I cannot quite recall but my first online purchase was probably on eBay (EBAY) and with my PayPal account. In today’s context, there are many more competitors through Alibaba (BABA), Amazon (AMZN), Shopee (SE) and a host of other traditional retailers now selling online like Walmart (WMT). Somehow, eBay still thrives in spite of the competition. It thrives even though it is not mentioned much in the investment world (I will get to the financials later), and it thrives because eBay offers value to consumers and thus remains relevant since September 1995 till today.

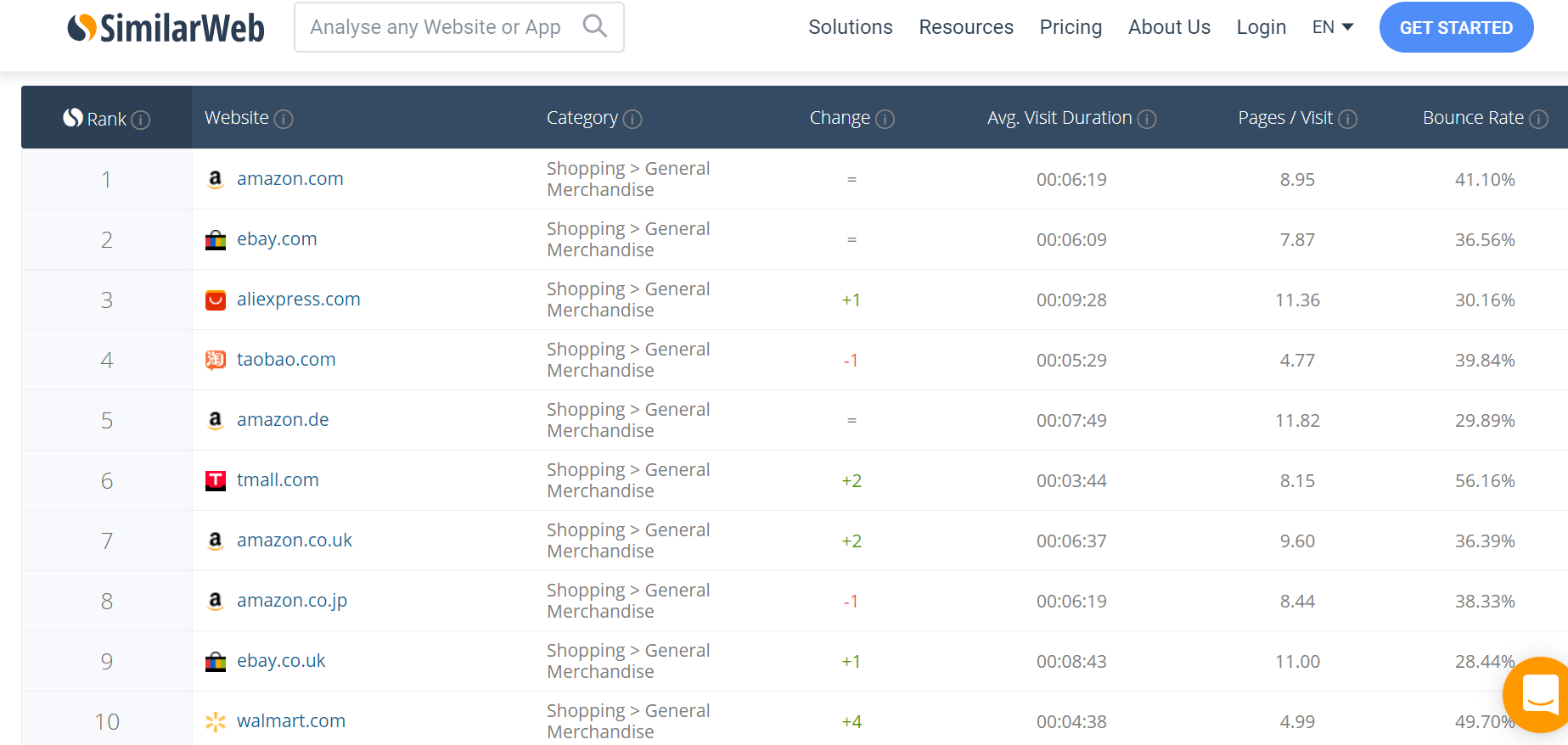

Here is a look at how eBay ranks in terms of traffic, which is a respectable #9 in the USA and #30 worldwide. In terms of e-commerce sites globally, eBay still ranks #2, behind Amazon.com (note that Amazon has other domains listed in the list below for other countries like the UK and Japan).

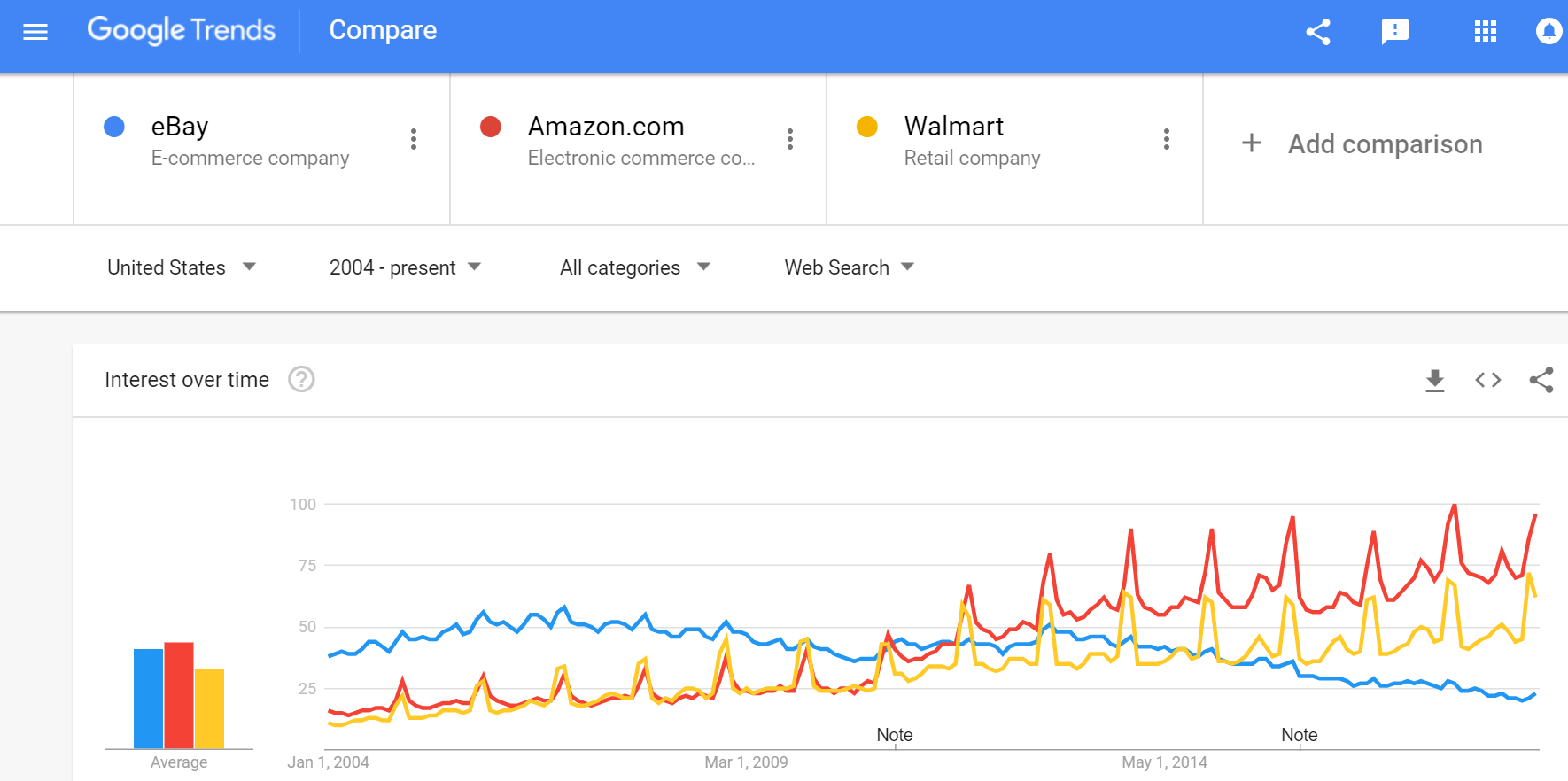

The concern which everyone has probably expected is illustrated below. Based on a long term trend from 2004 to today, interest in eBay has declined while Amazon and Walmart have both trended upwards in a consistent manner.

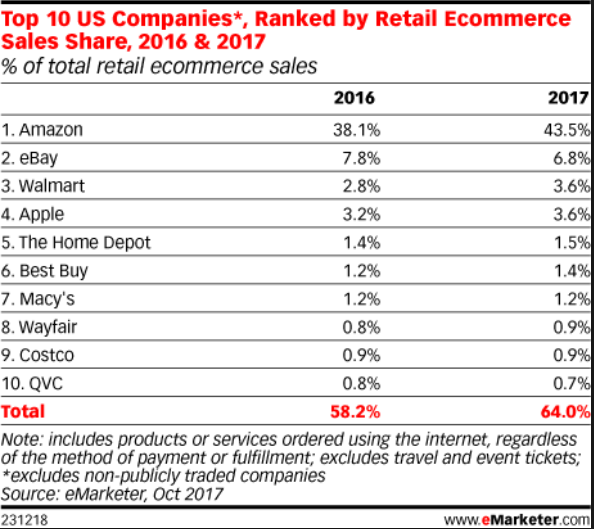

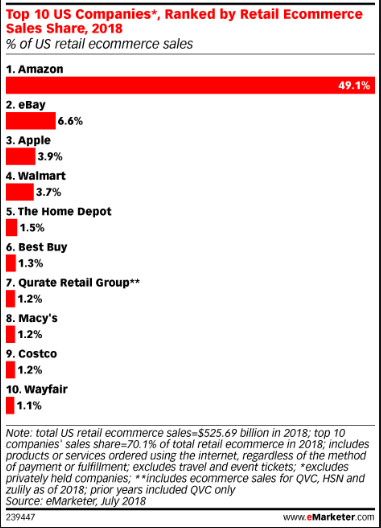

eBay’s share of Ecommerce in the US has also declined since 2016 based on eMarketer.com data from 7.8% share to 6.6% share in 2018.

A declining share of the market does make the investment outlook bleak. However, there has been transactions growth on eBay’s website despite the declining share, meaning that more consumers are purchasing online, growing the wider market, and bulk of that goes to Amazon and to a lesser degree, players like Walmart.

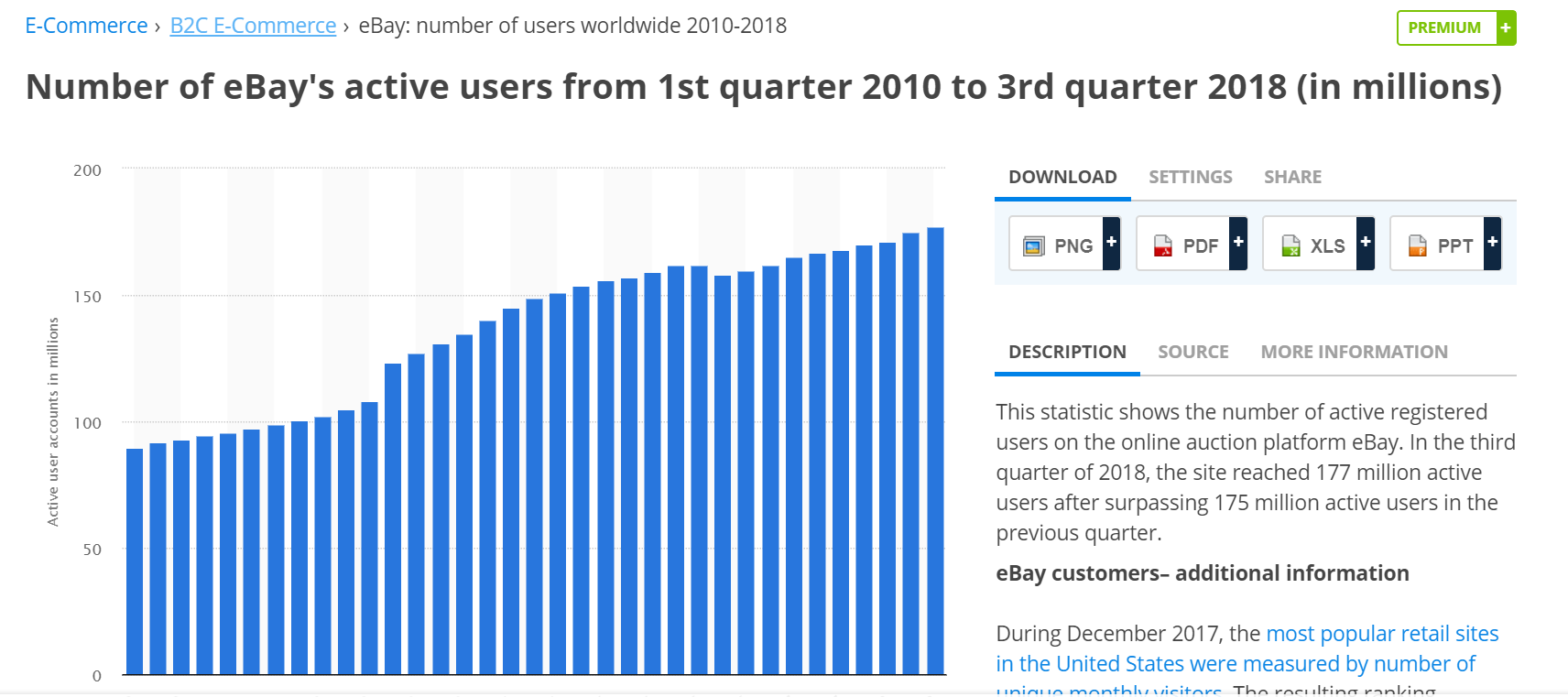

Based on statista data, eBay’s active users has been rising consistently between 2010 and 2018. In eBay’s Q3 2018 filings, management reported growth in “active buyers by 4% across its platforms, for a total of 177 million global active buyers” and “marketplace revenue growth was 6% on an as-reported basis and 5% on an FX-Neutral basis, and GMV was up 5% on both an as-reported and FX-Neutral basis.”

7% and 8% growth in revenue was reported in StubHub and Classifieds respectively. The data infers that each user on average is spending more money on eBay.

At the end of 2017, eBay reported 170 million active buyers, rising from 167 million in 2016 and 162 million in 2015. Growth in active buyers validate eBay’s continued relevance despite aggressive growth among competitors, especially Amazon.

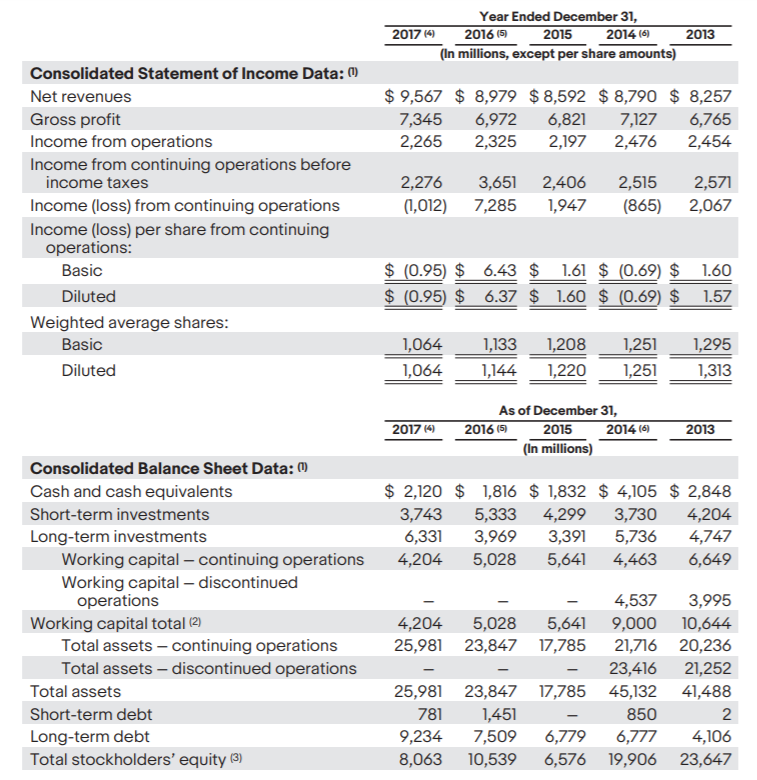

The ability to remain relevant and be competitive however has come with a price tag in the form of margin compression and a flat bottom line.

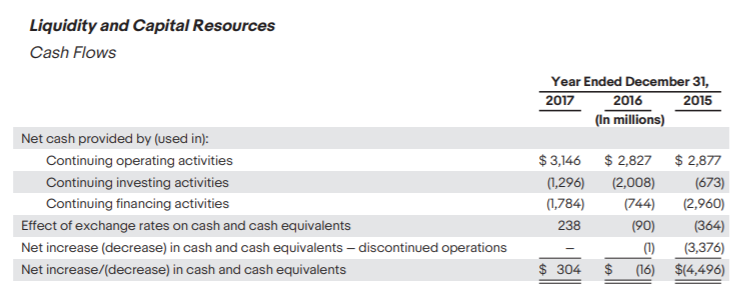

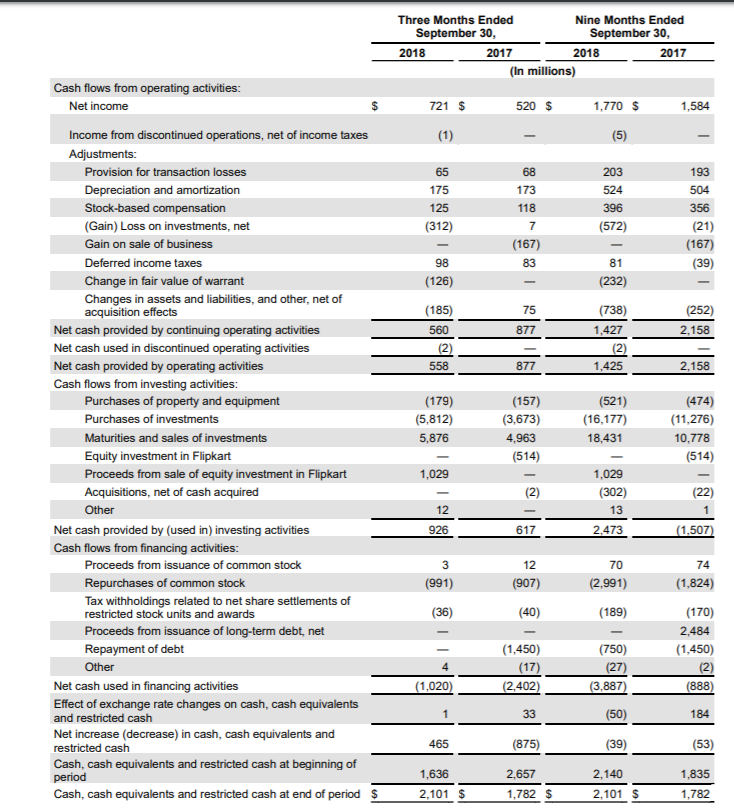

The business continues to generate cash from operations and bulk of the cash has been used for investments and share repurchase.

The main concern is the amount of debt that has risen since 2013. Net debt (debt excluding cash and short term investments) was $4.15 billion in 2017 compared to net cash of $2.94 billion. Q3 2018 Net debt was $4.37 billion.

Having increasing debt is not a concern if the debt is used appropriately and helps grow the business in a sustainable manner.

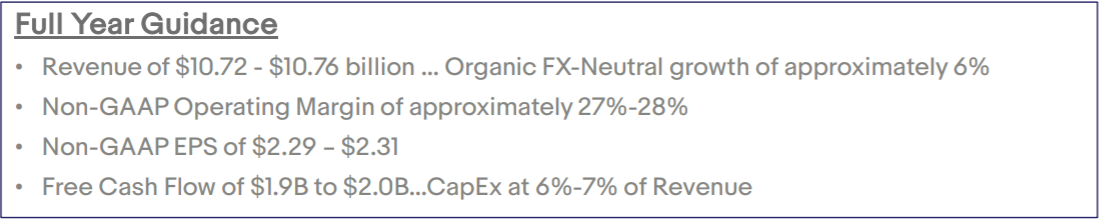

With free cash flow guiding at $1.9 billion and EPS of $2.29, eBay has operating leverage in managing its debt and share repurchases. Importantly the current price of $29 values eBay at a PE of 12.7x, which is inexpensive.

eBay now has to execute on growing its earnings and turning its ticketing business into a profit growth driver. Stubhub contributes over 10% to the total revenue of the business but the revenue growth demonstrated above has not cascaded down into net profits. Because eBay does not report operating profits by its marketplace, classifieds and ticketing platform segments, it is my guess that the results from acquisitions have not been successfully converted into profits.

From a merger and acquisitions perspective, management has made a couple of shrewd and strategic decisions around the StubHub acquisition and the sale of eBay’s India business to Flipkart. The StubHub purchase valued at $310 million back in 2007 which generated $100 million sales in 2008, about 3x price-to-sales. eBay further acquired Ticketbis for $165 million in 2016 to give StubHub a global reach. It was reported that Ticketbis sales was $45 million in 2016 having grown from $25 million in 2015.

The Flipkart deal has enabled eBay to profit from Walmart’s acquisition of Flipkart for $16 billion. In addition, now that a competitor has bought out Flipkart, Flipkart had to cease operating the eBay.in website with eBay stating its intention to enter India again.

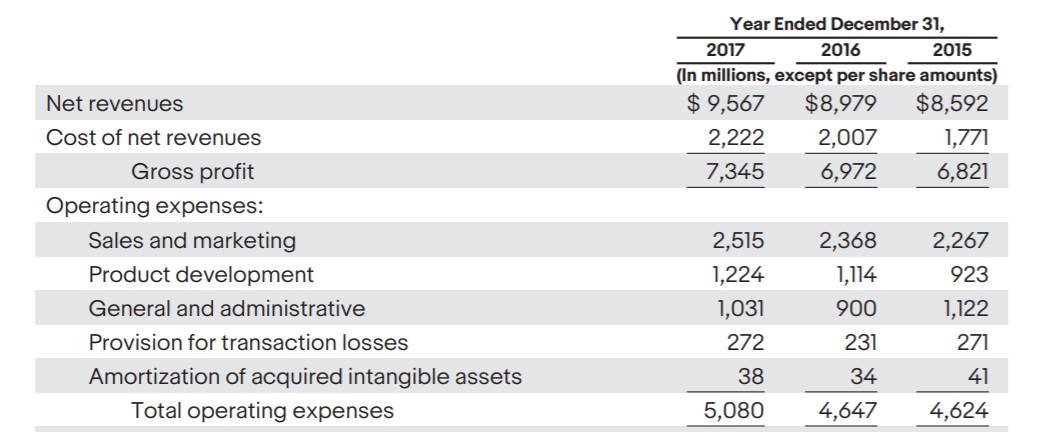

The issue in the growth equation lies in the operating expenses below gross margins. Gross margins has declined from 82% in 2013 to 77% in 2017. That 5% decline is understandable as the competition has intensified through this period. However, operating margins has also been squeezed with rising sales and marketing costs, product development and general and administrative costs.

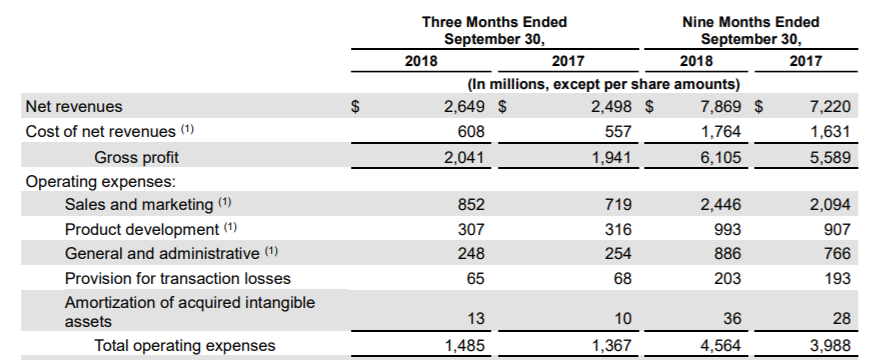

The same trend persists into the first 9 months ended September 30, 2018.

With these headwinds in place, the answer is in Adyen, the payments solution provider replacing PayPal. Management had reported a potential savings of $500 million when fully deployed in 2020. This deal allows eBay to potentially own 5% of Adyen’s shares as well, valuing this stake at about $750 million (Adyen’s market capitalization is about $15 billion). This additional savings translate to about 20% upside given the same 12.7x multiple.

eBay meanwhile continues to repurchase shares and its business is able to afford more leverage to do so. The authorized repurchase program has $4.7 billion remaining which I reckon can be made within 2 years, through the cash generated from operations. This represents another potential 15% value creation opportunity.

The total 35% in potential value being created makes this company an interesting pick for my retirement portfolio which is designed to accumulate in value before transitioning into a distribution yield focused retirement portfolio.

Note: fellow investors who are interested in screening stocks with a PE under 15x and has had either a growth story or a record of earnings growth can take a quick read of some of my articles and shortlisted picks.

Disclosure: I/we have no positions in any stocks mentioned, but may initiate a long position in EBAY over the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment