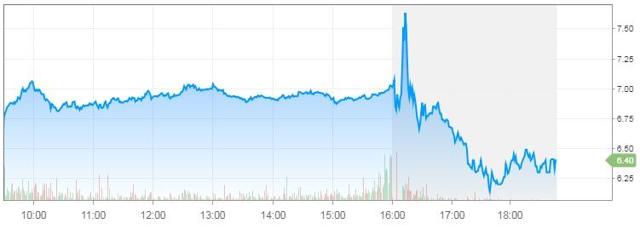

After the bell on Thursday, shares of camera company Snap (SNAP) initially jumped when the company reported top and bottom line beats with its Q3 results. Unfortunately, as the quarter was further digested, shares took a tumble as seen in the chart below, just as they did after the Q2 report, falling to a new post-IPO low. While some progress was made during Q3, things aren’t where they need to be just yet.

(Source: cnbc.com)

Revenues of $297.7 million smashed street estimates for $283.2 million, although I should note that weak guidance a few months ago sent street expectations down about $7 million between reports. The non-GAAP loss of $0.12 per share also beat estimates by two cents, as the company narrowed its net loss and negative Adjusted EBITDA figure.

This time around, guidance was a bit better, although the midpoint of the company’s forecast for revenues of $355 million to $380 million was still below the street midpoint of $371 million. The good news is the negative Adjusted EBITDA number is also expected to improve, but Q4 is the company’s highest revenue quarter of the year. We’ll see what happens in Q1 2019 when the top line falls due to seasonality.

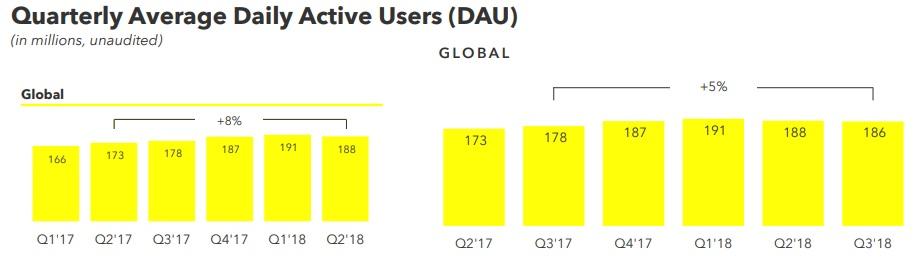

Unfortunately, the biggest problem here is that the company cannot get its user base growing. As you can see in the graphic below, this was the second straight quarter where daily active users declined. For a company with less than 200 million users, there should be plenty of growth, as a name like Facebook (FB) has no problem growing with more than 2.2 billion users.

(Source: Snap Q3 investor slides)

(Source: Snap Q3 investor slides)

Snap will only be facing even higher base numbers for the next couple of quarters, so unless things improve, we may see a decline in the year over year user base number very soon. The big problem here is if users are declining, what are advertisers to do? I know that many have criticized Facebook over privacy and other concerns, but it still is the best place for advertisers to be.

While Snap did improve its bottom line and other financial metrics a bit, the company again burned through a bit of cash, this time $159 million. Cash and marketable securities finished the period at just over $1.41 billion, compared to just under $2.30 billion a year earlier. Large cash burn was one of my biggest concerns when the company went public, and those who have followed my recommendations on this name have done quite well. The number of shares outstanding has also risen by 9.4% in the last five quarters.

Currently in the after-hours session, Snap shares are trading at $6.40, which is below the lowest point they’ve ever traded at during market hours. I warned that hitting single digits was only the beginning, and things have deteriorated quite a bit since. At this point, outside of some other company or firm thinking a buyout makes sense, I don’t see why shares should rise until this company can not only get its user base growing again, but do so without burning tons of cash that will require a massive capital infusion. If you want to be in this space on the long side, Facebook remains my preference at this point, because the social media giant offers more short term growth potential at a reasonable valuation and has a rock solid balance sheet.

Author’s additional disclosure: Investors are always reminded that before making any investment, you should do your own proper due diligence on any name directly or indirectly mentioned in this article. Investors should also consider seeking advice from a broker or financial adviser before making any investment decisions. Any material in this article should be considered general information, and not relied on as a formal investment recommendation.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment