Shares of German biotech InflaRx (IFRX) have fallen by 13% since my “Buy the Dip” piece was published in June. I noted that the company reminded me of a prior winner for ROTY, Argenx (ARGX), in that its lead program appeared to be a “pipeline-in-a-product” that could address a multitude of auto-immune and inflammatory diseases.

While much of weakness has occurred recently, I wanted to revisit now that a phase 2b study for lead drug candidate IFX-1 finished enrolling patients and the company reported third-quarter results.

Chart

Figure 1: IFRX daily advanced chart (Source: Finviz)

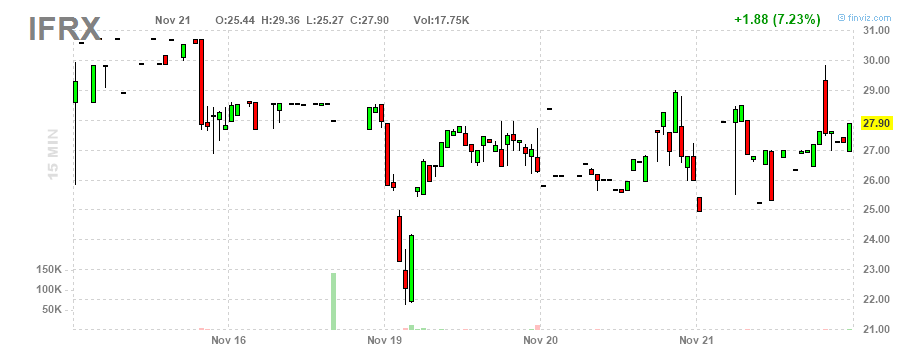

Figure 2: IFRX 15-minute chart (Source: Finviz)

When looking at charts, clarity often comes from taking a look at distinct time frames in order to determine important technical levels to get a feel for what’s going on. In the first chart (daily advanced), we can see shares spent much of 2018 trading in a range (peaked above $40 a few times, now gravitating to mid 20s). In the second chart (15-minute), we can see the very thin trading volume resulting in excessively volatile behavior with shares falling as low as $22 before bouncing back.

Overview

In my last update piece, I outlined the following keys to the bullish thesis:

- A secondary offering in May significantly extended the operational runway, allowing Wall Street to focus on the firm’s potentially lucrative prospects.

- I very much looked forward to data from the company’s Phase 2b study evaluating first-in-class anti-human complement factor C5a antibody IFX-1 in patients with moderate to severe Hidradenitis Suppurativa (HS). I noted that a large market is being addressed (around 200,000 patients in the US alone) of whom 50% do not respond or lose response to Humira (sales set to hit $21 billion in 2020, but generic competition coming by 2023) and that the trial appeared significantly derisked given prior data.

- Lastly, I stated my belief that IFX-1 has a leg up on the competition and that expansion into other autoimmune or inflammatory indications such as antineutrophil cytoplasmic autoantibodies (ANCA)-associated vasculitis (AAV) added substantially to longer-term prospects here.

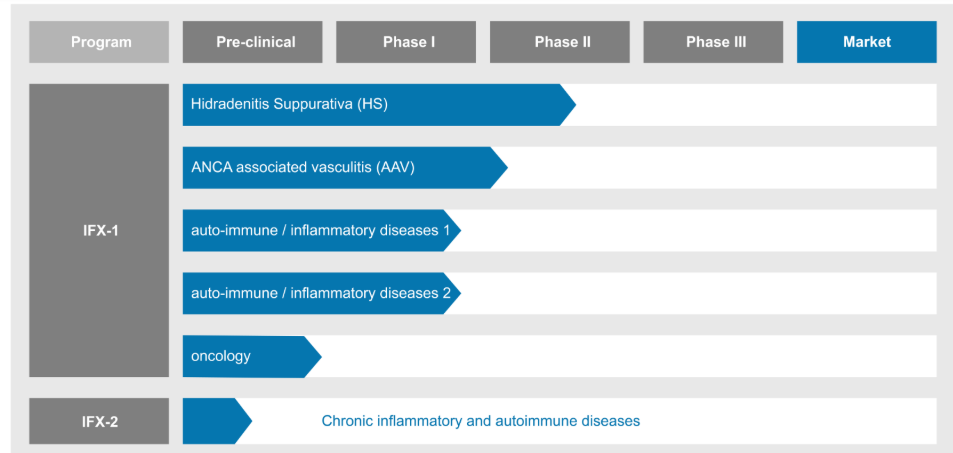

Figure 3: Pipeline (Source: corporate webpage)

Despite recent weakness, my first instinct is that shares are still a good buy here into the upcoming data readout. However, I’d still like to dig into the firm’s Q3 update and other news for any potential red flags or further clues.

Recent Developments

In late October, the company announced that the first patient had been dosed in a mid-stage study evaluating IFX-1 in patients with ANCA-associated vasculitis (AAV). The rare, life-threatening condition affects 40,000 patients in the United States and 75,000 patients in Europe. It’s well established that activation of the complement system (generation of larger amounts of C5a) plays a key role here. 36 patients will be enrolled utilizing a double-blind, randomized, placebo-controlled design comparing two different dose regimens of the study drug to placebo (all patients will be receiving standard of care immunosuppressive therapy and high dose glucocorticoids). While the primary endpoint is safety, Wall Street will be more focused on any signs of efficacy including via the Birmingham Vasculitis Score (BVAS). As for the length of the study, patients will be treated for 16 weeks with an observation period of 8 weeks to follow.

In November, the company announced that patient enrollment had finished up for the phase 2b study evaluating IFX-1 in patients with moderate or severe Hidradenitis Suppurativa (HS). The trial utilizes a placebo-controlled, double-blind design where 4 doses of the study drug are evaluated for 16 weeks (plus a placebo arm) followed by a 28-week open-label extension phase to gain better insights into long-term efficacy. The primary endpoint is dose response signal utilizing the Hidradenitis Suppurativa Clinical Response (HiSCR) score.

Other Information

For the third quarter of 2018, the company reported cash and equivalents of €162.1 million (compared favorably to net loss of just €6.7 million). Research and development expenses more than doubled to €5.5 million.

As for future catalysts of note, the company is guiding for top-line results from the lead program (phase 2b study in HS) to be released in the first half of 2019.

Listening to the company’s lengthy R&D presentation from September, here are a few nuggets that stuck out to me:

- Management continues to emphasize the large niche in the treatment landscape for HS that IFX-1 is likely to fill, as AbbVie’s (NYSE:ABBV) Humira offers only a 50% response rate at 12 weeks and around 50% of patients successfully treated the first time around encounter secondary failure.

- Phase 2a data truly does offer a significant element of derisking, considering that the safety profile was quite clean (of 5 serious treatment-emergent adverse events and 4 mild occurrences, all were deemed not related to study drug). HISCR response rate was very encouraging and improved over time, reaching 83% at Day 134.

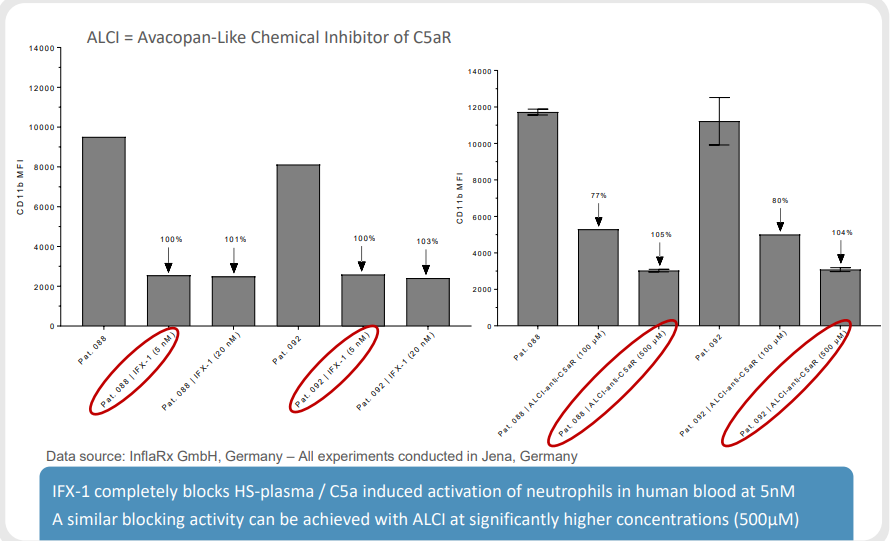

- In minute 33, management takes the time to address competition (namely avacopan from ChemoCentryx (NASDAQ:CCXI)) and refers to in vitro head to head data stating that blocking C5a appears superior to blocking C5aR (difficult to achieve 100% blockade with the latter).

- For the ongoing phase 2b study, I found one aspect of its design intriguing in that when patients transition into the open-label extension study, non-responders will be switched into medium-dose IFX-1 arm, while responders will transition into a low-dose IFX-1 arm (hypothesis is that patients who respond well after 14 weeks might not need full dose to keep disease status stable).

Figure 4: Blocking C5a with IFX-1 versus blocking C5AR with chemical avacopan-like inhibitor (Source: R&D day presentation)

As for institutional investors of note, Adage Capital Partners recently disclosed a 10.45% stake (indicates a high degree of conviction for it). Other key holders include Ra Capital and Cormorant Asset Management.

Final Thoughts

To conclude, this story remains attractive across multiple time frames as lead program IFX-1 has great promise in treating HS patients and additional indications are explored.

For readers who are interested in the story and have done their due diligence, I suggest accumulating shares in the near term.

Risks include disappointing results from the phase 2b study (would be devastating to the bullish thesis) and setbacks with enrollment or initiating studies in separate indications. Competition including from ChemoCentryx should be watched closely. Dilution in the near term does not appear likely given the current cash position and burn rate. Also, take into account volatility due to low trading volumes (limit orders are a must).

Disclaimer: Commentary presented is NOT individualized investment advice. Opinions offered here are NOT personalized recommendations. Readers are expected to do their own due diligence or consult an investment professional if needed prior to making trades. Strategies discussed should not be mistaken for recommendations, and past performance may not be indicative of future results. Although I do my best to present factual research, I do not in any way guarantee the accuracy of the information I post. I reserve the right to make investment decisions on behalf of myself and affiliates regarding any security without notification except where it is required by law. Keep in mind that any opinion or position disclosed on this platform is subject to change at any moment as the thesis evolves. Investing in common stock can result in partial or total loss of capital. In other words, readers are expected to form their own trading plan, do their own research and take responsibility for their own actions. If they are not able or willing to do so, better to buy index funds or find a thoroughly vetted fee-only financial advisor to handle your account.

About ‘ROTY or Runners of the Year’

ROTY is a 500+ member community which provides a welcoming atmosphere where due diligence and knowledge are generously shared. Subscription includes access to our 10 stock model account, Idea Lab, Catalyst Tracker, a very active & focused Live Chat and much more at an affordable price point ($25/month or $200 annually). This article is a small sample of my work, with the majority of my writing being published exclusively for ROTY members (as tickers mentioned at some point could be chosen for the ROTY model account).

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment