I originally wrote about OneSpan (OSPN) a few months ago and explained why I believe investors who were holding shares in the e-signature company should eliminate their position due to anemic revenue growth. I attributed the weak revenue growth to OneSpan’s slow transition to a SaaS business model since it seemed that licensing had the effect of repelling prospective customers who were not keen on spending a lot upfront and leaving existing customers content with older versions of OSPN’s software and thus foregoing upgrades for years at a time.

Three months later, I am here to update investors on whether OneSpan has made noticeable progress in bolstering revenues and delivering tangible growth for shareholders.

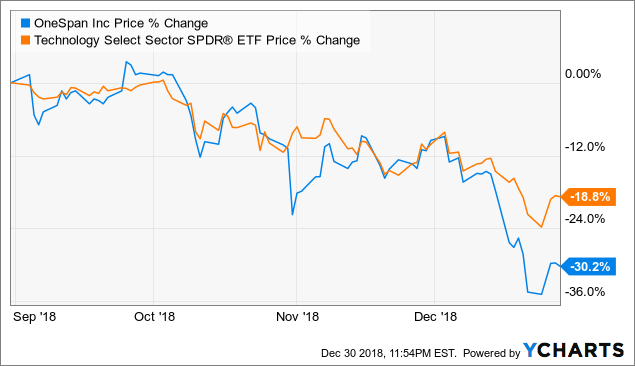

OSPN data by YCharts

Before getting into the analysis, I just wanted to show you how OneSpan has performed since I last wrote my critical piece on it; the e-signature company has fallen 30%, while the ETF that I use as a technology sector benchmark fell 18% in the same period.

Balance Sheet

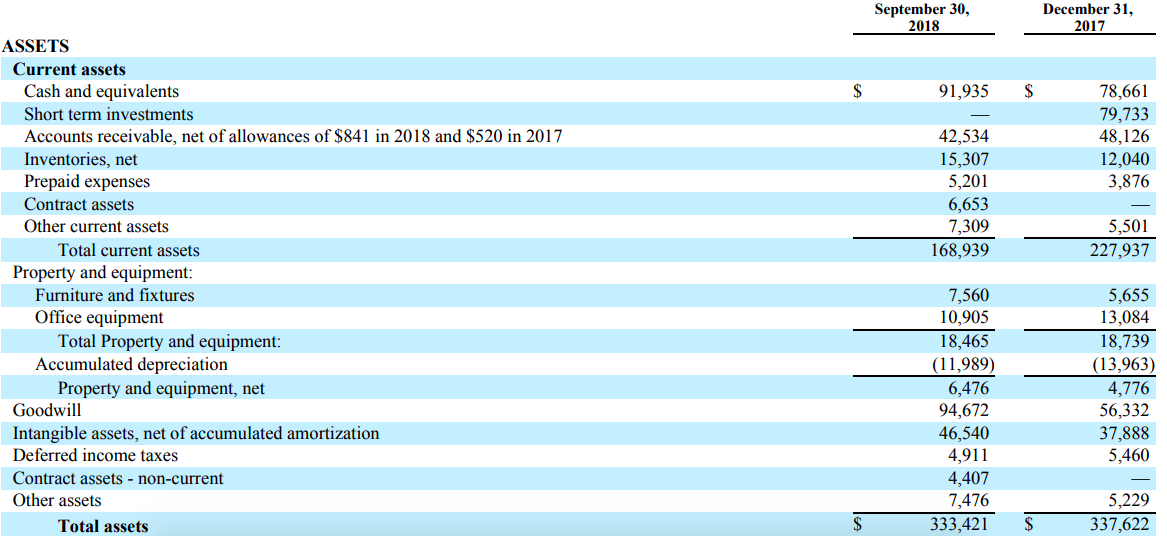

Let’s start the analysis with a look at how OSPN is doing in terms of assets.

(Source: Q3 2018 10-Q)

Cash & equivalents rose $13 million from the beginning of the year to the end of the third quarter. However, you probably also noticed that short-term investments were completely depleted. Earlier this year, OneSpan acquired Dealflo for $53 million. The decrease in current assets amounted to $59 million for the nine-month period. A net decrease of $6 million in current assets is not a red flag. If you look at goodwill, you will notice that it rose by $38 million following the Deaflo acquisition. This means Dealflo only increased OSPN’s assets by $15 million. This also means that OneSpan paid a 153% premium to acquire the company. For that much, investors should be hungry to see Dealflo generate serious growth.

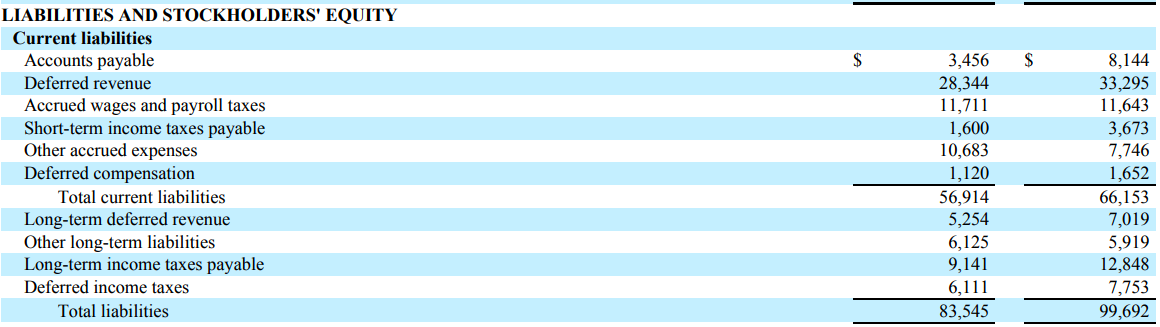

(Source: Q3 2018 10-Q)

There is not much to glean from liabilities; the only figure worth noting is the $5 million decrease in deferred revenue. It is not uncommon for SaaS businesses to collect payment for subscriptions ahead of time and for varying periods (such as three months in advance or one year in advance). Accordingly, when I notice a fledgling SaaS company like OneSpan experience a decline in deferred revenue that tells me it is struggling with its transition to a SaaS model. If the deferred revenue decrease occurred between adjacent quarters, I might give OSPN the benefit of the doubt and shrug it off as a seasonal issue or isolated event, but over a nine-month period, management has no excuse.

Revenues

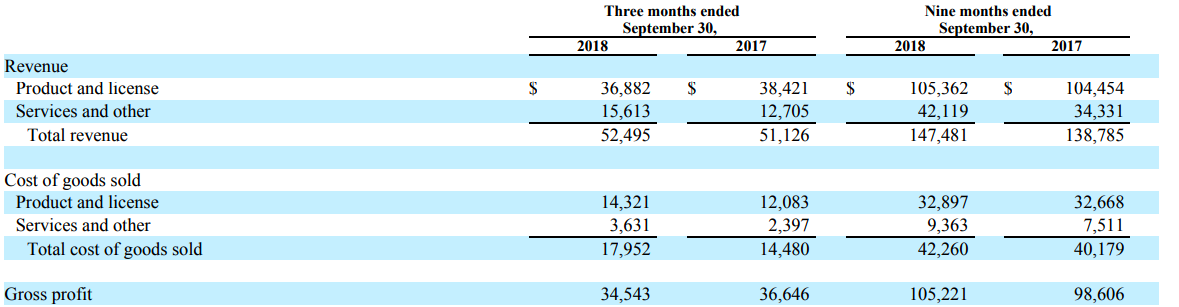

(Source: Q3 2018 10-Q)

Now, for a look at revenues. For the quarter-over-quarter results, there is a continued shift to recurring revenue as services and other increased 25% to $15 million. Meanwhile, licensing revenue fell approximately $1.5 million. Overall, total revenue increased a measly 2.7% in the period. When you factor in costs of revenue, the story looks bleaker: licensing costs rose 19% and services and other costs rose 52%. Paying higher licensing revenue costs on declining licensing revenue is a pressing problem and shows that management’s inability to quickly transition to a recurring revenue model is hurting shareholders. On the other hand, I would like to know why services and other costs increased 52% because the whole point of recurring revenue is to increase operating leverage – not erode it. Even over the nine-month period, you see the increase in recurring revenue costs outpace the increase in recurring revenue. I could not find any insight from management that would suggest that those cost increases are mostly fixed and not variable, which leaves me uneasy about OneSpan’s e-signature market position.

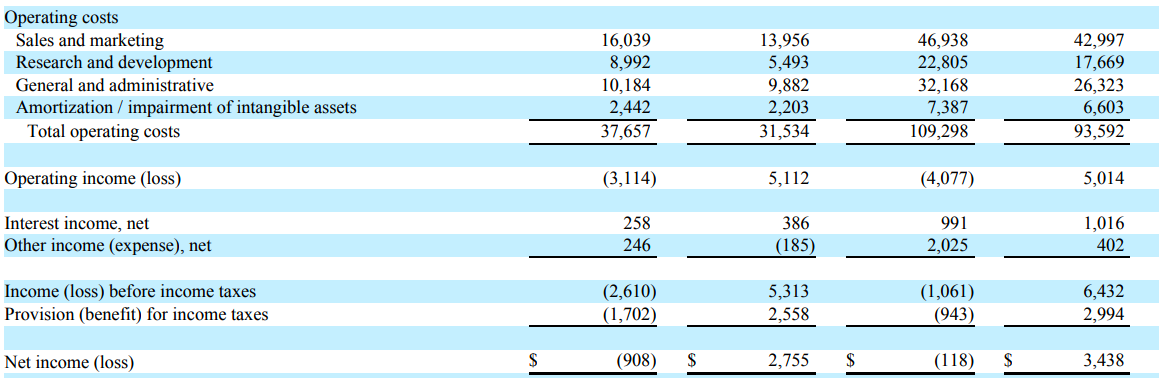

Here are the operating costs and net income figures as well:

(Source: Q3 2018 10-Q)

I want to point out OneSpan’s inefficiency in sales/marketing. Management increased sales/marketing expenditure by $2 million this time, but gross profit fell by roughly $2 million. I am seeing two reasons for why this is happening: either the increase in sales/marketing was focused on attracting more subscription customers or this is symptomatic of the licensing model, in which sales just had a bad quarter. That would be something else that management should clarify for investors. For the reasons above, OneSpan’s net income turned into a net loss in the last quarter, which is not a good sign for investors. What makes this especially concerning is that the net loss does not stem from growth initiatives that require heavy capital expenditure upfront, but rather, stems from anemic revenue growth and larger increases in costs.

Cash Flows

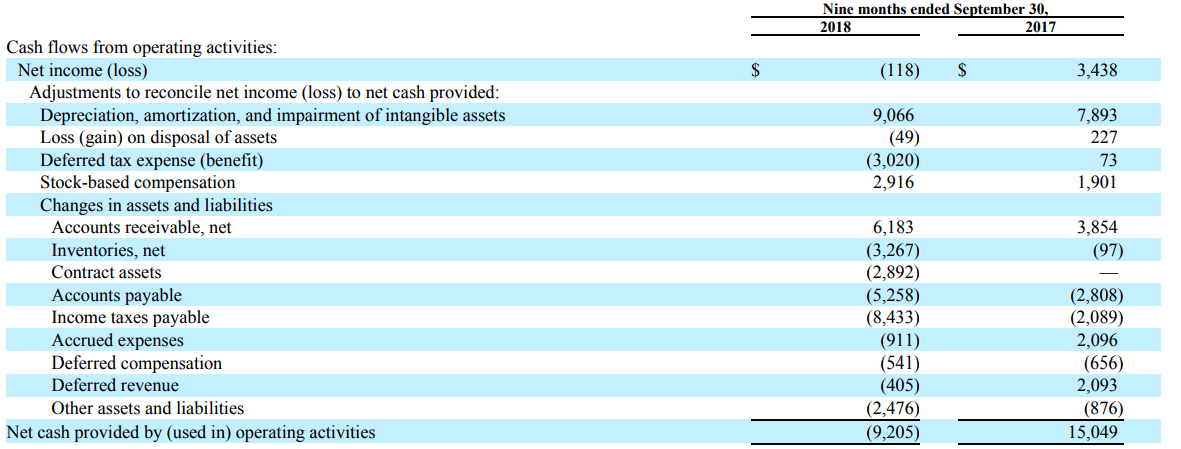

The income statement did not look too good, but the operating cash flows will give us a better look at the financial health of OneSpan.

(Source: Q3 2018 10-Q)

At the bottom, OSPN was over $9 million in negative operating cash flows. In 2018, however, the company had a deferred tax benefit of $3 million. So the real loss is down to $6 million. Another factor was an inventory increase that also decreased operating cash flows by $3 million. The increase in inventory seems to contradict management’s intentions to transfer licensing revenue into subscription revenue. It seems as though OSPN has difficulty forecasting demand because licensing revenue fell relative to last period, and now the company is sitting on inventory that could be outdated by next year if it is not sold. Contract assets also lowered operating cash flows by nearly $3 million, but OSPN will collect on this eventually, so operating cash flows for the latest period are nearer to zero rather than negative $9 million.

Moving on, here are the cash flows from investing:

(Source: Q3 2018 10-Q)

In this table, you can see that OneSpan freed up cash by letting $80 million of short-term investments mature so they could pay for the Dealflo acquisition, which cost them $53 million. It seems that management freed up more cash than required to finance the Dealflo purchase since operating cash flows were negative. With about $92 million left in cash and equivalents, OSPN has a decent liquidity buffer, so the negative operating cash flows are not yet a huge concern. But, if the company continues to see negative operating cash flows, then investors may have to worry about management seeking out debt to keep the company afloat. It is too early to speculate about insolvency, so I will save that for a future article.

Exchange Rate Woes

Lastly, I want to discuss the effect of exchange rates on OSPN’s cash flows.

(Source: Q3 2018 10-Q)

From the latest quarterly filing, 48% of OneSpan’s revenue is derived from EMEA (Europe, Middle East, and Africa). I believe that a substantial majority of EMEA revenue comes from Europe alone, so I pulled up a two-year chart of the euro versus the dollar.

(Source: XE)

The graph shows the value of the euro in terms of dollars from the beginning of 2017 to now. As the chart increases in the beginning, the dollar weakened. Thus, OneSpan’s cash flows were buoyed $640,000. Fast forward, and as the dollar strengthened, OneSpan lost $647,000 in the first nine months of fiscal year 2018. Due to political/economic issues within Europe, such as “Brexit” and turmoil within France and Germany, the dollar looks poised to gain further ground against the euro as investors migrate to it for higher yielding US bonds (thanks to interest rate hikes) and for its greater safety compared to other currencies around the world. Thus, this could be another disadvantage that OneSpan faces, considering its rivals – DocuSign (NASDAQ:DOCU) and Adobe (NASDAQ:ADBE) – generate greater proportions of their revenue within the United States.

Conclusion

OneSpan was struggling when I originally wrote about it, and unfortunately, this e-signature company’s woes continue. Its liquidity has decreased as millions were spent on the acquisition of Dealflo. Despite the acquisition, revenue growth was marginal with costs of revenue growing at a faster rate than revenue itself. Operating cash flows turned negative, forcing the company to redeem short-term investments in order to cover expenses for the foreseeable future. Finally, a strengthening dollar has eroded OneSpan’s cash flows since nearly half of its revenue comes from EMEA.

For the reasons listed above, and the fact that management has been slow and ineffective with transitioning to a recurring revenue model, I recommend a short position on OSPN.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment