While I expect the company to beat on revenues, I will be more attentive to margin trends, and do not rule out an EPS miss this week.”

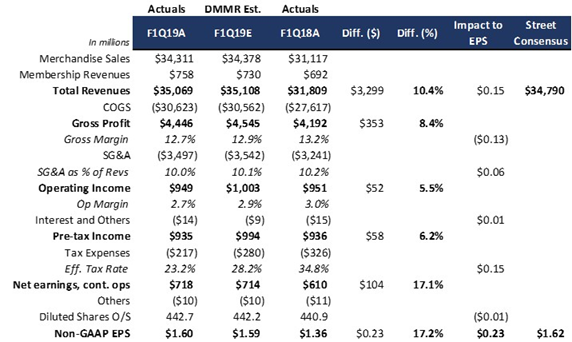

This was one of the key takeaways from my earnings preview published earlier in the week on consumer wholesale chain Costco (COST). The Irvine, California-based company did not disappoint me this Thursday evening, delivering $35.07 billion in revenues that beat consensus by a sizable $280 million, but landed short of my estimate by a much less meaningful $40 million. Meanwhile, $1.60 in EPS adjusted for an SBC-related tax benefit lagged expectations by two cents, although it topped my projections by a penny.

Credit: Food and Wine

When it comes to merchandise revenues, once again Costco had set the expectations ahead of time with its monthly sales reports. Adjusted comps of 7.5% had already been known and priced into the stock, but I was impressed to see membership revenues rise 9.5% YOY. This was highly unexpected, in my view, as Costco has already lapped the July 2017 fee increase of 9%. The results can probably be best explained by what I anticipated would be “a robust trend in new signups and a favorable mix towards the higher-end $120 tier” – although to a greater extent than I had originally projected.

Membership sales are too small, however, to make much of an impact on total company revenues, at roughly 2% only. I would have imagined the true P&L impact of better-than-expected fee revenues to be felt in the form of better profitability metrics since I estimate that memberships have a very high margin profile. Therefore, I was a bit disappointed to see op margin of 12.7% land 20 bps short of my estimate. With SG&A as a percentage of revenues having dropped YOY once again, as per my expectations, the culprit here seems to have been merchandise margins that did not quite impress.

At play here are likely the well-known factors that have been plaguing most in the retail industry: trade wars, higher fulfillment costs, and a revenue mix shift towards lower-margin e-commerce. Although I had anticipated some YOY deterioration, more specifically around 30 bps worth of margin contraction, I expect that the more pronounced pullback is likely to keep sentiment more on the bearish side during this Friday’s trading session.

Source: D.M. Martins Research, using data from company reports

On the stock

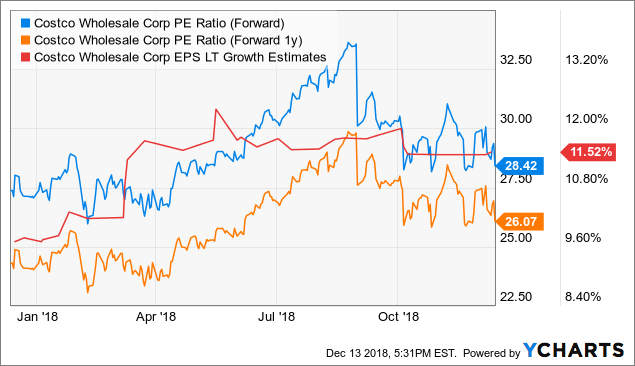

There isn’t much that I can say, following Costco’s earnings report, that I haven’t already made clear about this stock. The company continues to perform very well, and I am deeply appreciative of the recurring-like business model that should ensure stable earnings growth over time as a result of “sticky” and relatively stable membership revenues. For example, see the very steady trend in long-term EPS growth expectations represented by the red line in the graph below.

COST P/E Ratio (Forward) data by YCharts

COST P/E Ratio (Forward) data by YCharts

Having said that, COST could suffer some short-term pressure as a result of (1) less-than-impressive merchandise margins and (2) valuations that might still look rich to many, at a multiple of 28.4x current-year earnings. Should the stock suffer a more pronounced correction in the next few weeks, COST could become a “pound the table” buy, in my opinion. Still, even at current levels (the stock has been beating the broad market by nearly three percentage points over the past three months), I find COST a stock worthy of further due diligence by those that do not currently own shares.

Note from the author: COST is one of the names in what I call my “All-Equities SRG” portfolio. To learn about other names that I have invested in and find out how I have built a risk-diversified portfolio designed and back-tested to generate market-like returns with lower risk, join my Storm-Resistant Growth group. Take advantage of the 14-day free trial, read all the content written to date and get immediate access to the community.

Disclosure: I am/we are long COST. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment