Manole Capital Management

November 2018

If you wish to view any of Manole Capital’s proprietary research, thematic notes, prior newsletters or individual stock calls, please search the Seeking Alpha site under Manole Capital. We always publish our research to SA. If you enjoy our FINTECH focus or process, strategy and/or investment philosophy, please become a SA “follower” of ours.

America First:

One may not like President Trump or his policies, but he clearly relishes his role as a non-Washington DC insider. He delights in his character as a political outsider and took office vowing to shake up the global free-trading system. He has imposed tariffs on allies and frenemies. He has trashed NATO, removed the US from the UN Human Rights Council and made numerous other decisions to bewilder political elite. He seems unafraid to “ruffle some feathers”, as he attempts to follow through on some of his campaign promises. His popularity with many is a result of his anti-establishment and ridicule of the media and elite. So many politicians have failed to deliver on campaign promises, that it is easy for him to state his demand for action and America First mantra. What seems to upset so many, is President Trump’s harsher delivery of the America First message.

For a very long time, America has been the world’s policeman. For decades, we ceded fair trade policies to better our less fortunate neighbors and allies. At a recent political rally of his supporters, President Trump said he was elected to be “the President of the United States and not the President of the World.” With such a global economy, this worries those that believe these policies are leading us towards protectionist and isolationist strategies. President Trump and his administration are steadfast in their defense of the American worker and continue to pronounce a strategy of acting in “the best interest of America first and foremost”. At a recent UN speech, initially set to discuss global relations, President Trump said “we will no longer tolerate such (labor) abuse. We will not allow our workers to be victimized, our companies to be cheated, and our wealth to be plundered and transferred”.

Farmers, businesses and even some Republicans are pushing back on this approach. Many worry that it will ultimately cost consumers and those dependent upon exports. Lawmakers facing tough congressional elections are also worried about the short-term ramifications. The administration counters with the same argument every time. It states that its goal is to “preserve and expand trade, not contract”.

For decades, the US allowed other countries to apply tariffs to our goods, to build out a healthy, global trading environment. The days where the US subsidizes other countries growth sound to be over. Even if a zero-tariff initiative could be negotiated, it will be nearly impossible to enact. No country will remove protections for industries it deems to be vital. This becomes even more prevalent, when a country’s leaders are up for re-election.

A Look Back on China:

Before we tackle the complicated US/China trade issue, we thought it would be helpful to look back on some Chinese economic history. To fully appreciate the current trading situation, we believe it is necessary to understand the last 50 to 100 years of Chinese economic growth.

A Century of Chinese History:

Starting in 1900, the Open Door policy advocated by the US spared China from European colonization. Prior to World War II, the US deployed military assets in the Pacific in defense of that policy. During World War II, the US mobilized to assist China’s defense against an aggressive Japan. At the end of the war, the US ensured that China was included as one of five permanent members of the United Nations Security Council.

Following World War II, China and the US begun to have some issues. The Chinese, while unified in fighting a Japanese occupation, were beginning to become a divided country. On one side, there were the Communists, led by Mao Zedong. On the other, were the Capitalists or Nationalists led by Chiang Kai-shek. The US provided military assistance to the Nationalists, but ultimately, the Communists controlled mainland China by 1949. The Nationalists fled to Taiwan, and the US failed to recognize the newly declared People’s Republic of China for years.

In 1949, following the Chinese Revolution, Mao Zedong and his People’s Republic embarked on an international isolationist program. This essentially stifled growth for the Chinese for over two decades. During the Korean War, American soldiers fought the Chinese, and there were serious problems in the islands between mainland China and Taiwan. In recently released government documents from 1954, the US considered using nuclear weapons against China, but restrained that drastic measure. During this tense period, the US and Taiwan signed a mutual defense treaty, that still exists today.

The tense feelings between the US and China stayed that way until the late 1960s. At this time, China and the Soviet Union relations were boiling over. The old adage of “the enemy of my enemy is my friend”, became more relevant. National Security Advisor Henry Kissinger, under President Nixon, seized the opportunity to forge ties with China. Under President Nixon, in 1972, the US re-established bilateral ties with China with the Shanghai Communique and the US recognized the People’s Republic of China. It was in the best interests of both countries to foster a more constructive relationship, especially considering both viewed the Soviet Union as a threat. In fact, both countries fought together in Afghanistan against the USSR.

At this point in time, in the early 1970s, China’s economy was marginal to overall world trade. As an emerging market, China erected trade barriers to build up its embryonic industries. Developed countries accepted these barriers, primarily for security and strategic reasons. Global businesses were intrigued by the sheer size of China’s population and its untapped addressable market. Foreigners dealt with cumbersome bureaucracy, obstacles, structural impediments and downright discrimination just to gain access to this captivating market.

Deng Xiaoping, who took over power from Mao in 1978, pushed an economic agenda called “reform and opening”. China’s spectacular rise was fueled because America hoped that engaging with China would lead to a more open country, both politically and economically. The US also hedged its bets with China, by maintaining strong air and naval forces in the region (in the Philippines and Japan).

Trade:

Following World War II, when Japan and Europe were in ruins, the US accounted for as much as 50% of global manufacturing. In the 1960s, the US still represented 40% of the global economic output. During the 1980s, when Japan truly began to shine, current US Trade Representative Robert Lighthizer, then deputy trade representative under President Reagan, played hardball with this emerging power. The US used Section 301 of the 1974 Trade Act to pressure Japan to open up its markets. The US purchased about 1/3 of Japan’s exports and contributed roughly half of its foreign investment. Considering that Japan was also reliant on the US for its national defense, there was little it could do to fight back.

In textbook economics, trade is often a “win-win” proposition. Two countries that freely exchange goods and services are both better off and receive comparative advantages from fair trade. For the last century, the US had comparative advantages in manufacturing due to its technological prowess, educated workforce, and access to capital. With strong protections for intellectual property and laws, the US was the strongest and largest market in the world.

There continues to be uncertainty and doubt about how current trade disputes will be resolved. Most countries have significant businesses and industries they wish to protect. For example, South Korea has a 57% tariff on agricultural products, and India applies a 33% tariff of imported food. Brazil and China have a 15% and 12% tariff on imported manufactured goods. China erected an auto tariff that is 10x the size of the US’s, while Canada was adamant in protecting its dairy farmers with imported tariffs. Trade and tariffs remain a constant, but individual trade deals can attempt to level the playing field.

The WTO:

The WTO, which the US helped to create in 1995, is the global arbiter of trade disputes for 164 participating countries. In 2001, China entered the World Trade Organization and received numerous benefits for its inclusion. The hope was that by joining the WTO, China would end their state-directed investments and market protections. As China became integrated into the global economy, many were hoping for a series of reforms, like unwinding various state-owned enterprises. The term “Chimerica” encapsulates a new economic world order, that was intended to highlight the combination of China’s massive labor force and savings surplus with America’s consumer-led spending and thirst for cheaper goods. The first decade of China’s WTO admission led to higher returns on capital, by reducing labor costs and depressing the cost of capital (i.e. lower interest rates).

The WTO, which the US helped to create in 1995, is the global arbiter of trade disputes for 164 participating countries. In 2001, China entered the World Trade Organization and received numerous benefits for its inclusion. The hope was that by joining the WTO, China would end their state-directed investments and market protections. As China became integrated into the global economy, many were hoping for a series of reforms, like unwinding various state-owned enterprises. The term “Chimerica” encapsulates a new economic world order, that was intended to highlight the combination of China’s massive labor force and savings surplus with America’s consumer-led spending and thirst for cheaper goods. The first decade of China’s WTO admission led to higher returns on capital, by reducing labor costs and depressing the cost of capital (i.e. lower interest rates).

Updating WTO rules is necessary and is only getting addressed now, because the administration has been so vocal with its displeasure. Europe, Canada and Japan are actively working to reform these rules, before the organization becomes totally useless in December 2019. Why? That is when its appellate body and ruling judges will effectively shut down, leaving the WTO’s dispute settlement powers in disarray. The clock is ticking, and it only has one year left.

Hoping for a strong WTO to play global trading policeman is not a viable strategy. The best solution to these trade disputes would have been for multi-lateral deal, led by the WTO, involving dozens of allied countries. Instead, the WTO has proven to be inept at handling unfair trade practices.

President Trump has criticized the WTO and says that “China continues to violate every single principle” on which the group is based. Chinese officials respond by accusing the Trump administration as a “trade bully”, that is seeking to unwind 40 years of global economic stability. The Trump administration makes claims of China’s abuses, and China responds that the Trump administration is failing to foster a stable global economy and that it is “intimidating” smaller countries. China believes the US is “brazenly preaching unilateralism, protectionism and economic hegemony”.

Will this trade disagreement turn into a trade war? We do not believe it will, but both sides need to fully appreciate the other’s perspective. A solution that allows both to claim victory will not be easy to solve. There have been countless opportunities to fix this growing Chinese problem, but no US leader (nor the WTO) has had the “guts” and determination to solve it.

A School Yard Fight:

The President has broad authority over trade and any items related to national security. He is using these powers to threaten and impose his will on the negotiations. This is an emerging rivalry that seems like schoolyard fight waiting to happen.

The President has broad authority over trade and any items related to national security. He is using these powers to threaten and impose his will on the negotiations. This is an emerging rivalry that seems like schoolyard fight waiting to happen.

The US has won more than 90% of the 123 WTO disputes it has filed. Despite this, some in the administration claim that the WTO is “a failure”. They criticize the Chinese for violating the spirit of its letter to join the WTO in 2001. Complaints include higher than warranted tariffs, government subsidies, currency manipulation, unnecessary barriers to entry, forced transfers of technology and theft of intellectual property. The rules, enacted years ago, have been slow to adapt to digital commerce and other new technology. The Trump administration complains that the WTO gives too much flexibility to developing countries to “skirt rules” that were designed for emerging economies.

Peter Navarro, the director of the National Trade Council recently told CNBC that while the market might be more volatile near term, “you should see this as a bullish move toward a structural realignment of a global economy.” He also said, “In the absence of President Trump basically having a tough stance on trade, of setting the standard that trade must be free, fair and reciprocal, we would not have countries talking to us in earnest like they’re talking to us now.” This seems to be the Trump’s trade strategy. While it might increase market volatility in the short term, the goal is to create lasting, strong and fair-trade agreements.

What is Hank Saying?

As we stated in our 4th Quarter Investor Newsletter (published on SA last month), we have an immense amount of respect for former Goldman Sachs CEO and Treasury Secretary Henry “Hank” Paulson. At the Bloomberg New Economy Forum this month, Paulson stated that an “economic Iron Curtain” may soon descend between China & the US. Seventeen years after joining the WTO, Paulson stated that China “still has not opened its economy to foreign competition in so many areas.”

He further stated that China’s use of joint-venture requirements, ownership limits, technical standards, subsidies, licensing procedures and regulations to block foreign competition is “simply unacceptable”. Paulson’s speech highlighted discrimination against foreign companies has actually done something fairly unusual in this partisan country. It has unified American leaders, across the political spectrum, in the belief that China is a strategic rival whose rise “has come at America’s expense”.

Times Have Changed:

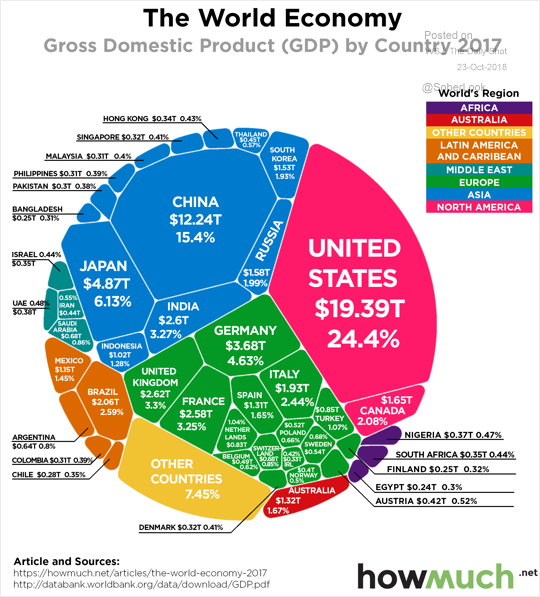

When President Trump placed more than $250 billion of tariffs on China, he cited Section 232 of the 1962 Trade Expansion Act and Sections 301 of the 1974 Trade Act. Today, President Trump likes to highlight how China has a $700 billion trade relationship with the US. However, it also has a $3 trillion trade relationship with the rest of the world.

As the chart above indicates (see article and source data), the US is under one quarter of global GDP, and China has reached an impressive 15%. President Trump may wish to return to a mid-20th century America, but this is not realistic. Everything is no longer made in the US, and this will not be the case going forward. Times change, and using the same legal framework used against Japan in the 1980s will not likely work.

A Trading Game Plan?

One by one, trading deals with be broken and then re-created. The new South Korean deal, according to Peter Navarro, is “a validation of the Trump trade strategy”. We see the game plan as follows. First, threaten penalties to bring a country to the negotiation table. Once there, persuade them to recast trade pacts. When tensions are resolved, hold a symbolic signing ceremony that can then be utilized for political advertisements and proof that “things are getting done”.

However, the mesh of supply chains that have emerged in this global economy are staggeringly complex. Changing trading routes and rules can be unbelievably disruptive to a manufacturing cycle. Will each new trading pact result in vast benefits for the US? Probably not, but deals are getting re-negotiated, and the administration is steadfast in stating that it is trying to protect US interests around the globe. The details have not been released on these new deals, nor has the analysis been completed. Many of these negotiations are vague on details and goals. The timetables are also open-ended. However, even minor tweaks, like regulatory standards and future negotiations, can be wrapped up as a new deal benefitting America.

Wendy Cutler, who negotiated the original US/Korea deal under Presidents Bush and Obama had an interesting takeaway. She said, “the changes made are meaningful, but modest”. Korea likely came with demands of its own, and we assume that the US gave as well as got desired changes. Does each deal have to have a winner at the expense of another country? We do not believe this is a zero-sum game. Symbolic victories are vastly preferable to trade wars.

NAFTA Becomes USMCA:

We believe that the new Nafta deal has set the administrations trading template. No, we have not read the entire agreement. There remains much debate about whether or not the new USMCA is dramatically different from the old NAFTA deal. In our opinion, the market does not particularly care if the new deal is markedly different or beneficial to the US.

The markets seem to have been shrugging off these trade tensions for months. Then, the comments get inflammatory, and the market becomes volatile. We expect this to continue, right up until the sanctions and tariffs are levied.

This appears to be the negotiation tactic the administration wishes to take. Threaten and negotiate through the media. Throw out aggressive comments and penalties, unless the counterparty comes to the negotiation table. The template and trading strategy have been telegraphed.

The Trump administration has initially turned to its allies in Asia (i.e. South Korea) and Europe for trade deals. Even as the US/Chinese relations deteriorate, the market is applauding President Trump is for striking new market opening deals. The revised free-trade pact with South Korea demonstrates that the US can and will make new deals that please both sides. This will likely lead to additional talks and a revised trade deal with Japan. There is already chatter that a European Union expanded framework is in the works. Japan and the European Union are next on the docket, while the UK and the Philippines will shortly follow. It seems that the US trade negotiation tactic is to focus more on using trade deals to confront forces that are distorting global commerce. By seeking tougher, new standards for the flow of trade, the US can steer more jobs and manufacturing back home.

Once the administration set a deal with Mexico, it put a deadline on Canada to adhere. This new deal, re-branded as USMCA, has already forced the hands at several European car makers. Supply chains are being impacted, and more manufacturing should get shifted to North America.

Over the next several months, we anticipate a continuation of this nasty, tit-for-tat trade fight. We look at the US and Europe negotiation as a decent indicator for how the US versus China spat will play out. After imposing stiff penalties on EU steel and aluminum exports, the US pledged not to enforce these tariffs during ongoing negotiations. The two sides continue to meet, and we anticipate an amicable agreement can ultimately be reached. A similar negotiation is occurring with Canada and Japan. Deals have already been struck with Mexico and now South Korea.

Europe:

Currently, the US and EU have an economic partnership that accounts for $1 trillion in annual goods and services trade, with $6 trillion in total foreign – direct investment. The European trade deal will not easy. The pressure tactics used by the administration will not be as successful when it comes to a European Union deal. Why? The EU’s 28-member bloc, with nearly $18 trillion of GDP has the heft and trading power that puts it on a much more even playing field with the US.

Currently, the US and EU have an economic partnership that accounts for $1 trillion in annual goods and services trade, with $6 trillion in total foreign – direct investment. The European trade deal will not easy. The pressure tactics used by the administration will not be as successful when it comes to a European Union deal. Why? The EU’s 28-member bloc, with nearly $18 trillion of GDP has the heft and trading power that puts it on a much more even playing field with the US.

Canada and Mexico were compelled to follow the US’s wishes, or they could have been shut out of the American market. The French Secretary for Europe recently said that “We Europeans are the largest trade power in the world. So, we don’t have to be worried. We don’t have to negotiate under threat.” Only time will tell, especially since the US Trade Representative Robert Lighthizer has touted USMCA as a “paradigm shifting model for all of Washington’s trade policies.”

The Eurozone continues to face numerous hurdles and remains well behind the US in its growth following the Financial Crisis. The 19-nation currency union continues to struggle to deliver the broad-based economic growth that its central bankers would like to see. The European Central Bank or ECB recently lowered its forecast for economic growth in 2018 to 2.0% and 1.8% in 2019. To keep some perspective, Europe is simply slowing from last year’s 2.5% pace.

In prior quarterly newsletters, we have opined on our disbelief regarding negative interest rates. The ECB remains on autopilot, without enough evidence of growth to remove its easy monetary policies. It sounds like the Eurozone remains at least two to three years behind the growth the US is experiencing. Inflation has been much lower (at 1.2%), and unemployment has been much higher (at 8.5%) in Europe versus the US. The ECB can justify continuing its easy monetary measures, maybe even its negative interest rate program. Despite a softer economic environment, the ECB continues to carefully telegraph its plan to phase out its easy monetary policies. While it would like to follow The Fed’s policies, the Eurozone is simply not as strong as our economy. It is winding down its bond-buying program or Quantitative Easing (i.e. QE), but it is accommodating a fragile economy. ECB President Mario Draghi still plans to hold its benchmark interest rate at minus 0.4% through the summer of 2019. In fact, he stated that the ECB will not raise interest rates until “well past” the end of its 2.5 trillion QE, bond-buying program.

However, maybe, just maybe, US technology innovation, solid workforce productivity, tax reform, and energy independence are benefitting our economy versus other developed areas? Maybe the language barriers that exist across countries negatively impacts their job markets. With these European risks still prevalent, the ECB simply cannot phase out its stimulus programs. As we see it, we have left a world of free markets and entered a world of managed economies. Central banks are currently running economic policies are will do everything in their power to prevent another downturn. Instead of globalization and market forces dictating policies, we see more trade conflicts and regionalized pacts.

The Stakes Are Obviously High:

By 2015, China accounted for a tremendous amount of global manufacturing. China was 28% of global auto production, 41% of ships, 50% of refrigerators, 60% of TV’s and 80% of air conditioners and computers. When China entered the WTO, it was 13% of the US’s GDP, on a current-dollar basis. By 2016, it was 60% of our size. Projections by the International Monetary Fund (IMF) are looking for China will be 88% of our size by 2023.

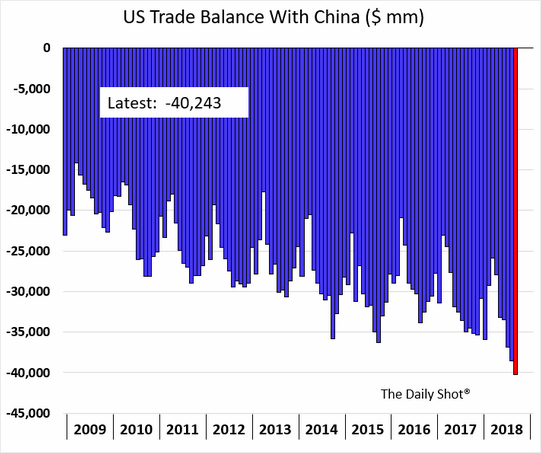

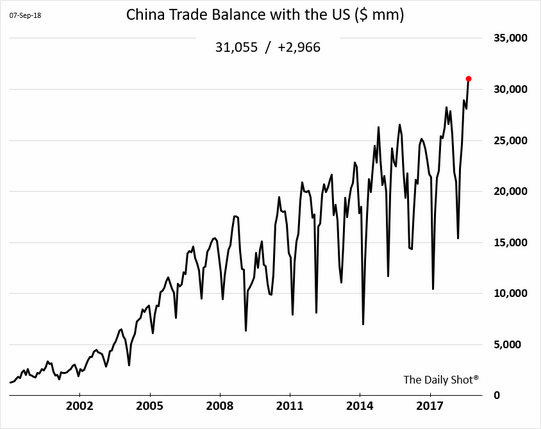

According to US Department of Commerce foreign trade data, the “trade-in goods” deficit with China has increased 45% over the past 10 years. As the chart to the left highlights, the US trade in-balance with China remains awful. In fact, during the month of September, China produced a record trade surplus of $34.13 billion. For the January through September time frame, China’s advantage was a whopping $225.8 billion. This should only intensify an already heated discussion.

Back in 2015 and then again in early 2016, a drop of roughly 3% of the Chinese yuan to the US dollar created panic in the market. The S&P 500 fell more than 10% in a few, short days and the global markets were quite volatile. The plunge was because the market assumed the Chinese government was devaluing its currency to stimulate is sputtering economy. The worry was that this would spread across the globe, and this caused commodity prices to crash and oil to fall. Investors raced to the safety of bonds, with a fear of deflation.

Intellectual Rights:

US businesses are at a crossroads. Some are heavily exposed to China, either for supply chain issues or from a growth market perspective. These are the companies (or farmers) that want to see a truce on trading relations. On the other hand, there are plenty of US companies that are displeased about stolen intellectual property, unfair restrictions or Chinese government subsidies.

One of trade war biggest issues or sticking points revolves around intellectual property rights. Global companies spend trillions on research and development and assume that fair practices will protect their rights. The Trump administration claims that China forces the transfer of foreign technology as a condition for access to the huge Chinese market opportunity. In addition, the US claims that China enforces foreign licensing requirements and foreign-ownership restrictions that tilt in favor of Chinese companies. In fact, new cybersecurity rules published in October give Chinese authorities sweeping powers to inspect any company’s IT, either on the physical site or by remotely accessing corporate networks. China believes it has the right to inspect any company doing business in its country and check for “security loopholes”.

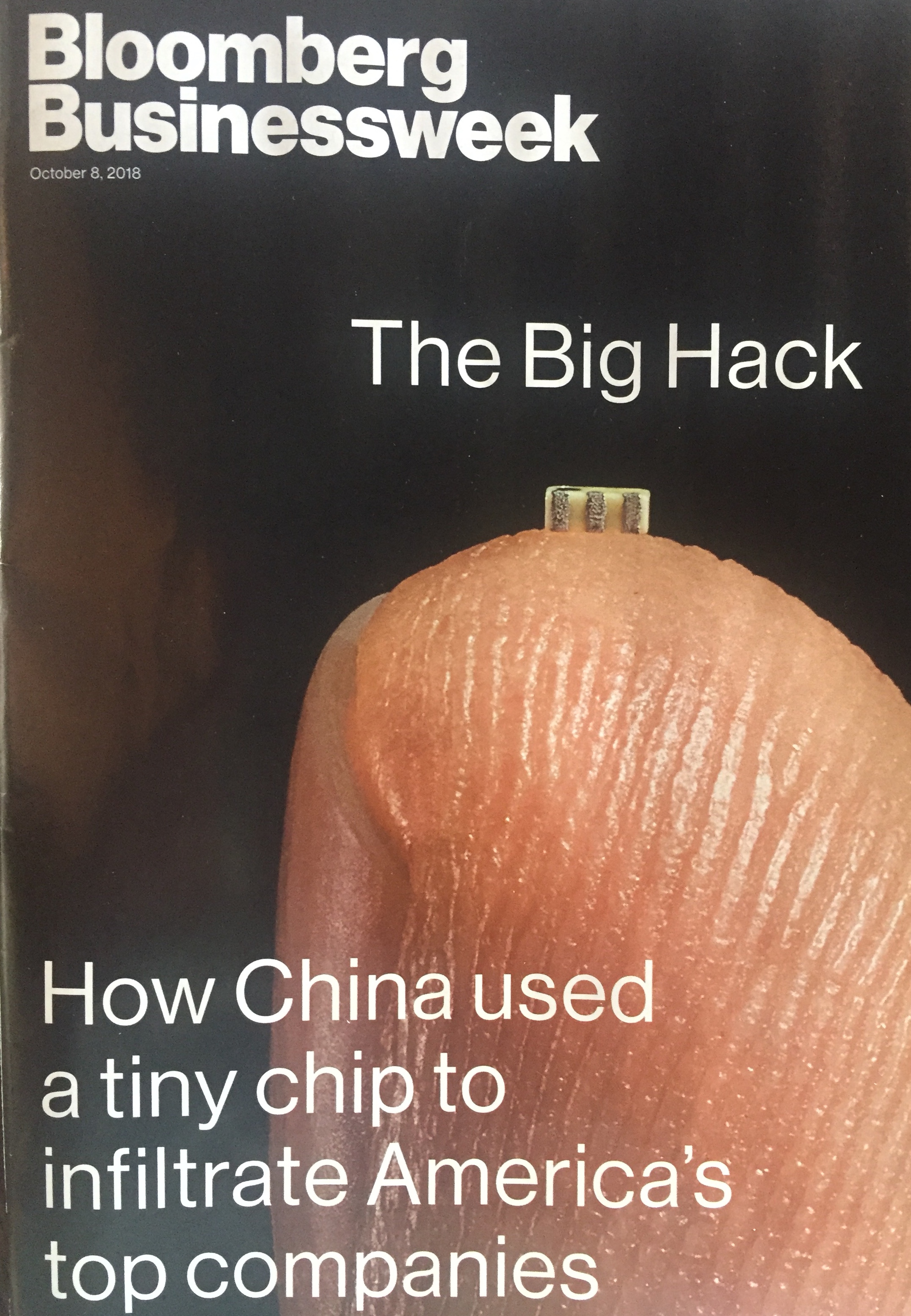

This follows a recent new story from Bloomberg (cover above) that laid out evidence that China used a tiny chip to hack thousands of US companies, including Amazon (NASDAQ:AMZN) and Apple (NASDAQ:AAPL).

Instead of intellectual property theft, China has published a full-throated rebuttal in the form of a state-sponsored whitepaper, published by its State Council. That document says China adheres to a “complete and high-standard intellectual property legal system. The Chinese argue that it does not force foreign firms to enter its market. It says that foreign firms enter into “voluntary commercial contracts” and transfer production capacity and technology willingly. China further states that these foreign firms “are the biggest beneficiaries of technical cooperation”, so no entity is being unfairly treated.

William Zarit, Chairman of the American Chamber of Commerce recently said “It does not seem like our companies have a choice”, if they wish to do business in China. Unfortunately, for the US, China can easily wait this out. They get to plan for the long term and have a leadership in place to execute this plan. The Chinese understand that it only needs to wait out four to eight years before a new leader or set of priorities reins in the US. Using another sports analogy, China can simply “run out the clock”.

Cold War II:

In early October, Vice President Pence gave a speech at the Hudson Institute that was possibly the boldest and most inflammatory speech on China that we have ever heard. Over the course of 40 minutes, Vice President Pence delivered a remarkable and blunt assessment of the US/Chinese relationship. He did not mince words and accused China of abusing its economic power, stealing American technology, bullying our companies, militarizing the South China Sea, intimidating its neighbors, and persecuting religious believers. He denounced the Chinese suppression of the Tibetans and Uighurs, as well as criticized its “Made in China 2025” campaign.

To quote his speech, China has “chosen economic aggression, which has in turn emboldened its growing military.” It was a speech that condemned Chinese military, political, economic and ideological aggression. Besides that, it was lovely! The tension and tone of Vice President Pence’s speech certainly is negative and will play out on various fronts. During the Cold War between the US and the Soviet Union, there was plenty of tension, but little economic ties between the two superpowers. Now that the US and China are so heavily bound together on an economic front, it can play out on so many different levels. The complex relationship between Washington and Beijing is just as tense as the original Cold War, but even more challenging to decipher considering the economic ties and co-dependency.

Just like any country, there are worries plaguing the Chinese economy. The major gauges of China’s economic performance, for the recently completed 3rd quarter, are soft. Their currency has been buoyant, but that is starting to weaken. In mid-October, the Chinese yuan reached 6.9452 per $1 US dollar, which was its weakest level in almost 2 years. While the US Treasury Department has not named China a currency manipulator, its currency is clearly weakening.

The same strategy the US employed against the USSR will not work. A military strategy will not work, against a new economic foe. In an era of cyberwar and climate change, the US must adapt. There are still areas where the two countries can work together to solve problems. For example, North Korea may become a positive solution for both parties. If both sides remain level-headed, this can become a selective cooperation agreement.

President Trump defends his administrations tariff policy by telling allies that the US will no longer tolerate “abuse” on trade and that he seeks to renegotiate what he calls “broken and bad trade deals”. One day, the administration will talk about “no tariffs, no barriers.” It has a team of ardent free traders that discuss its desires for a level global trade field. Then, a day later, President Trump will tweet about applying a 10% tariff on $200 billion of Chinese goods.

The next day, China responded with tariffs on $60 billion of US goods, targeting Trump’s midwestern, political support (i.e. farmers). The very next day, the Trump administration hinted at an additional $267 billion of Chinese products that would be subject to penalties. This would cover virtually 100% of all Chinese products and goods sold into the US.

The Stock Market Shows Who Is Winning:

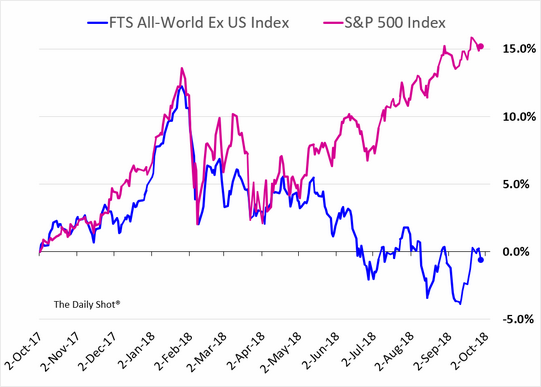

There are no winners in a trade war, only losers; however, as the chart highlights, the early rounds of this title fight seem to be in the US’s favor. Despite the S&P 500 falling in October and November, by roughly 10%, the Chinese stock market has significantly underperformed its US peer.

While the US equity market is up over 300% from the market bottom in March of 2009, the Shanghai Composite is up only 10%. So far this year, the Shanghai Composite is down 35% through mid-November, which is its lowest level in 4 years. Since June of 2015, the Chinese equity market is down well over 50%.

The Chinese stock market is lower today than it was over 5 years ago, and it has fallen by over 30% since its highs set in late January.

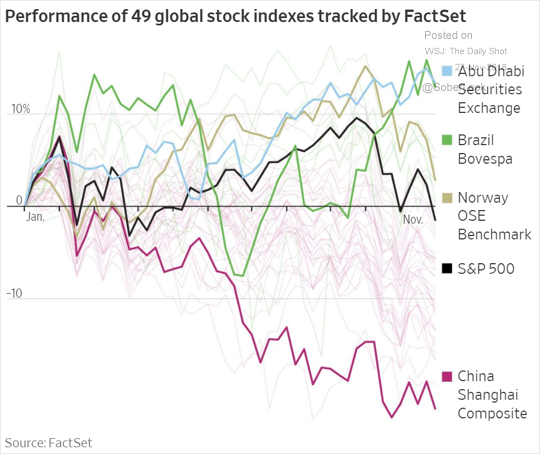

As the chart to the below indicates, other global indexes, especially emerging markets, have dramatically fallen this year. Concerns on tariffs, trade wars and commodity volatility are impacting all global markets. Plus, not all economies have fully recovered from the Financial Crisis. For example, equity markets in Portugal and Greece are still lower than where they were 9 ½ years ago. No country will be immune from a trade war between the two largest economies on the planet.

Chinese Fundamentals:

Why is China down significantly, while the US remains one of the world’s strongest equity markets? There is a confluence of factors, but Chinese growth is slowing, there are debt and liquidity issues, plus the country is negatively impacted by rising oil prices.

Why is China down significantly, while the US remains one of the world’s strongest equity markets? There is a confluence of factors, but Chinese growth is slowing, there are debt and liquidity issues, plus the country is negatively impacted by rising oil prices.

During the 3rd quarter of 2018, Chinese GDP was 6.5%. While many economists do not believe the accuracy of Chinese government data, let us just assume it is truthful. The Chinese government recently claimed that its outlook “is very bright.”, and then it asserted that the US tariffs are more of a “psychological impact, rather than actual impact.” While we are all for positive spin, we believe there is more to this trade war than the Chinese are admitting to. The 3rd quarter 2018 GDP growth rate was its 2nd lowest level ever reported. Ouch!

Chinese investors are clearly concerned about rising debt levels (now estimated at 300% of GDP) and the simmering trade war with the US. The government is beginning to intervene and attempt to lift its markets. To counter an economic slowdown, the Chinese government has plenty of ammunition to bolster their markets. Beijing is trying to boost consumer spending and in September, the government lowered tax rates to stimulate its economy. In addition, Chinese households will now be able to claim deductions for expenses, like healthcare, education, children, and mortgage interest payments. The government also altered banking capital requirements, to spur additional loans and growth. Could China devalue its currency to spur growth? Could it lessen the vast amounts of Treasuries it owns, dumping so much supply onto the market to force an inverted US yield curve? There are so many permutations to grapple with, in this very complex game of chess.

There remain serious humanitarian long-term problems inside of China. There are an estimated 1 million Muslim Uighurs in Xinjiang in “re-education” or modern-day concentration camps. Tibet continues to struggle with repressive Beijing policies. The Communist Party leadership continues to see liberalism and democracy as threats to its rule. In addition, it is upset about recent US sales of arms and weapons to Taiwan, which it still believes is Chinese territory. Recent media reports highlight that China will shortly become the world’s first total surveillance state, with 200 million cameras and plans for another 600 million advanced facial recognition systems. In addition, the foreign policy of China has never been more assertive. The Chinese government is building small islands in the South China Sea and militarizing areas thousands of miles from their coastline. Not only are China’s claims infringing upon their neighbors’ sovereignty, but it flies in the face of international legal rulings. Is China promoting development with its Belt & Road initiative or is it an economic ploy to increase its influence around the world?

Some believe that a clash between the US and China is inevitable, unless China liberalizes politically. This should never be about China’s political system or attempting to create a Jeffersonian democracy. That is not our place to decide. China will never accept the US’s decisions for how to govern or how to control its population.

The road ahead for China is increasingly rocky. Instead of adopting many of the norms of the postwar era, Beijing has rewritten rules in its own favor. How far will their leaders go in curbing the will of their people? Will financial uncertainty at home cause significant unrest inside the mainland? We believe the Chinese leadership has one primary concern for continuing its control and reign. At all costs, Chinese leaders must keep its economic engine growing. Nothing will end Communist rule faster than 400 to 500 million unhappy and unemployed Chinese.

We Are Not Alone:

When Trump withdrew from the Trans-Pacific Partnership (TPP) and then began to question America’s Asian alliances, it signaled a US retreat from the world. President Xi Jinping proclaimed before the Davos elite that China was a defender of the postwar global trading system and was willing to displace the US as economic leader of the world.

Instead of enacting structural changes, President Xi Jinping has launched an anti-corruption campaign and installed himself as leader for life. China will not willingly listen to the US, considering its economy is now 30 times larger than it was 30 years ago. As the second largest economy in the world, it will not simply be content to be a “responsible stakeholder” (as Secretary of State Robert Zoellick’s said in 2005).

The risk is not that the US and China are sparring, but what will occur if more countries decide to side with China and isolate itself against the US. Just like the Chinese are pushing their “Made in China 2025” campaign, the US should strengthen itself through independence. Some US companies should look to build in America, become more independent and re-route some supply chain away from China.

Belt & Road Errors:

China has made a few errors on its ascension to the 2nd largest economy in the world. For example, we believe that Beijing overreached with some of its terms with its Belt & Road infrastructure initiative. China launched this enterprise and promised $1 trillion of infrastructure spending through Eurasia. In the fine print, the world is beginning to understand the dark side of doing business with China.

China’s aggressive building plan came with “strings attached”, and now many countries are beginning to view it as a “debt trap”. Some countries are pushing back against China, when they begin to understand that an inability to repay development loans means greater Chinese presence in their country, as well as losing ownership of key facilities. Malaysia and Pakistan, both long-time Chinese allies, have announced that they will cut back on Sino-funded projects for fear of indebtedness to Beijing. Last weekend, the Chinese embassy in Pakistan was attacked.

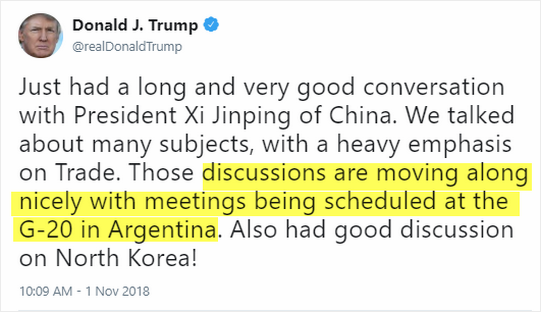

G-20 Meeting in Argentina:

President Trump and Xi plan on speaking at the G-20 meeting this week in Argentina. Do we anticipate any breakthrough on trade to occur? Absolutely not!

The two Presidents will meet, but there is nothing in the pre-meeting commentary to indicate that a complicated and intricate trade war will get settled. The market may be pleased that the leaders are speaking, but we do not anticipate a resolution for months and/or quarters. In fact, during an interview President Trump gave to the Wall Street Journal on Monday the 26th, he said it is “highly unlikely” that the two countries will reach a deal to prevent the 25% tariff on the first $200 billion worth of Chinese goods. He then said that if the talks “don’t go well and we don’t make a deal, then I’m going to put the $267 billion (of additional tariffs) on.”

All the US seems to want is a level and fair-trading environment. Convincing the Chinese to update trading rules will not be an easy task. The best-case scenario is to construct a balanced agreement, that allows both parties to claim victory. Easier said than done, right? We expect heightened volatility for the majority of 2019 or until President Trump wants this Chinese trading issue to “simply go away”. By agreeing to even a minor truce in this trade war, President Trump will certainly claim victory.

We expect President Trump’s campaign to focus on economic and trading success. This has to be Trump’s game plan for re-election in 2020, right? Whether you will vote for President Trump or whoever his Democratic challenger is, his campaign will be centered on a positive economy and numerous, new trading agreements.

Conclusion:

The Chinese / US trade connection is the single most important bilateral relationship in the world. Since it began to open its borders in the 1970s, China has leveraged its 1.4 billion people to become the 2nd largest economy in the world. For decades, many Chinese citizens have been educated in the US and then returned to China to become leaders in both business and government. The China of today is fully capable of competing with foreigners, especially in its home market. China cannot expect to continue to receive accommodations and favorable trade terms when it now is so large and important. It must level the playing field, as its economic development flourishes.

China is not responsible for the US healthcare problems, aging infrastructure, public school system, failed immigration policies or exploding debt. However, China is too large of an economic power to hide behind the same rules it leveraged as a developing country.

The country or region that develops the technology that drives the next revolutionary wave, will ultimately win. Key technologies like automation, robotics, artificial intelligence, blockchain, the Internet of Things, energy independence, blockchain and others. If we can control these advances and technologies, we will remain the pre-eminent economic power in the world.

The US is currently winning this trade war, as evidenced by our stock market return this year. However, both countries will ultimately be losers, if an agreement benefitting both parties cannot be reached.

Warren Fisher, CFA

Manole Capital Management

Disclaimer:

Firm: Manole Capital Management LLC is a registered investment adviser. The firm is defined to include all accounts managed by Manole Capital Management LLC. In general: This disclaimer applies to this document and the verbal or written comments of any person representing it. The information presented is available for client or potential client use only. This summary, which has been furnished on a confidential basis to the recipient, does not constitute an offer of any securities or investment advisory services, which may be made only by means of a private placement memorandum or similar materials which contain a description of material terms and risks. This summary is intended exclusively for the use of the person it has been delivered to by Warren Fisher and it is not to be reproduced or redistributed to any other person without the prior consent of Warren Fisher. Past Performance: Past performance generally is not, and should not be construed as, an indication of future results. The information provided should not be relied upon as the basis for making any investment decisions or for selecting The Firm. Past portfolio characteristics are not necessarily indicative of future portfolio characteristics and can be changed. Past strategy allocations are not necessarily indicative of future allocations. Strategy allocations are based on the capital used for the strategy mentioned. This document may contain forward-looking statements and projections that are based on current beliefs and assumptions and on information currently available. Risk of Loss: An investment involves a high degree of risk, including the possibility of a total loss thereof. Any investment or strategy managed by The Firm is speculative in nature and there can be no assurance that the investment objective(s) will be achieved. Investors must be prepared to bear the risk of a total loss of their investment. Distribution: Manole Capital expressly prohibits any reproduction, in hard copy, electronic or any other form, or any re-distribution of this presentation to any third party without the prior written consent of Manole. This presentation is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use is contrary to local law or regulation. Additional information: Prospective investors are urged to carefully read the applicable memorandums in its entirety. All information is believed to be reasonable, but involve risks, uncertainties and assumptions and prospective investors may not put undue reliance on any of these statements. Information provided herein is presented as of December 2015 (unless otherwise noted) and is derived from sources Warren Fisher considers reliable, but it cannot guarantee its complete accuracy. Any information may be changed or updated without notice to the recipient. Tax, legal or accounting advice: This presentation is not intended to provide, and should not be relied upon for, accounting, legal or tax advice or investment recommendations. Any statements of the US federal tax consequences contained in this presentation were not intended to be used and cannot be used to avoid penalties under the US Internal Revenue Code or to promote, market or recommend to another party any tax related matters addressed herein.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment