As my loyal readers know, I try to avoid writing on political matters, recognizing that Seeking Alpha is a financial site. However, from time to time, I must weigh in on certain political topics because that’s just part of my job.

We’re now in the midst of a partial federal government shutdown that began after House and Senate lawmakers failed to end the budget standoff, and adjourned when last-minute negotiations fizzled.

The House went home and the Senate adjourned, assuring that a quarter of the government would run out of money and be forced to shut down at midnight. Once it became a foregone conclusion that the government would be partially closed, President Trump took to Twitter, where he acknowledged the inevitability of a shutdown in a video.

In the video, President Trump called for bipartisanship support while he continued to insist that it is a “Democratic shutdown.” In a departure from his remarks at the White House earlier, President Trump said that he was prepared for a long shutdown,

We’re going to have a shutdown. There’s nothing we can do about that, because we need the Democrats to give us their votes.”

The standoff between President Trump and Democrats is in its second week and according to CBS News, “this is the 21st government shutdown since Congress adopted new budgeting procedures in 1976… and it’s also the third this year alone.”

One of the biggest misconceptions, as it relates to a temporary shutdown, is the impact to DoD spending. While some important agencies are impacted, such as Homeland Security, Transportation, Interior, Agriculture, State and Justice, as well as national parks and forests; Social security, military, Medicare and Medicaid will remain in operation.

The shutdown will impact 800,000 federal workers who will face furloughs or be forced to work without pay. Nine of 15 Cabinet-level departments and dozens of agencies are also affected.

But, to put it bluntly, a government shutdown will have zero impact on national security, the government will continue to pay all obligations (including rent).

As I said, I am purposely avoiding political commentary related to the highly debatable political issues, surrounding the Trump administration’s firm stance on border control, yet I am standing firm as it relates to Corporate Office Properties (OFC), the “black knight” of this on-going checkmate.

{kind=link}

Pullback Creates ‘Rare’ Investment Opportunity

According to the Congressional Budget Office (or CBO) “spending for the Department of Defense (or DoD) accounts for nearly all of the nation’s defense budget. The funding provided to DoD covers its base budget – which pays for the department’s normal activities – and its contingency operations.

CBO analyzes the possible consequences of planned reductions in funding for the military’s force structure and acquisitions. The agency also studies the budgetary implications of DoD’s plans, including those for military personnel, weapon systems, and operations.”

Funding for support functions consumes more of the defense budget today than it did in the 1980s, CBO finds. The largest increases were in healthcare, DoD management, communications infrastructure, and the science and technology program.

Source: COPT Investor Presentation

The U.S. military’s readiness to respond to current and future threats depends on the quality and availability of military forces – personnel, weapon systems such as ships and aircraft, and other material resources such as ammunition and fuel.

In turn, the quality and availability of military forces depend on the support infrastructure. The military uses that support infrastructure – such as bases, depots, and schools – to recruit personnel, train units for deployment, acquire and maintain equipment, construct facilities, provide healthcare, facilitate communications, and more.

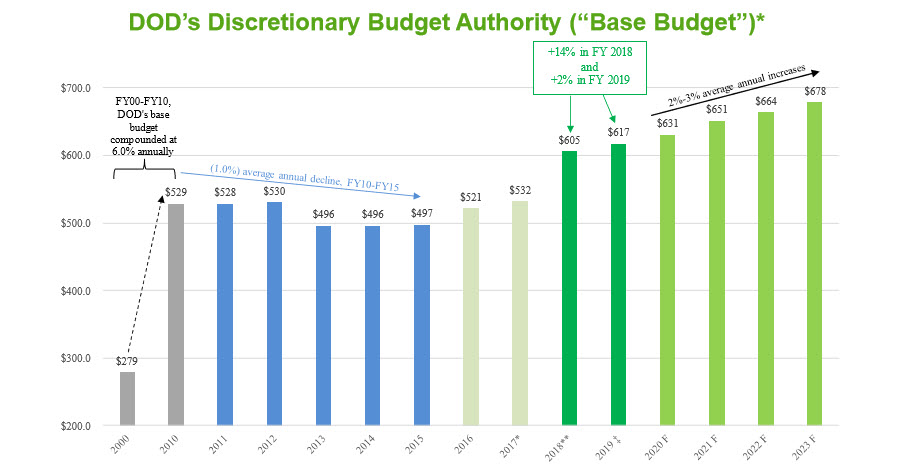

From the 1980s to the 2010s, the funding for support activities in DoD’s base budget rose in relation to funding for forces. Between 1980 and 1989, a period marked by the rapid defense buildup against the threat of the Soviet Union, support costs accounted for 43% of DoD’s nearly $500 billion base budget, on average.

Between 1990 and 2000, during the defense drawdown after the Soviet Union’s collapse, the average share of DoD’s base budget devoted to support costs grew to 49%. In the post–9/11 period, from 2001 to 2016, it rose further – to 50% (see below).

The Full Year 2018 budget provided the DOD with a $605 billion base budget – a 14% increase over Full Year 2017. The Full Year 2019 NDAA currently would increase DOD budget by another 2% (FY 2019 reflects amounts authorized in the FY 2019 NDAA (H.R. 5515), which was appropriated and signed into law on September 28, 2018).

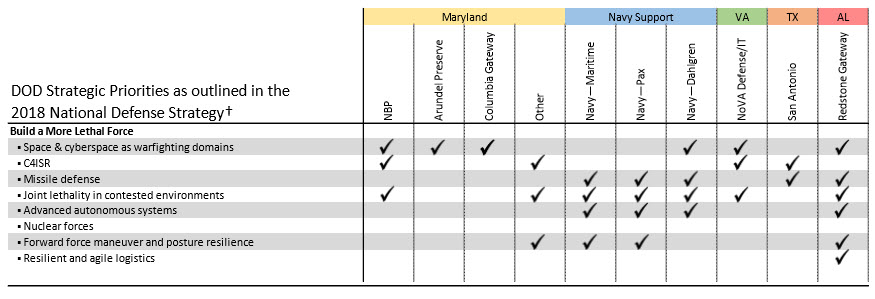

In 2018, the National Defense Strategy highlighted three DOD Strategic Priorities: (1) Build a More Lethal Force, (2) Reform the DOD for Greater Performance and Affordability, and (3) Strengthen Alliances and Attract New Partners. As viewed below, COPT’s (abbreviated throughout the rest of the article) Defense/IT locations are well-aligned with the nation’s defense spending priorities:

Source: COPT Investor Presentation

While DOD spending remains a top priority for Congress, Mr. Market seems to be less enthusiastic for shares in COPT, amid the prolonged stages of the current partial government shutdown.

Source: Yahoo Finance

A Mission-Critical REIT On Sale

COPT is the only REIT that is specifically focused on serving U.S. government agencies and defense contractors engaged in defense information technology and national security-related activities. This is a very strategic niche, and one in which COPT’s tenants are generally focused on knowledge-based activities such as cybersecurity, R&D, and other highly technical defense and security areas.

COPT has a strategic tenant niche that provides real estate solutions serving a specialized cyber-based platform. The defense installations (or government demand drivers) where COPT’s tenants operate are R&D, high-tech knowledge-based centers, NOT weapons or troops-related.

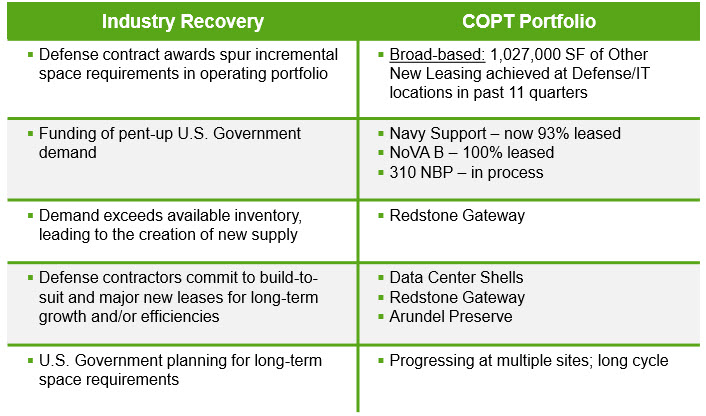

Accordingly, the REIT has a regional focus on owning properties in targeted markets or submarkets in the Greater Washington, DC/Baltimore region with strong growth attributes. COPT is a market leader in these markets, and the company has identified five impacts of industry recovery that are or will be driving demand at these mission-critical, Defense/IT locations.

Source: COPT Investor Presentation

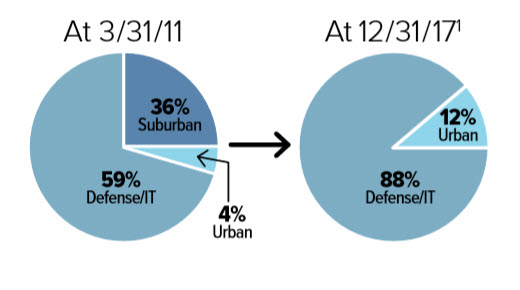

As of Q3-18, COPT owned 159 office and data center shell properties, encompassing 17.7 million square feet and was 94% leased. Of these, COPT owns 152 buildings in Defense/IT (15.7 million sf) and 7 regional office buildings (2.0 million sf). As of September 30, 2018, COPT derived 88% of its core portfolio annualized revenue from Defense/IT Locations and 12% from Regional Office Properties.

Source: COPT Investor Presentation

From 2011–2017, COPT has transformed its portfolio to focus on its unique Defense/IT franchise by selling $1.6 billion of commodity suburban office assets (10.9 mm SF), developing $1.2 billion (6.0 mm SF) and acquiring $345 million (1.5 mm SF) of strategic properties. The company has a significant concentration of assets in or around the Greater DC area, where there are a number of Federal Agencies and cybersecurity-focused operations.

COPT’s niche-based model provides competitive advantages that include:

Unique Land Positions – COPT has properties and entitled land adjacent to key knowledge-based defense installations. The company earns 59% of its core portfolio’s annualized rental revenue from 82 properties that are adjacent to Strategic Demand Drivers.

Development Expertise – COPT is a preferred and trusted developer with considerable experience in providing space for secured government operations.

Operating Platform – The company has unparalleled teams of managers with the specialized skills required to handle complex security-oriented needs. COPT’s credentialed personnel collaborate with the US government and defense customers on a frequent basis.

Customer Relationships – Its highly specialized business model provides a distinct competitive advantage, and one in which COPT’s customers reward the company with repeat business and sustainable growth opportunities.

Track Record – COPT was founded in 1988 as Royale Investments, and traded on the Nasdaq. The company changed its name to Corporate Office Properties Trust, and went on the NYSE in 1998. COPT has over two decades of operating experience, with growth in assets from $300 million (in 1998) to over $5 billion today.

Source: COPT Investor Presentation

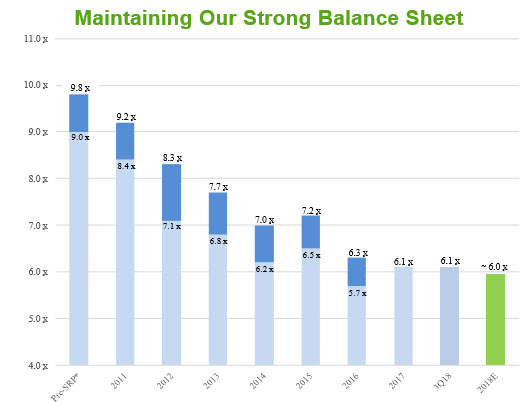

The Balance Sheet

During Q3-18, COPT executed several capital market transactions:

In late July the company closed on a $116 million construction loan for 2100 L. Street in Washington, D.C. The proceeds from this loan will completely fund the project’s remaining development cost and COPT continues to match fund development investments with equity.

The company drew down $80 million of its forward equity agreement and issued $30 million at $30.46 a share under the ATM program. The company said it was using the proceeds from the ATM to fund project capex which is incremental to the 2018 development plan.

Shortly after Q3-18, COPT entered into a new $800 million credit facility to replace its existing line. The new credit facility has improved pricing and covenants, matures in March 2023 and has two six-month extension options. Also, Fitch ratings upwardly revised its outlook on COPT’s credit rating from stable to positive.

Source: COPT Investor Presentation

The balance sheet metrics remain strong, and the company expects year-end debt plus preferred to EBITDA ratio to be consistent at ~6.0x and Debt/Adjusted Book ≤40%.

Source: COPT Investor Presentation

A Very Clear Path To Development Profits

One key differentiator for COPT is its focus on development. Demand for new construction in the company’s core markets remains strong, even during multiple consecutive years during which the DoD had no budget. As COPT’s CEO Steve Budorick, explains on the Q3-18 earnings call,

An elevated and predictable defense spending environment and consistent bipartisan support in Congress to fund defense are driving demand for expansion space throughout our operating portfolio and for new developments.”

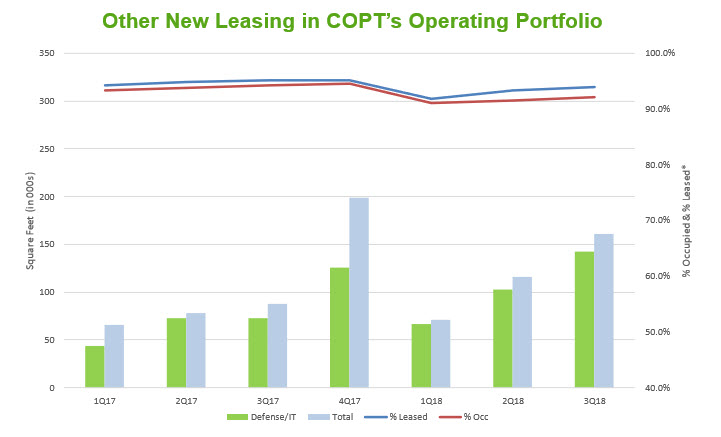

Highlights from Q3-18 include 161,000 square feet of vacancy leasing in the company’s operating portfolio that along with developments placed in service drove core portfolio back up to 94% leased. Notable large leasing gains during the quarter included the Fort Meade BW corridor sub-segment, which is up 50 bps to 92.4% leased. The NoVA defense/IT sub-segment is up 80 bps to 92.1% leased, and the Navy Support Group which gained 160 bps is now 93.2% leased.

Source: COPT Investor Presentation

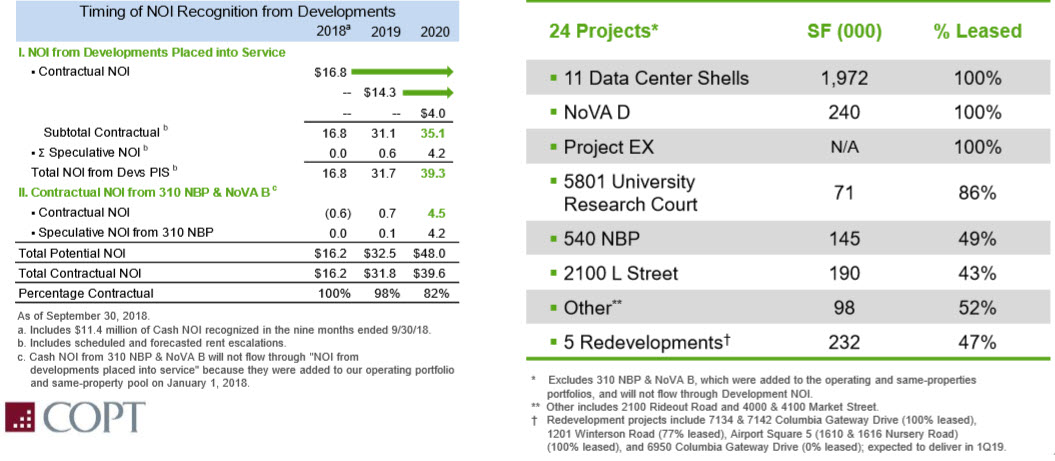

COPT announced (post Q3-18) two full building pre-leases for data center shells, representing the sixth and seventh leases of the 11 building pipeline. These leases bring COPT’s annual development leasing above 1 million square feet, and the company expects to meet our upwardly revise its development leasing goal for the year. COPT’s concentration of expirations at mission critical Defense/IT Locations mitigates rollover risk, as illustrated below:

Source: COPT Investor Presentation

On the Q3-18 earnings call, the company said that “the sheer volume of data center development activities has stressed the capacity of accounting zoning and power distribution resources extending the completion times for land development”. This means that the delayed commencements will defer some of the anticipated 2019 revenue into 2020, but “the magnitude of the revenue and the value creation of this program has not changed.”

Each quarter of delay in leasing the remaining 120,000 square feet equates to $0.01 of FFO opportunity cost to next year’s results, and the company said that “although the timing associated with leasing has been frustrating”, it “continues to have confidence the property will fully lease.”

COPT’s CEO added,

The DoD’s fiscal 2017 budget is driving the year-over-year increases we have achieved in vacancy leasing this year. Throughout 2019, incremental demand from the DoD’s substantial 2018 budget, which passed in law only seven months ago should amplify existing demand as defense outlays filter down to the real estate level. We will likely see incremental demand from the 2019 defense budget emerge toward the end of next year, further expanding leasing opportunities.”

Through 2020, 24 recently completed and under construction projects that are not in same-property represent up to $39.3 million of future annual Cash NOI, $35.1 million of which is contractual. Additionally, the two U.S. Government buildings represent potential Cash NOI of $8.5−9 million in 2020, $4.5 million of which is contractual.

Source: COPT Investor Presentation

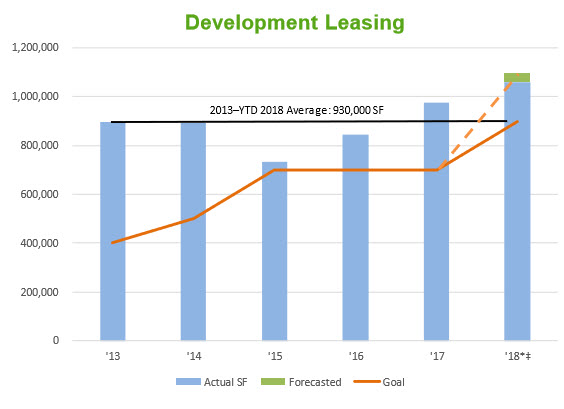

As viewed below, COPT’s robust shadow development pipeline bodes well for future development leasing & NOI growth. The 2–2.5 million SF shadow development pipeline supports the company’s upwardly revised 2018 goal of leasing 1.1 million SF in development projects. To date, 1.06 million SF have been completed:

Source: COPT Investor Presentation

The ‘Black Knight’ Wins

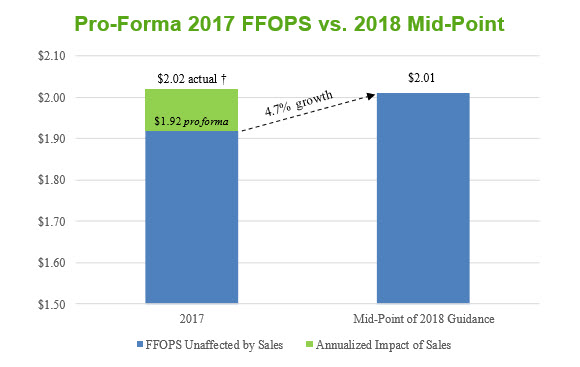

On the Q3-18 earnings call, management said it was maintaining the $2.01 mid-point of its annual guidance and tightening its range, from $1.98−2.04 to a new range of $2.00−2.02:

Source: COPT Investor Presentation

The company said it was also tightening Q4-18 FFO per share guidance from the prior range of $0.48 to $0.52 to a new range of $0.49 to $0.51. The $0.50 cent midpoint of the Q4 range is flat with Q3 results because the company is completing several weather-related R&M projects that were budgeted for earlier in the year. As illustrated below, the $2.01 mid-point of 2018 guidance represents 4.7% growth over pro forma 2017 results.

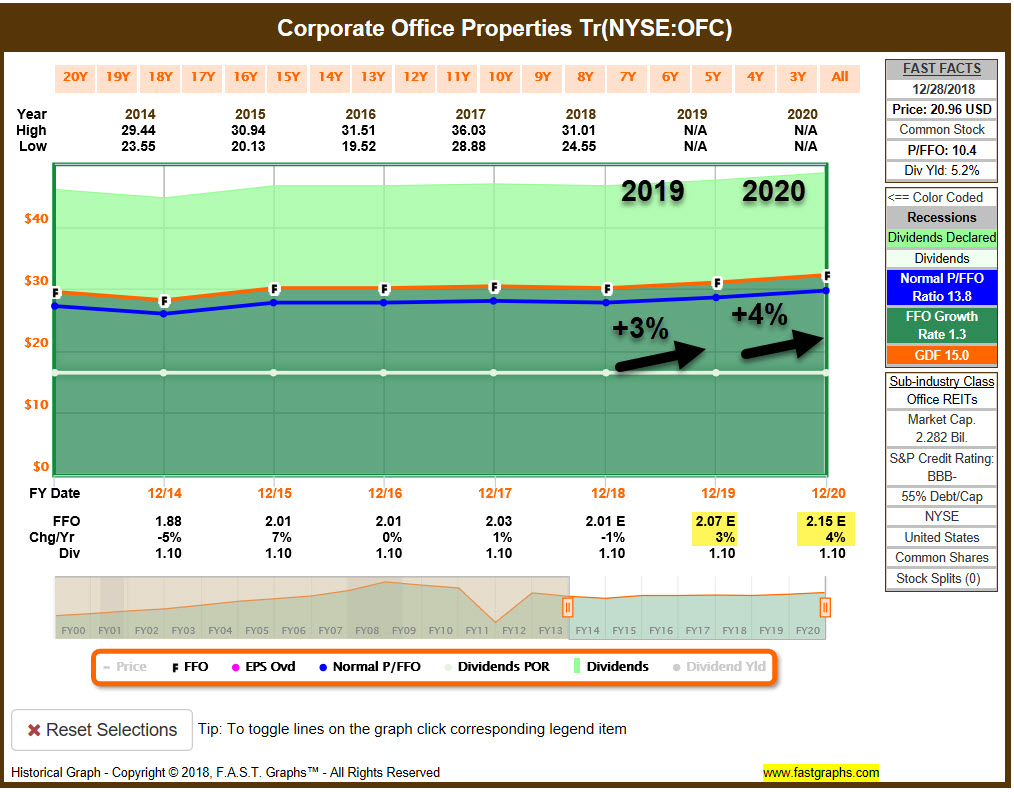

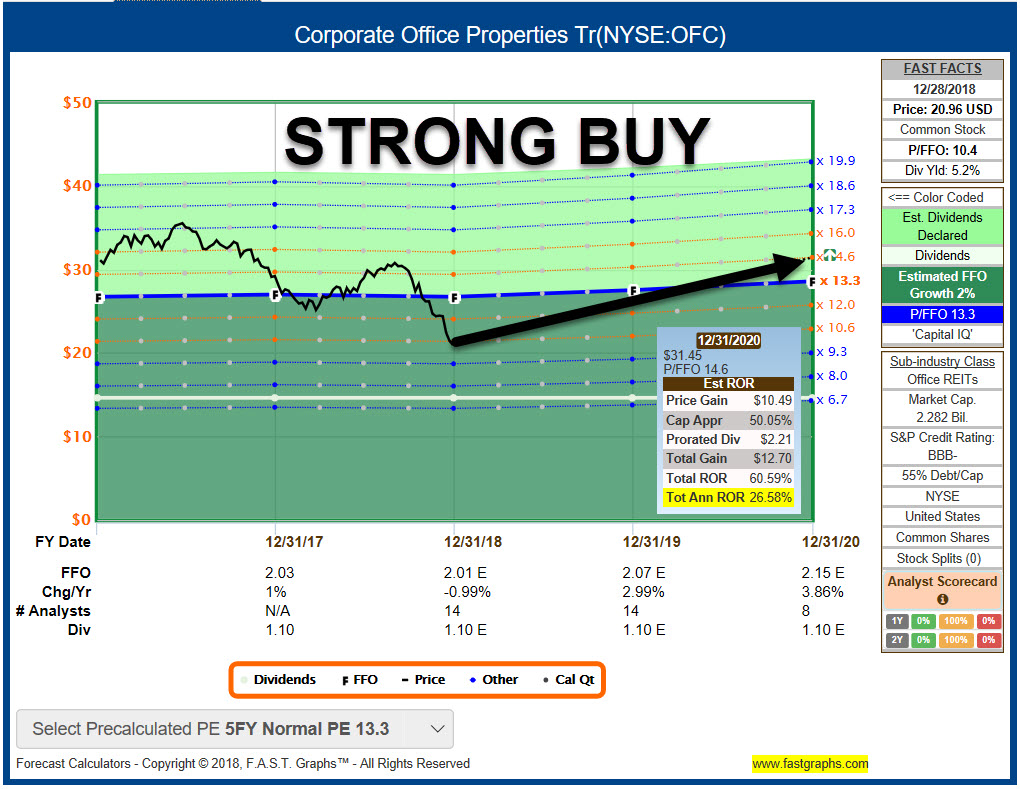

Although the above-referenced delays in completing the data centers and leasing will reduce COPT’s 2019 results, the strength and volume of leasing in the operating portfolio, and the benefit of executing additional development projects will partially offset the impact of these delays. Here’s how analysts forecast COPT’s FFO/share growth in 2019 and 2020:

Source: F.A.S.T. Graphs

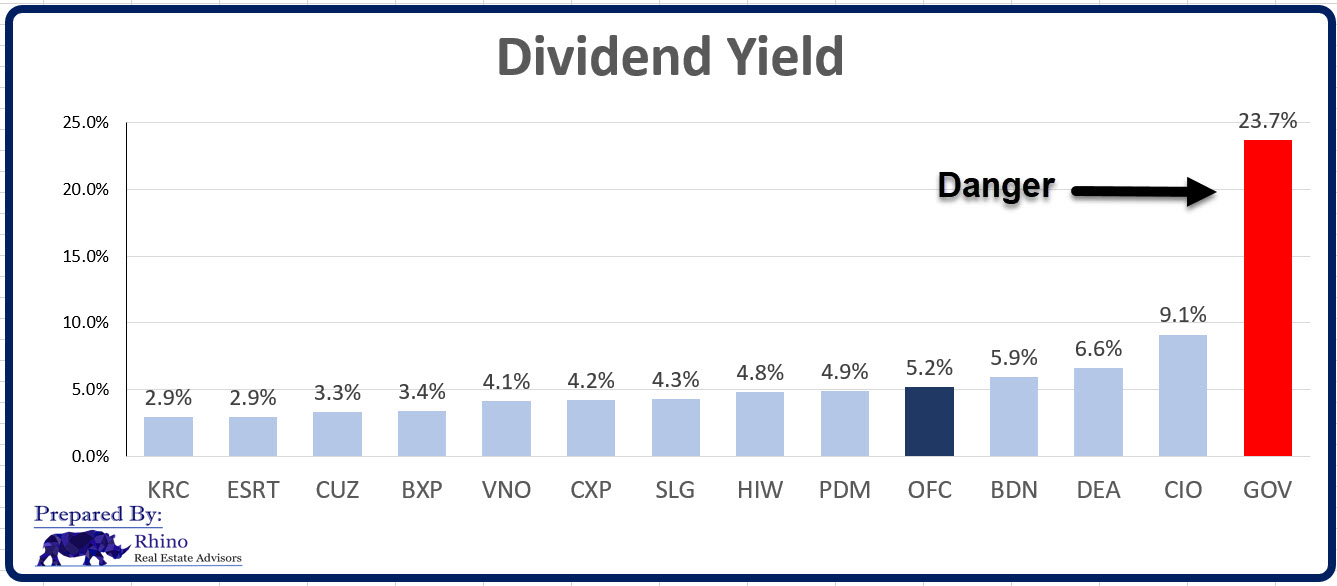

Now, as I said, COPT has no direct peer, so we will compare to the broader peer group, starting with the dividend yield:

Source: Rhino Real Estate Advisors

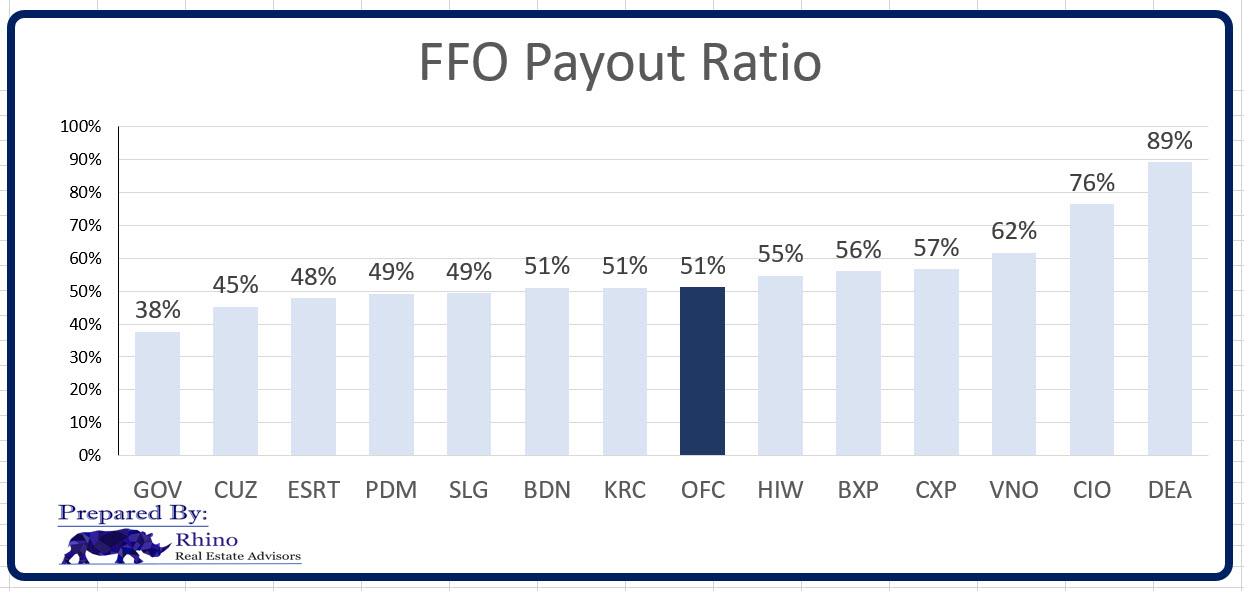

As you can see, COPT is yielding 5.2%, and the although the company has not raised its dividend (it cut in 2011 and has not increased since 2012), the payout ratio appears relatively safe, as illustrated below:

Source: Rhino Real Estate Advisors

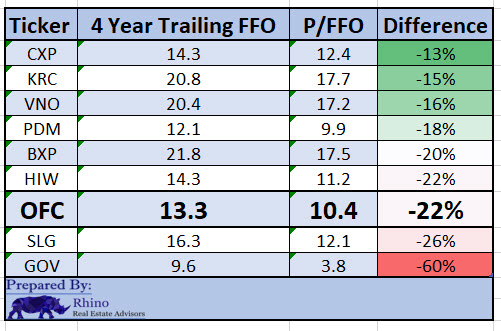

Now as viewed below, OFC trades at a sizable discount, based on P/FFO metrics:

Source: Rhino Real Estate Advisors

Keep in mind that 88% of COPT’s core portfolio annualized rental revenue comes from growing Defense/IT locations (core portfolio 94% leased). Also, the pipeline of future build-to-suit transactions and expansion activity among existing operating properties remain robust.

The company has multiple avenues of growth in Defense/IT generate durable, less correlated demand for new facilities: (1) U.S. Government, (2) Contractors serving at the mission, and (3) Contractors providing cloud computing.

And remember, the temporary government shutdown has ZERO impact to COPT’s rent checks and, as a result, we are upgrading the company from a Buy to a Strong Buy. While the checkmate over the budget continues, we are confident that the “black knight” will prevail, and we will have no problem “sleeping well at night” owning shares in Corporate Office Properties Trust.

Disclosure: Stephanie Krewson-Kelly, my co-author of The Intelligent REIT Investor (available on Amazon (AMZN)), is also director of Investor Relations at COPT.

Author’s note: Brad Thomas is a Wall Street writer and that means he is not always right with his predictions or recommendations. That also applies to his grammar. Please excuse any typos and be assured that he will do his best to correct any errors if they are overlooked.

Finally, this article is free, and the sole purpose for writing it is to assist with research, while also providing a forum for second-level thinking.

Disclosure: I am/we are long OFC. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment