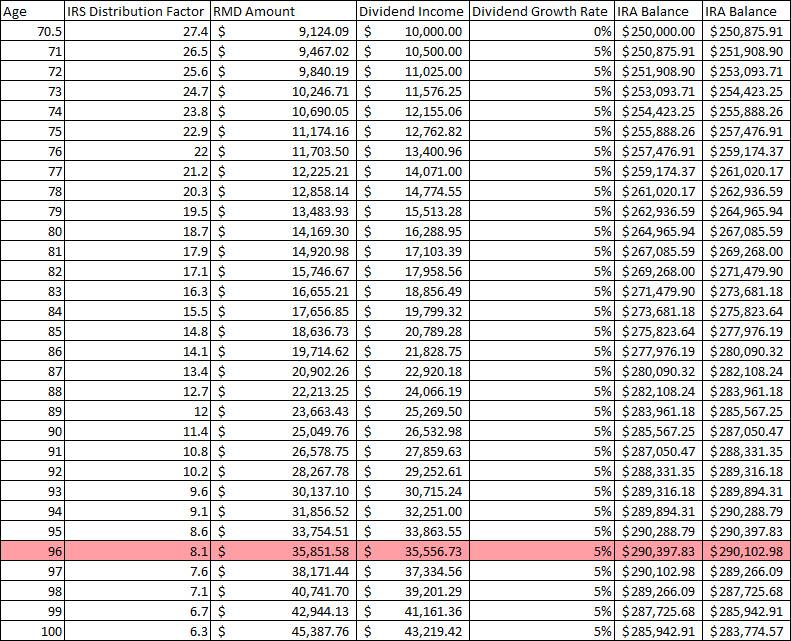

Example #1 – 5% Yield With 5% Growth

Source: Consistent Dividend Investor, LLC.

A portfolio yielding 5% on $250,000 would receive $12,500 of dividend income in its first year. With a balance of $262,500 on December 31st, we would expect an RMD of $9,580.29. As a retiree, this situation is extremely beneficial because we are earning more income than the IRS is requiring us to take an RMD.

This trend doesn’t just apply to the first year of retirement, it actually continues until age 98 when the RMD becomes greater than the income being generated by investments. In other words, a retiree with similar circumstances who is only withdrawing the exact amount of the RMD has the potential to live off the income created by those investments alone until the age of 98! At 98 they would still have significant assets to where they could live off the dividends and would have built a cushion of $100k in cash which means they would still be able to meet their RMDs without the need for selling stock.

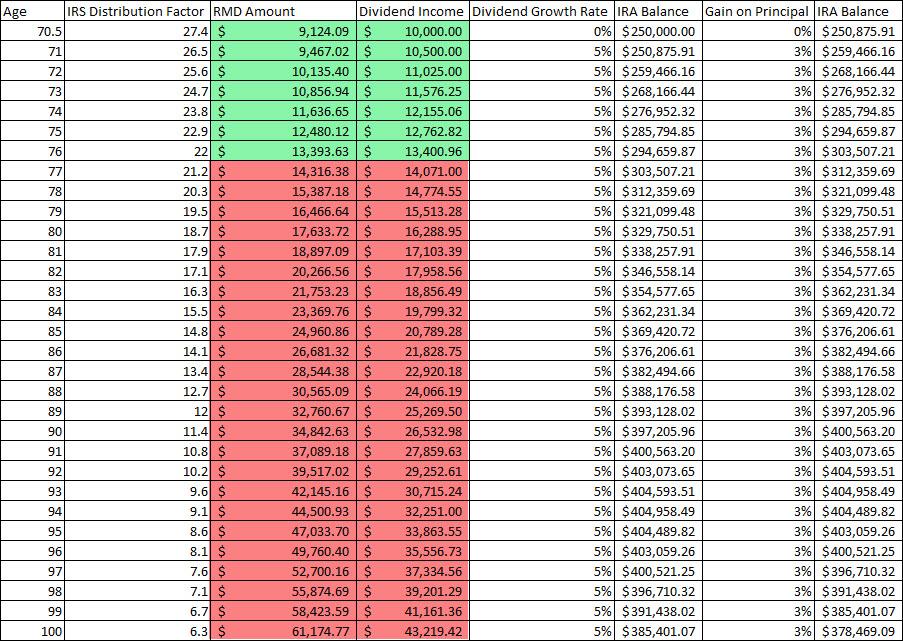

Example #2 – 4% Yield With 5% Growth

I agree that a 5% starting yield might be excessive, especially if we are considering a retiree who builds a rock solid portfolio of companies like 3M (MMM), Hormel (HRL), PepsiCo (PEP), etc. so I thought a portfolio with an initial 4% yield would be more realistic.

Source: Consistent Dividend Investor, LLC.

A portfolio yielding 4% on $250,000 would receive $10,000 of dividend income in its first year. With a balance of $250,000 on December 31st, we would expect an RMD of $9,489.05. Although the dividend income is significantly less than the $12,500 we would receive if the average yield was 5%, we are still earning more income than the IRS is requiring us to take an RMD.

Similar to Example #1, we continue to earn more income than the RMD until the age of 95. One major difference is that the lower starting yield cuts into our IRA balance significantly since there isn’t as much excess dividend as there was when the yield started at 5%.

Even with negatives considered, what I find so compelling about Example #2 is that it demonstrates how an investor who desires safety can also live on the income generated by their investments and is able to satisfy the RMD for at least the first 25 years of retirement.

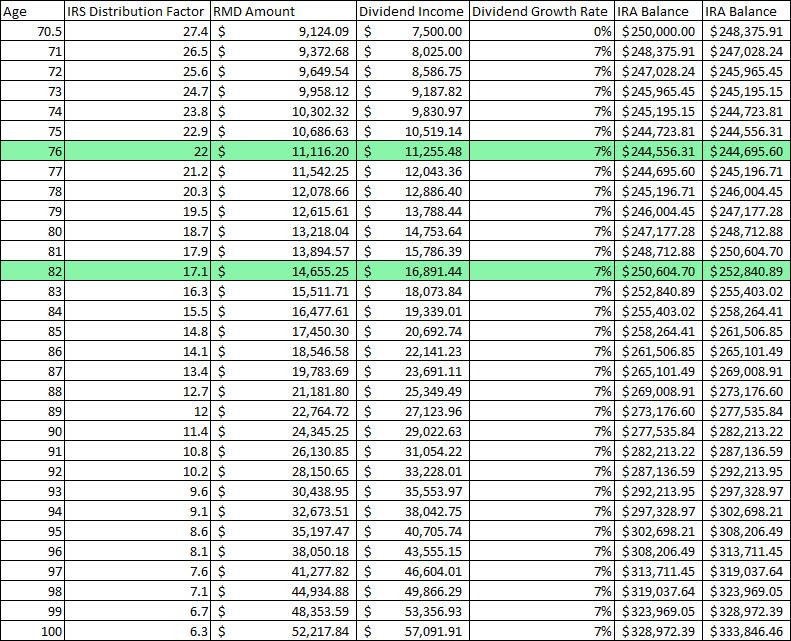

Example #3 – 3% Yield – 7% Growth

Let’s assume you have only recently established a DGI portfolio that has only the highest quality stocks in it, as a result, the yield is lower than normal but the prospects of growth are high. I would picture this portfolio consisting of stocks like Boeing (BA), Apple (AAPL), Microsoft (MSFT), Walmart (WMT), etc.

Source: Consistent Dividend Investor, LLC.

In this scenario, it is important to consider the following:

- This investor starts off by being forced to sell a small amount of stock to meet the RMD from age 70.5 to age 76. At age 76, this trend will reverse as the retiree’s dividend income will exceed the RMD.

- Since stock will need to be sold to meet the RMD, we need to consider that dividend growth in the first few years might be lower than what is shown. Because of this, a retiree would experience some dilution during the first 6-7 years of withdrawals.

- By age 82, the retiree will have generated enough dividend income in excess of the RMD so that the IRA balance will be back to the level it originally started at.

A retiree in this scenario would see the dividend income generated to be sufficient to cover the RMD until the age of 109. At the age of 109, the retiree would have $100k in liquid cash available in their IRA (since they are not reinvesting this cash) that would be used to cover the difference between the RMD and the dividend so that they would not have to sell any shares.

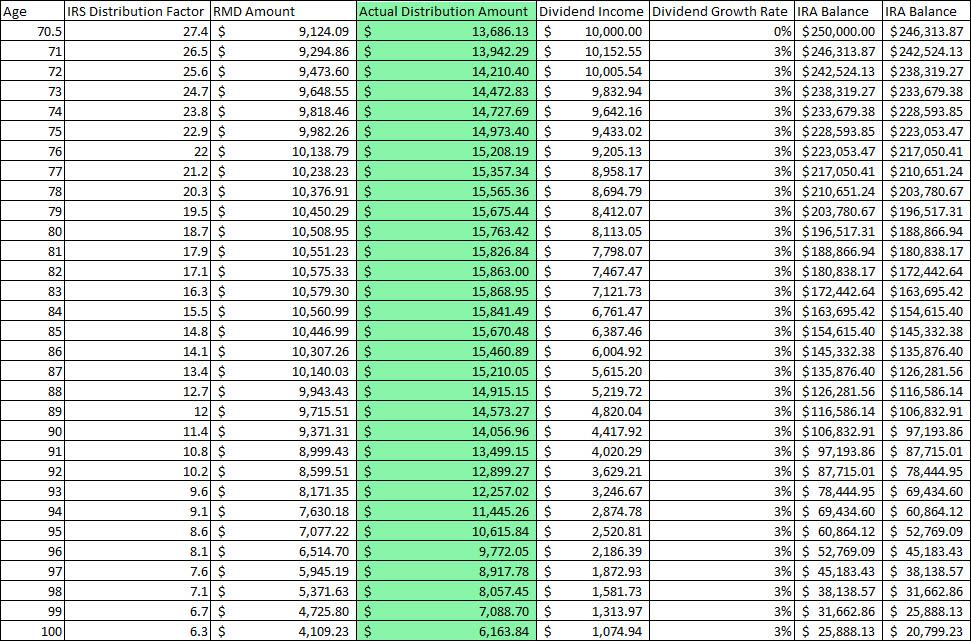

Example #4 – 4% Yield – 3% Growth – 1.5x RMD

In the first three examples, we explored what would happen in a DGI portfolio if a retiree were to only withdraw exact amount of funds to satisfy the RMD. Realistically speaking, most retirees will need more income than the RMD amount in order to support their lifestyle. I chose to use the middle-ground portfolio when it comes to yield and dividend growth. In order to account for the need to sell shares to generate enough income to cover the 1.5x RMD Distribution, I am using a 3% dividend growth rate instead of 5% since this will help account for some of the dividend dilution that should help consider the negative impact that comes from selling shares.

Source: Consistent Dividend Investor, LLC.

In this scenario, it is important to consider the following:

- In order to have enough funds to pay 1.5x the RMD, the retiree would be forced to sell shares every year. This is why the dividend income continues to fall after age 71.

- By taking a larger distribution than the minimum RMD, the retiree is subjecting themselves to significantly more risk and limiting how much money they will have available later in their retirement.

- The RMD peaks at a little over $10,500 in the retirees’ early 80s and continues to drop thereafter because the principal IRA balance begins to rapidly deteriorate. Since the RMD amount is based on the IRA balance, it remains much lower than in other scenarios due to the significant deterioration of the principal.

By following this method, a retiree can still live a very comfortable retirement even though their total balance will be nearly gone by the time they hit 100 years old.

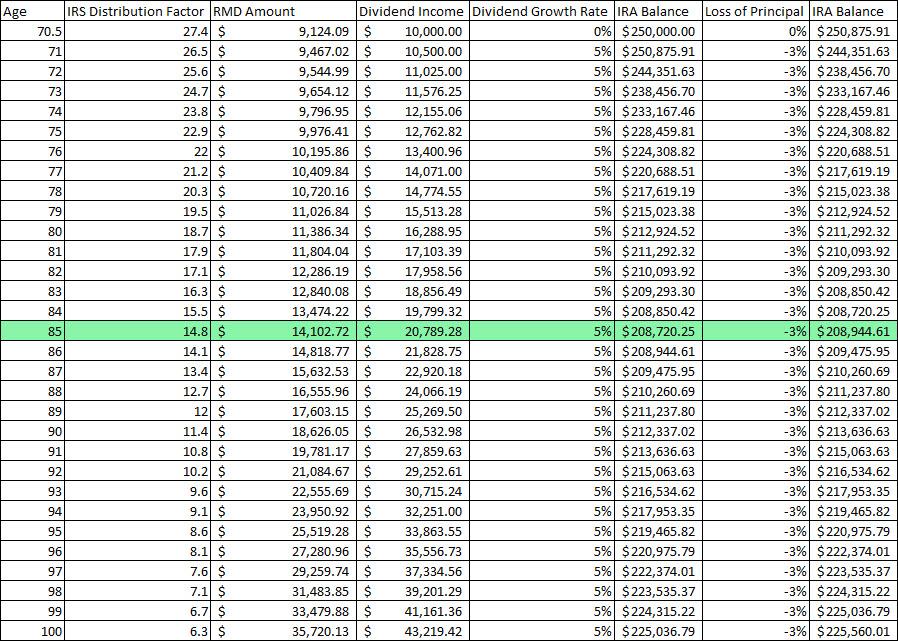

Example #5 – 4% Yield – 5% Growth – Bear Market Impact

In this example, we take the same scenario from Example #2 and apply an adjustment of -3% annually on the remaining IRA balance in order to see how it impacts our RMD. This scenario is meant to help retirees understand that as long as the dividends are coming in that there should be no loss of income since the decline in market value would have no direct impact on the dividend income being generated.

Source: Consistent Dividend Investor, LLC.

In this scenario, we need to consider the following:

- We do not discount the dividend rate as the IRA balance declines since we are not selling shares (which would dilute our future dividend).

- The decline of principal eventually levels out around age 85 assuming the retiree in question is only withdrawing their RMD amount.

- Because of the growth of the dividend (which has significantly outpaced the growth of the RMD), a retiree would see their IRA balance begin to recover after the age of 85.

- Because of the continuous -3% annual hit to the IRA balance, the RMD amount is actually reduced when compared to the same 4% Yield – 5% Growth scenario (Example #2). The RMD at age 100 would be $35.7k in this scenario versus $45.4k in Example #2.

Example #6 – 4% Yield – 5% Growth – Bull Market Impact

In the last scenario, I want to explore what the impact would be if we consistently saw 3% gains every year after a retiree turns 70.5 years-old. Although the scenario like this is highly unlikely, what I am more interested in is how improving market value impacts the RMD.

Source: Consistent Dividend Investor, LLC.

In this scenario, we need to consider the following:

- Although the principal balance is increasing significantly, this has no impact on the dividend income stream because we are only collecting additional dividends as cash and the increased value of stocks in the portfolio is only realized in the event that they are sold.

- The dividend income stream in this example is the exact same as the dividend income stream in Example #5 even though they represent different bear/bull market scenarios.

- The RMD in this scenario increases much more rapidly due to the growing balance in the IRA. The RMD exceeds the dividend income when the retiree turns 77. Due to the fact that there are too many variables, I did not attempt to show the impact of dilution from selling shares to fully cover the RMD.

Conclusion

Although the six examples above are not exhaustive, I believe that they provide important insight that validates some of the principles we already knew. By taking the time to walk through these examples, I was able to gain a better understanding of my own about RMDs and how the circumstances change relative to initial yield, dividend growth, IRA balance, and bear/bull market conditions.

If there are only a few things to take away from this article, it is the following:

- Dividend growth potential is vastly more important than a high starting yield that exhibits no growth. A portfolio may suffer in the early years due to low yield but will pay off in the long-run by providing a dividend stream that will quickly rebuild cash reserves. Companies that fit this description are also safer and typically have wide moats that make their business difficult to replicate and are therefore the safest entities to invest in.

- Only taking your RMD, in the beginning, allows a retiree to preserve/grow account balances during some of the most important years. The long-term value of a retiree’s IRA would be crippled if larger than necessary withdrawals are taken during the beginning of retirement. (See Example #4).

- A DGI portfolio that follows the parameters used will demonstrate the same dividend income stream regardless of whether it is a bear or bull market. At the same time, the RMD during a bear market will decrease because the total IRA balance will be decreasing (the dividend continues to be paid so long as no shares are sold). During a bull market, the RMD will continue to increase because the total market value of the IRA will continue to grow.

- Collecting the excess dividend stream as cash can be helpful in the later years when the dividend stream is not sufficient to cover the RMD. A few scenarios, we were able to build up cash reserves of close to $100,000 (from the age of 70.5 to mid-90s). The excess dividend that is kept as cash could be accessed at any time and would serve as an excellent emergency savings account for a retiree.

Once an adequate amount of principal has been accumulated it becomes unnecessary to continue investing in growth stocks that pay no dividend. This isn’t to say you shouldn’t have some money invested in these types of companies but that the bulk of holdings should be paying you for holding their stock.

Disclaimer: This article is for informational purposes only and is not to be taken as investment advice. I always recommend that readers take the time to perform their own due diligence so that they can create a portfolio that makes sense for their risk tolerance and lifestyle. This article was written on my own and does not reflect the views or opinions of my employer.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: My clients are long the following stocks mentioned in this article: Apple (AAPL), Boeing (BA), 3M (MMM), Hormel (HRL), PepsiCo (PEP).

Be the first to comment