Introduction

About six months ago, I wrote an article about Kenmare Resources (OTC:KMRPF), as I had the impression the company had just turned a page as the higher ilmenite and zircon prices were boosting the company’s revenue and financial performance. The free cash flow in 2017 was strong, and after publishing decent results in the first half of the year, Kenmare Resources has now unveiled a new dividend policy on its Capital Markets Day. I think this will put the company on a lot more radar screens.

Source: londonstockexchange.com

Kenmare has its main listing on the London Stock Exchange where the average daily volume is approximately 250,000 shares (for a total dollar volume of almost $1M). The ticker symbol in the UK is KMR.

Don’t let the amazing first semester fool you

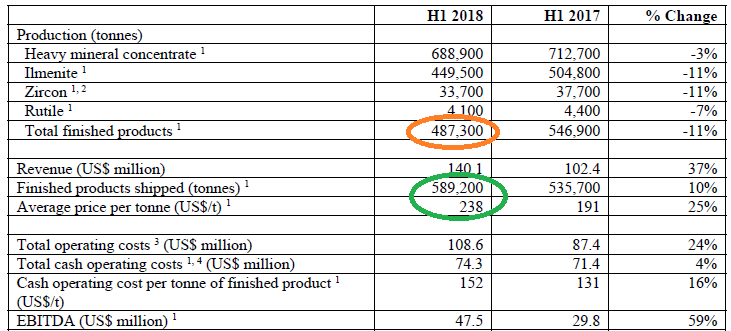

Kenmare Resources proudly announced a 10% increase in the total amount of products it has shipped from its operations in Mozambique. That’s absolutely great, and the higher sales volumes combined with a 25% price increase of the sold product is an excellent development, but there’s a catch. Although the company has shipped 589,200 tonnes of finished product, it produced just 487,300 tonnes of product which means it has sold quite a bit of unfinished products it had on the balance sheet last year. That being said, the total amount of heavy mineral concentrate decreased by just 3%, and I would expect the company to ramp up its production of finished products in the second half of the year when the Mineral Separation Plant can return to a 100% utilisation rate.

Source: press release

This isn’t anything to worry about as Kenmare’s H1 production remains in line with the full-year guidance of approximately 1.07M tonnes of finished product. The company has also indicated it expects the production level to increase in the second half of the year, which should result in a lower cost per tonne of produced finished product. Just keep this in the back of your mind when you look at the company’s H1 results.

Source: financial results

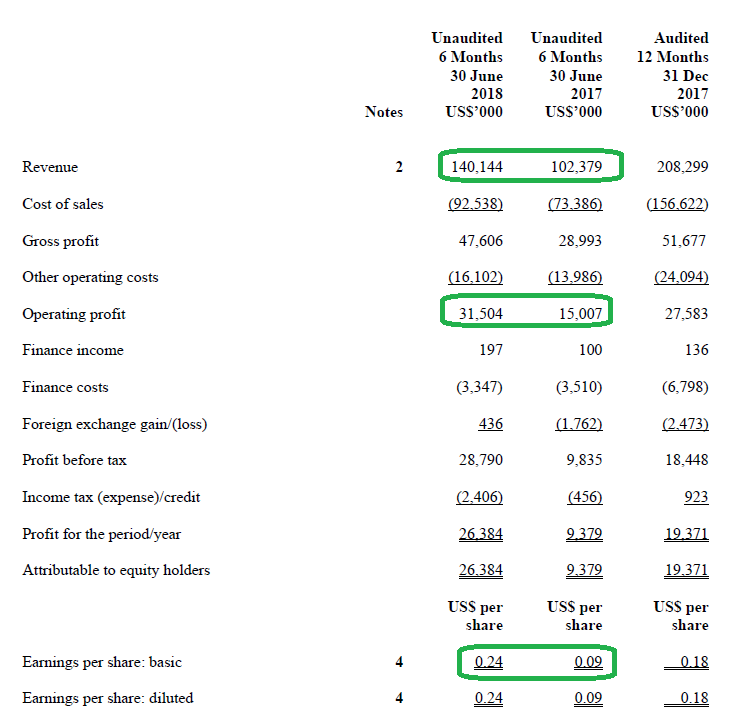

Thanks to the strong commodity prices, Kenmare Resources is actually doing very well. Its revenue increased by approximately 37% to $140M, and gross profit in the first half of the year was almost as high as the gross profit in the entire financial year 2017. This resulted in a pre-tax income of $28.8M and a net income of $26.4M. The tax bill remains low as it looks like Kenmare is able to apply ‘retained losses’ to its taxable income. This will help the company to keep its tax bill low for the next 2-3 years, but investors will have to keep in mind a higher tax bill will be inevitable down the road.

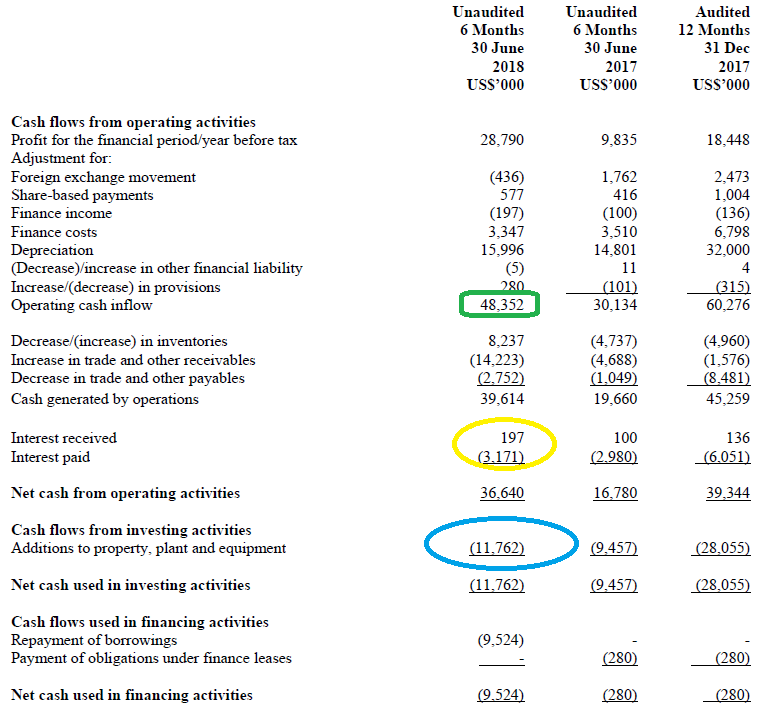

The cash flow results support the excellent net income. Kenmare reported an operating cash flow of $48.4M and after taking the interest payments (and the taxes due but not paid) into consideration, the adjusted OpCF is approximately $43M. The total amount spent on capex in the first half of the year was just below $12M, which means the company remains on track to keep its sustaining capex limited to $22M this year. I do expect the capex to increase in the second semester, but that will include some non-sustaining capital expenditures as well.

Source: financial results

This means that – if Kenmare would be able to replicate its strong H1 results in the second semester – the company will be generating approximately $60-65M in free cash flow this year. That’s approximately 47.7M GBP or 43 pence per share (using the mid-point). Rounding this result down for fluctuations in the shipment schedule, I think assuming a FCF of 40 pence per share would be very reasonable for this year. This means that at the current production profile, Kenmare is trading at just 6 times its free cash flow result. And yes, that’s cheap.

The big news? A new dividend policy

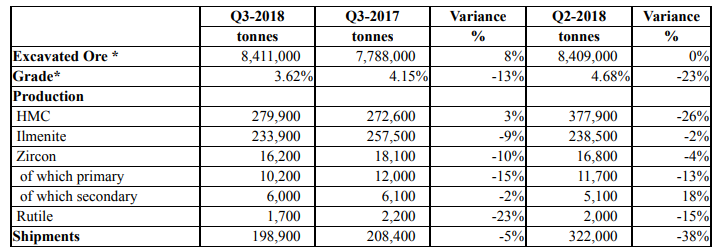

Kenmare reported its Q3 results on its Capital Markets Day earlier this week, and I think this update has reassured a lot of investors. The production of Heavy Mineral Concentrate increased by 3% to almost 280,000 tonnes, but as expected, the total shipments of finished products decreased to just short of 199,000 tonnes which confirm the slowdown of shipped products.

Source: press release

Kenmare has now shipped a total of almost 790,000 tonnes of finished product and remains on track to ship in excess of 1 million tonnes of product this year. On top of that, Kenmare appears to be confident it will see another production (and perhaps shipment?) increase in the final quarter of the year. Kenmare has in excess of 180,000 tonnes of finished product ready to be shipped, representing a value of roughly US$40M.

After the refinancing in 2016 and the excellent performance in 2017 and the first half of the year, Kenmare’s production profile and balance sheet are now ready to support a dividend. On the Capital Markets Day, Kenmare announced a new dividend policy, returning 20% of its net income to its shareholders as a dividend.

Based on the financial results in the first half of the year and extrapolating those results to the second half of the year, I think Kenmare should be in a position to report a net income of approximately US$0.40-0.45 per share, which is approximately 30-34 pence. Applying a 20% payout ratio would result in an anticipated dividend of 6-7 pence per share for a dividend yield of 2.5-2.8%.

That’s a very moderate dividend but this is just a start, as the board of directors has improved a capex program intended to increase the production rate of ilmenite by an additional 20% (to 1.2 million tonnes per year) from 2021 on. A first step will be to install and commission a new 12,000 tonnes per day dredge and Wet Concentrator Plant for US$45M (with an IRR of in excess of 30%) followed by a US$100M development of the higher grade Pilivili deposit. A full feasibility study will be published in Q1 2019, but I don’t expect the total development cost of $100M to change.

By paying just 20% of its net income as dividend, Kenmare should be in a strong position to fund its expansion plans with the cash flow from its current operations.

Investment Thesis

As I expected in May, Kenmare has now really turned a corner and is in a better shape than ever. With $84M in cash on hand and a net debt position of just $9M, Kenmare could easily fund its expansion projects while sustaining an even higher payout ratio than the 20% it will apply the first few years. But as the company was on the brink of collapsing a few years ago, I can only applaud the management’s decision to not rush into things.

But at the current titanium feedstock metal prices and the anticipated 20% production increase, I think Kenmare could become a dividend champion from 2021 on. Based on this year’s anticipated results, I think a payout ratio of 60% would result in a dividend of 22 pence per share. However, I also expect the total tax bill to increase around the same time, so after taking that into consideration, I am anticipating Kenmare to pay an annual dividend of 15-17 pence per share from 2020 on, representing a dividend yield of 6-7% based on the current share price. The official mine life of the Moma mine in Mozambique is approximately 40 years, but it will be up to Kenmare to maximize the efficiency and keep the cash flows and net income stable.

I have a small long position in Kenmare but am planning to increase this position on the back of strong cash flows and the new dividend policy.

Consider joining European Small-Cap Ideas to gain exclusive access to actionable research on appealing Europe-focused investment opportunities, and to the real-time chat function to discuss ideas with similar-minded investors!

Take advantage of the TWO-WEEK FREE TRIAL PERIOD and kick the tires!

Disclosure: I am/we are long KMRPF.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment