Background

Honeywell’s (NYSE:HON) shareholders soon have a decision to make, should they sell, hold or buy more shares of Garrett’s (GTX) stock which is being given to them. The answer might not be as straightforward as it seems. For those of you unfamiliar with Garrett following Honeywell’s spin-off, here is a brief background of the company, right from its Form 10.

Garrett designs, manufactures and sells highly engineered turbocharger and electric-boosting technologies for light and commercial vehicle original equipment manufacturers (“OEMs”) and the aftermarket.

Garrett’s products are highly engineered for each individual powertrain platform, requiring close collaboration with our customers in the earliest years of powertrain and new vehicle design. Turbocharging and electric-boosting products enable our customers to improve vehicle performance while addressing continually evolving and converging regulations that mandate significant increases in fuel efficiency and reductions in exhaust emissions worldwide.

I was very excited when Honeywell first announced that it would be spinning-off its transportation systems. When I first read Garrett’s Form 10 it was impressive to me, though I had a number of concerns. Let’s start with the positives.

Garrett has a number of important competitive advantages which I believe are essential for success in the automotive industry. To begin with, the firm is a low-cost producer. This is essential as the automotive industry is increasingly commoditized and companies look to source for the cheapest. Secondly, I like the fact that the company works with OEMs and has established business-to-business relationships. When companies collaborate on this scale, it usually means that they have strong working relationships and are interested in developing solutions together. For investors, this means strong and predictable income, which usually goes out over a number of years. Indeed, this is exactly what is taking place at Garrett.

Source 1: Investor Presentation

I was impressed by the company’s technology, forward-looking management and diversified revenue stream. The company is focused on pivoting its business to the electrified vehicle industry, and for a company that operates in the automotive sector, it is not dependent on any customer to a great degree. These were positive signs.

We stand to benefit from the increased adoption of hybrid-electric and fuel cell vehicles and the increased need for turbochargers associated with increased sales volumes for these engine types. IHS estimates that the production of electrified vehicles will increase from approximately six million vehicles in 2018 to approximately 22 million vehicles by 2022, representing an annualized growth rate of approximately 39%. OEMs will need to further improve engine performance for their increasingly electrified offerings, and our comprehensive portfolio of turbocharger and electric-boosting technologies will help OEMs do so. We expect to continue to invest in product innovations and new technologies and believe that we are well positioned to continue to be a technology-leader in the propulsion of electrified vehicles.

Source 2: Form 10

Valuation

Investing in spin-offs is always interesting because there can be a significant amount of volatility when the stock first begins trading. A large number of investors are unwillingly given shares and often don’t want to hold stock in a small-cap company; this often causes the stock price to move sharply downward. I believe this could well be the case for Garrett. Let’s examine why:

Honeywell currently has a market cap of ~$123 billion. The company is issuing 1 share of Garrett for every ten shares of Honeywell that trade in the market. Since there are 740 million shares of Honeywell outstanding, Garrett has 74 million shares outstanding and a market capitalization of ~$12 billion. With the revenue and EBITDA numbers that the company is putting up, I believe that the valuation is still slightly stretched. Garrett is a strong company but it has a number of important liabilities which need to be paid and a mediocre capital structure. With EBITDA numbers of ~$350 million, the company would be trading at around 35 times earnings. That is a very expensive price to pay for a company in a low growth space like turbochargers, even if the fundamentals of the business are strong.

I believe that the valuation of Garrett is on the high end, simply because Honeywell has been coming out with some amazing numbers recently. The stock has run up in price significantly and the businesses’ spin-offs are already priced into the stock. I believe that Garrett needs to dip significantly in price before it becomes an attractive investment from a risk/reward perspective.

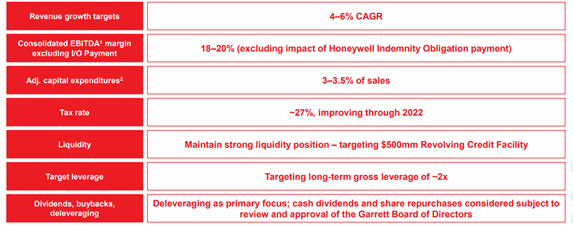

Source 3: Investor Presentation

Risks of owning the stock

The biggest red flag I saw in the Form 10 is that Honeywell is transferring responsibility to Garrett for certain Transportation Systems liabilities in connection with the separation. These are asbestos liabilities which date back to the 1920s. Honeywell is a defendant in asbestos personal injury actions mainly related to legacy Bendix Friction Materials business. Garrett has entered into an indemnification agreement with Honeywell as a means to create an obligation for Garrett to pay annually while not transferring the actual legal obligation for the liability.

This is dangerous, as the settlement amount seems unclear. Although Honeywell will retain legal obligation related to liability and continue to manage claims and administrative processes, Garrett will be required to pay the cost (although it can never be more than $175mm in any given year). Honeywell will only be responsible for 10% of the Bendix liabilities. Given the fact that this newfound spin-off has just had a massive liability lumped onto it, I would be very weary. Lawsuits are unpredictable and there is no way of knowing how much money Garrett could be on the hook to pay.

What should Honeywell shareholders do?

If I was a shareholder of Honeywell I would consider selling off my shares in Garrett if the company sells in the marketplace for a valuation of $12 billion. I think that is too rich of a price for a company with these kinds of growth numbers. Yes, the company has an attractive future ahead, but that does not mean that it is worth its valuation. Additionally, the asbestos liability is a major red flag which carries risk that cannot be calculated.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment