In my previous article on Mogo Finance Technologies (OTCQX:MOGOF) I had suggested that Mogo could become a takeover target. More than a year later, Mogo continues to fly solo. But going solo is not a bad because smaller companies are generally more nimble and quicker to adapt to consumer demands. In the past 2 years, Mogo continues to add new features and products to its list of product offerings.

The stock today trades at about $3.50 CDN range. The last time I wrote about Mogo (which was more than a year ago), the stock traded closer to $4.00. Going by the market price alone, this implies that the company’s value has gone down, which I do not agree with. Clearly, there is a mismatch of value.

Mogo continues to be a speculative play and it’s been unprofitable quarter after quarter, but I think Q3-2018 could be a turning point. Over the next few quarters I see Mogo narrowing it quarterly losses through new product offerings and offering a better product than its competition.

Mogo Highlight: Revenue Hit an All Time High

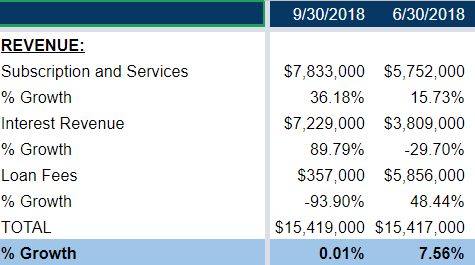

Subscription & Services revenue and Interest Revenue hit reached an all time high this past quarter, Q3-2018. In this same quarter, Mogo exited the short term loan business and this eliminated a quarterly revenue stream of about $4 million to $5.8 million a quarter. The reason Mogo decided to leave the short term loan business was because of tighter regulations surrounding the short term loan industry. More regulations means fewer revenue in the loan fee business so it was a “Short Term Pain for Long Term Gain” type of move. The Loan Fee business in Q2-2018 made up $5.8 million of the total $15.4 million revenue. This is a pretty significant number. Had Mogo continued its Loan Fees business in Q3-2018, Mogo would have added a couple million dollars to its bottom line:

(Source: Mogo Financials)

For Mogo to cancel out its Loan Fee Business that is worth a large chunk of its business is a big move. This was a calculated risk and it also means the company is willing to take a short term loss to grow its longer term business.

Also, it was very good timing for Mogo to cancel its Loan Fee business because interest rates have been on the rise. The Central Bank of Canada has been hiking its interest rate in recent months, and Mogo profits from higher interest rates because of its lending business. Its Interest Revenue business increased by 89.79% from a quarter ago.

What’s even more impressive is despite phasing out its Loan Fees Business worth $5.8 million last quarter, Mogo was still able to beat its prior quarter’s revenue by $2,000.

Given the rising interest rates and the increases in Subscription & Services revenue, this shows that its existing businesses is clearly gaining momentum.

New Product Launches

Mogo initially started out as a lending business for short term and long term loans. Fast forward to today, this Fintech company now offers a pretty comprehensive array of products and services to its customers:

- Mogoprotect subscriptions helps protect consumer’s identity and prevent fraud, launched in Nov 2017

- Mogocard, a prepaid credit card to help consumers manage their spending, launched in Feb 2017

- MogoMortgage, becoming a mortgage broker, launched in Jan 2017

- MogoCrypto, a platform for members to buy and sell bitcoin, launched in Mar 2018

- Started bitcoin mining by leasing 1,000 mining machines from DMG, launched in Jan 2018

What gives Mogo a strong advantage is its speed of bringing new products to market. In recent months, Mogo has been coming out with new products and features, such as the new cash back program for its Mogocard and it is launching MogoWeatlth (an investment related product).

The Market Demand is There

The millennial consumer today uses their cell phone more than any other generation. An article by MarketWatch had commented that “millennial are more likely than other groups to use their phone for educational content, apply to jobs, and learn more about their health condition.” By applying this to a very user friendly mobile app that allows members to check their credit score, apply for a loan, and buy / sell bitcoins, Mogo has designed an app that really caters to the millennial group.

Most Canadians continue to bank with the Big 5 banks in Canada but I believe because Canada’s banking industry is essentially an oligopoly where banks rarely innovate, this presents opportunities for smaller players to carve out niches for itself.

Risk: Mogo Continues to Bleed Red

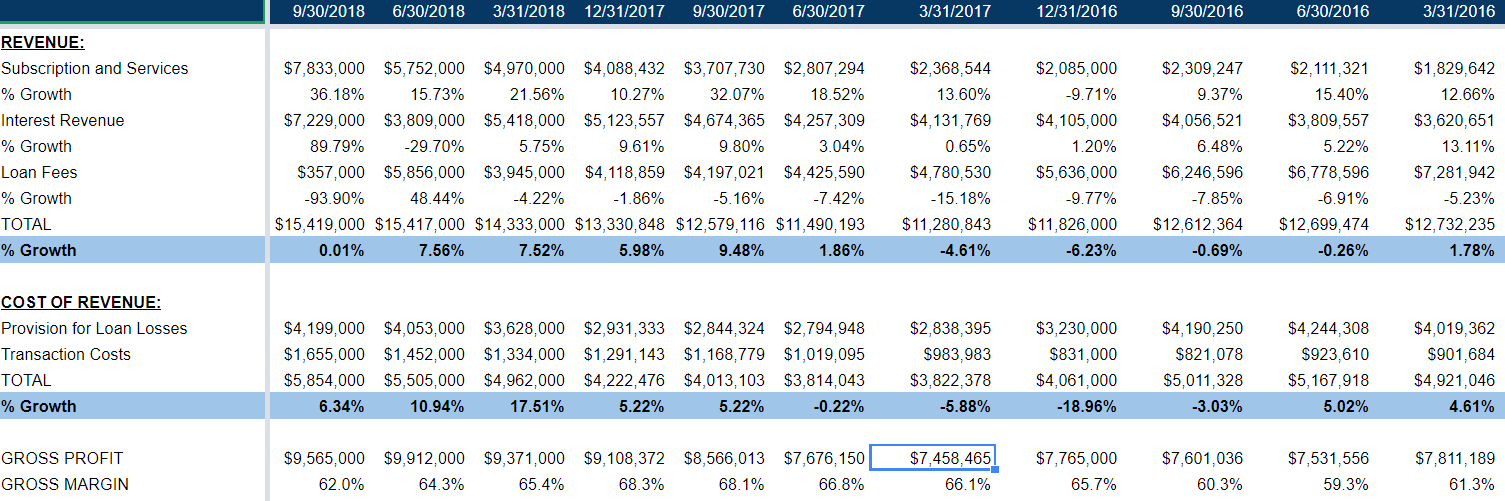

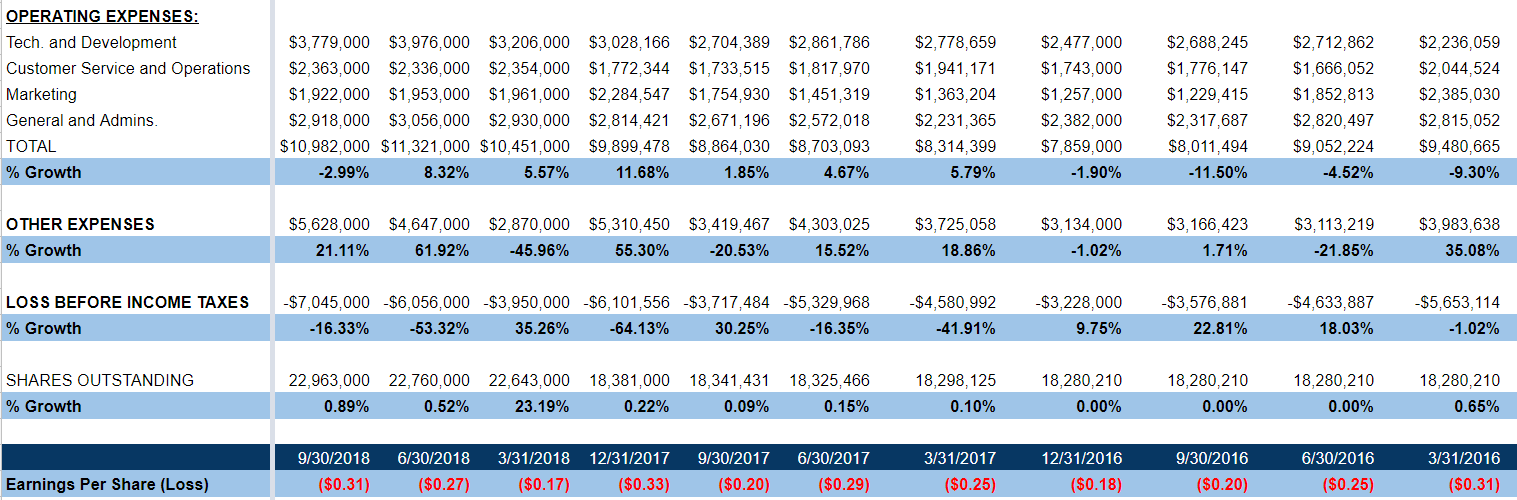

Despite its new product launches and its impressive Q3-2018 revenue numbers, the company is still bleeding money. Its quarterly profits continue to show negative and this loss had widened from a year ago:

(Source: Mogo Financials)

Its Q3-2018 loss is the second largest when compared to the last 11 quarters. This means that Mogo faces a problem where its expenses keep surpassing its revenue quarter over quarter. It doesn’t matter how much Mogo makes because if it can’t control its costs then it may eventually bleed itself to bankruptcy.

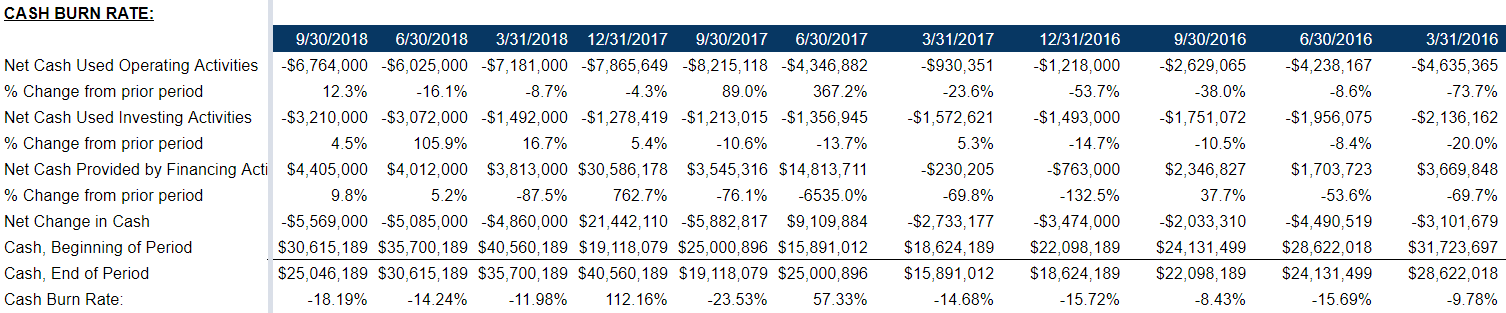

The silver lining here is its cash position remains strong. It raised new equity in Q4-2017 and its current cash sits at $25 million. In the past 4 quarters, its cash burn rate has been about $5 million a quarter so it has about 4 minimum before a new round of equity or debt financing is required:

(Source: Mogo Financials)

Speculative Buying Opportunity

When bitcoin was rising in price in late 2017, a number of companies jumped on the wave by changing their company name to something cyrpotcurrency related. These companies saw a rise in their stock price. Mogo did not do a name change but it did get into the bitcoin business by launching MogoCrypto and started a division to mine for bitcoin. This news created a lot of excitement because around the time that bitcoin’s price peaked in late 2017, Mogo stock price hit a 52 week high of $8.59 CDN.

When the price of bitcoin plummeted shortly after Dec 2017, Mogo’s stock price also fell in tandem. I believe this is where the opportunity is. There is a mismatch of what the market thinks Mogo is worth to what Mogo should be valued at. I think Mogo has potential and its current stock price doesn’t reflect this. Mogo has carved out a niche for itself and its mobile software is becoming a great tool to connect with millennial. Most of all, Mogo is actually making products that people do want and need.

Playing the long game, the millennial generation will need financial advice and they will gravitate to the ones that speak their medium: the smartphone. I rank this company a buy because of rising interest rates and revenue from its services and subscription has grown, but also understand that the caveat is Mogo needs to control its costs.

I’m bullish on Mogo Finance Technologies

Disclosure: I/we have no positions in any stocks mentioned, but may initiate a long position in MOGO over the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Be the first to comment