Investment Thesis

Rogers Communications’ (RCI) EBITDA margin continued to expand in Q3 2018. Similar to the first two quarters in 2018, the company benefited from strong wireless subscribers adds and average revenue per user growth rate. We believe Rogers will be able to maintain or expand its EBITDA margin as it has a much-improved wireless churn rate, robust growth in its cable Internet segment, and favorable outlook. The company is currently trading at a valuation slightly above its peers.

RCI data by YCharts

Rogers’ Excellent Q3 2018

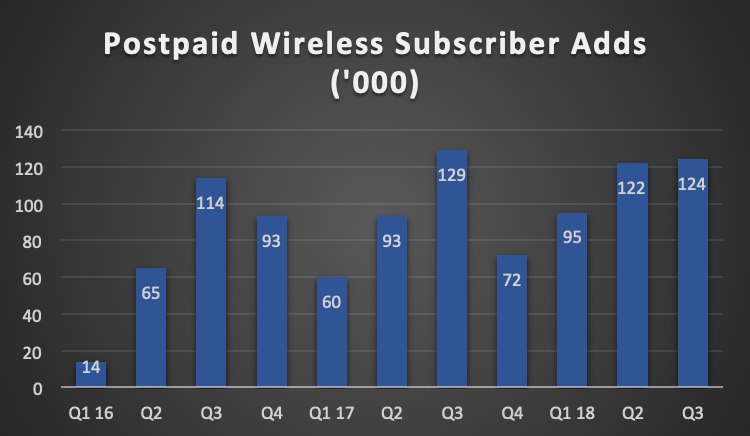

Rogers had another excellent quarter. The company added about 124,000 wireless postpaid subscribers in Q3 2018. The subscriber addition was 2,000 more than the addition of 122,000 subscribers a quarter earlier. We think this is impressive because Rogers continues to face the headwind of government subscribers migrating from its network to BCE (BCE) in the past few quarters.

Source: Created by author; Company Reports

Rogers’ EBITDA margin has been improving in the past few years. As can be seen from the table below, its wireless EBITDA margin improved to 47.1% in Q3 2018 from 46.2% in Q3 2017. Similarly, its cable EBITDA margin also improved to 49.8% in Q3 2018 from 48.2% in Q3 2017.

|

Q1 17 |

Q2 |

Q3 |

Q4 |

Q1 18 |

Q2 |

Q3 |

|

|

Wireless Adjusted EBITDA Margin (%) |

41.4 |

44.1 |

46.2 |

42.2 |

42.6 |

46.5 |

47.1 |

|

Cable Adjusted EBITDA Margin (%) |

43.3 |

46.6 |

48.2 |

N/A |

44.7 |

46.6 |

49.8 |

Source: Created by author; Company Reports

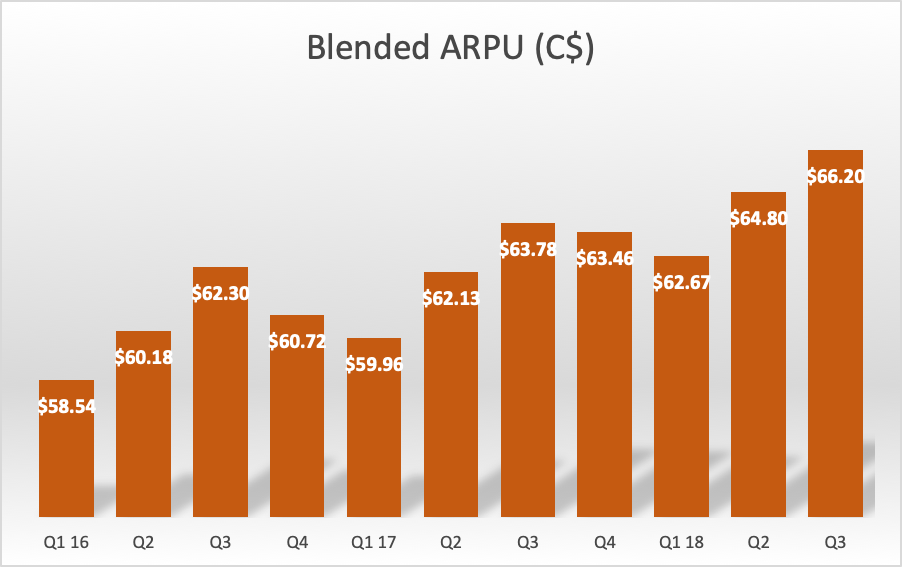

The increase in its wireless margin is due to its subscriber adds as well as healthy average revenue per billing user growth rate. As the chart below shows, its blended ARPU increased to C$66.20 in Q3 2018. This is an increase of 3.8% year over year. Compare to its peers who only registered about 1%~2% ARPU growth rates in the previous quarter, we think Rogers performed quite well in Q3 2018.

Source: Created by author; Company Reports

2018 Guidance revised upward

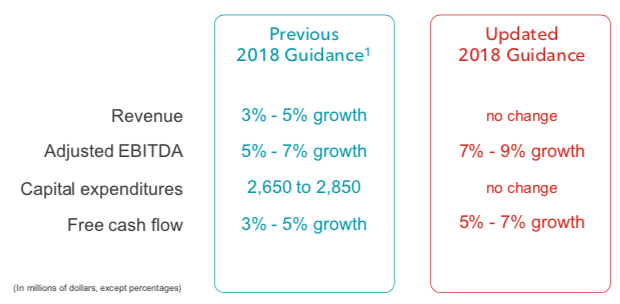

As a result of the company’s outperformance in the first three quarters of 2018, Rogers revised its 2018 guidance upward. It now expects 7% to 9% adjusted EBITDA growth (see table below). Rogers also revised its free cash flow growth rate to 5% ~ 7% (from 3% ~ 5%).

Source: Q3 2018 Investor Presentation

Reasons why we believe Rogers can maintain or expand its EBITDA margin

Good customer satisfaction

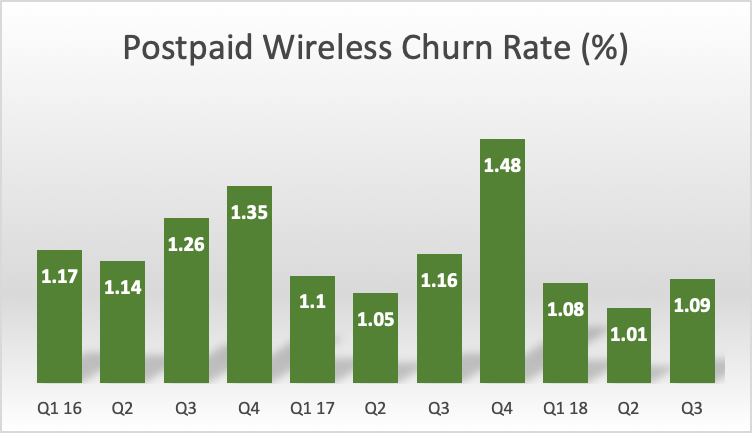

One area where Rogers has done well to expand its EBITDA margin is through customer satisfaction improvement. As management stated in its conference call, customer service improvement and cost savings go hand-in-hand. One metric to look at is Rogers’ churn rate. As the chart below shows, its postpaid wireless churn rate of 1.09% in Q3 2018 is an improvement of 7 basis points from the same period a year ago. Its churn rate in Q3 2018 is also 17 bps higher than two years ago.

Source: Created by author; Company Reports

Management is confident about its wireline Internet business

Rogers’ cable Internet business now represents about 55% of its cable business. As its Internet business continues to grow (35 thousand net subscriber additions in Q3 2018, and 8% revenue growth), its margin should improve as Internet services typically have higher EBITDA margin than its traditional TV business. In addition, the company has launched its Ignite TV platform. As management indicated, its cable EBITDA margin expanded by 160 basis points year over year.

Growth in data consumption will support its ARPU growth

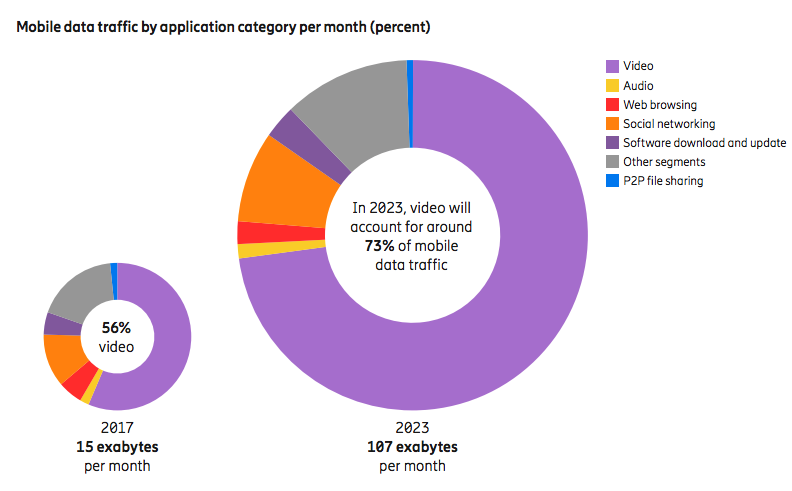

In a report published by Ericsson, worldwide monthly data traffic per active smartphone is projected to grow from 3.4GB in 2017 to 17GB in 2023. This is a growth rate of 31% annually. Majority of the demand for data will be from video streaming. Video applications will account for 73% of mobile data traffic in 2023. This will be much higher than the ratio of 56% back in 2017. We believe Canada’s data consumption will also grow rapidly. This should support Rogers’ ARPU growth momentum in the next few years. Besides strong growth in data consumption, Rogers should also benefit from the rise of 5G and the future of Internet of Things.

Source: June 2018 Ericsson Mobility Report

Valuation

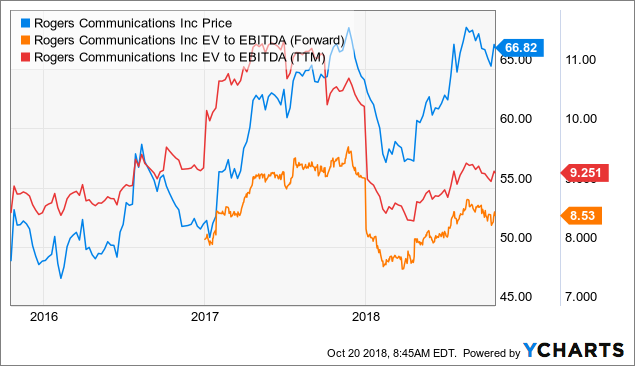

Rogers is currently trading at a price to earnings ratio of 18.8x. This is about 1.8x multiples below its 5-year average of 20.2x (It was 2.8x multiples below its 5-year average about 3 months ago). Its EV to EBITDA ratio of 9.3x is slightly above its 5-year average of 8.9x.

|

Current |

5-year |

|

|

Price to Earnings Ratio |

18.8x |

20.6x |

|

Enterprise Value to EBITDA Ratio |

9.3x |

8.9x |

Source: Morningstar

RCI data by YCharts

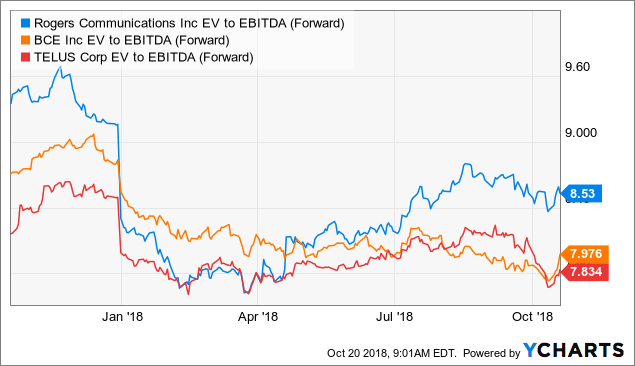

Compare to its peers, Rogers is currently trading at a premium. Its forward EV to EBITDA ratio of 8.53x is slightly above BCE’s (BCE) 7.98x and Telus’ (TU) 7.83x. We believe Rogers’ valuation is warranted because its wireless revenue represents a higher percentage of its total revenue than its peers. In addition, its wireless business continues to outperform its peers.

RCI data by YCharts

Rogers pays a quarterly dividend of C$0.48 per class B share. This is equivalent to a dividend yield of 2.9%. The company has not increased its dividend since 2015. The company has chosen not to increase its dividend, as they would prefer to use the cash towards future growth projects (e.g. spectrum auction, 4.5G network upgrade) and improve its balance sheet.

RCI data by YCharts

Risks and Challenges

Competition from Shaw Communications in wireless segment

Rogers continues to face competition from Shaw Communications, the new incumbent who entered the wireless market back in 2016. At the moment we have not seen any signs of deceleration in its wireless growth momentum. However, as Canada’s wireless penetration rate gradually moves towards 100% (currently at 87% based on Rogers’ recent conference call), competition may intensify. This may hurt Rogers’ revenue and EBITDA growth rate and result in lower EBITDA margin.

Competition from BCE in wireline Internet segment

As BCE gradually completes its FTTH upgrade in Ontario, the company will be able to offer Gbps speed Internet to its customers. Hence, Rogers’ wireline Internet business is expected to face intensified competition. This may impact Rogers’ cable Internet margin.

Investor Takeaway

Rogers should be able to maintain its EBITDA margin thanks to its low churn rate, favorable outlook in the Canadian wireless market, and continual growth in the cable Internet. We believe the company’s share price is fairly valued. Given its positive outlook, we believe any pullback will be a good investment opportunity.

Note: This is not financial advice and that all financial investments carry risks. Investors are expected to seek financial advice from professionals before making any investment.

Thank you for reading. If you like my article, please scroll to the top of the article and click on “follow” to receive future updates.

Disclosure: I am/we are long SJR, RCI.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment