by Daniel Shvartsman

I wrote this in another article, but one of the things I love about Seeking Alpha is not that we have tens of articles a week about Tesla (TSLA) going back and forth, but that intelligent debates pop up around obscure stocks. And it’s hard to get more obscure than Brighthouse Financial (BHF).

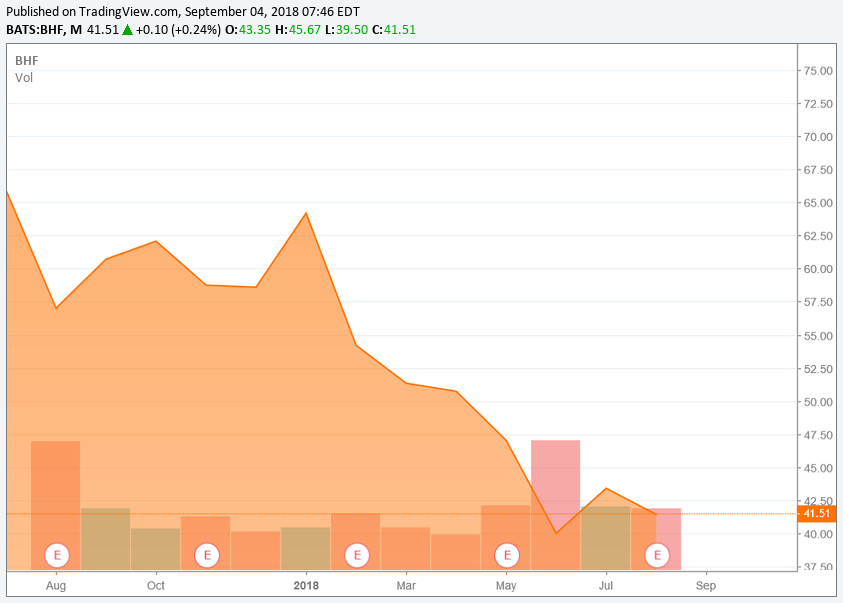

The company is a life insurer and a spin-off from MetLife (MET). It has been public for just over a year and has not done well, as its earnings have been wonky and full of adjustments, its book value hasn’t appeared to stabilize, and the company has not been returning capital to shareholders yet, a recently announced share buyback program aside.

![]()

Snoopy did not come with the spin.

David Einhorn of Greenlight Capital (GLRE) has detailed the firm’s thesis a couple of times. Essentially, it is a classic spin-off situation in his/their view – the presentation as the company prepared to go public via the spin was unenthusiastic, dampening market sentiment, Brighthouse is much smaller than MET, leading to a mismatched shareholder base, and the company’s plan of building up capital for 2-3 years before retruning capital to shareholders means the company doesn’t fit in traditional insurance investors’ portfolios.

We have published a few compelling articles on either side of the trade. To wit, our four most recent articles, in reverse chronological order:

The Ranjit Thomas article attracted pushback from Einhorn himself in a comment, which is what raised this to our attention. Mike and I have been spending a lot of time recently on growth names like Shopify (SHOP) or Alibaba (BABA), sections of the market that we are less comfortable with, to say the least.

So, we felt we were due to come back home to a value stock to see how the story stacks up. But there’s nothing easy about analyzing Brighthouse Financial.

Topics covered:

- 2:30 – Starting off – what does BHF do?

- 6:45 – The spin-off angle and the bull case for BHF

- 15:00 – Spelling out the bear case on BHF’s and whether its model works

- 20:00 – Getting into the books for BHF

- 27:00 – The value of hedging your book at a insurance company

- 31:00 – Reviewing Einhorn’s source idea and the underlying incentives in this story.

- 38:00 – Reaching conclusions and whether it’s better to get into the weeds or avoid them.

We hope you enjoy the podcast. If you have a chance, subscribe on iTunes and rate us or leave us a review – we will make the podcast better based on your feedback. We’re also available on SoundCloud, Google Play, and Stitcher. If you have any favorite articles you want covered, guests you want to join Behind the Idea, or any feedback about our podcasts, send Daniel or Mike a direct message or comment below. You can also now follow this account to get alerts on new Behind the Idea posts. For all my bluster about value stocks above, we’re going to be reviewing BABA again next week with a couple special guests, so stay tuned.

How do you wrap your head around a balance sheet or business model like BHF’s? Do you agree with Mike’s contention that it’s better to stay out of the weeds and to just take a probabilistic view of the market direction? Does this much debate lead you to dig in further or stay away? Let us know below.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: Neither Mike nor I have any positions in any stocks discussed.

Be the first to comment