For a while now, I wanted to write about Whitbread (OTCPK:WTBCF) and Costa Coffee since, in April this year, the firm announced to spin off its coffee chain by 2020. With Coca-Cola’s (KO) announcement to buy Costa, Whitbread management definitely overachieved in terms of sticking to its time frame.

I liked the idea of Costa as an independent business, and I don’t think Coca-Cola made a bad purchase, just one that definitely surprised me.

Below, I’ll give a quick summary about Costa because I can imagine, many US-investors are not familiar with what Coca-Cola is buying here.

Strange business combination

Costa’s current owner Whitbread sees itself as the UK’s leading hospitality provider. The group has a rather interesting combination of businesses: coffee chain Costa on the one hand and the hotel chain Premier Inn on the other.

Investors have long called for a break up of the current structure and to separate them into two businesses. In April this year, Whitbread gave in and announced to demerge Costa within the next 24 months.

While it would definitely be worth to write an article about how the future business of Whitbread could look like, this article will focus on what this coffee chain that Coca-Cola has bought is actually all about.

Costa is incredibly strong in the UK…

Costa Coffee founded in 1971 (coincidentally the same year as Starbucks (SBUX)) and has been part of the Whitbread group since 1995 and considers itself to be the UK’s favorite coffee shop brand and the customers seem to confirm this:

Whitbread Annual Report 2017

While Starbucks might have the US market strongly in its grip, things seem a bit different in the UK. In the UK, Costa has seen a meteoric rise in popularity over the last few years at the expense of Starbucks.

In 2011/2012, Starbucks experienced a major media backlash about them funneling royalties through the Netherlands to reduce its tax bill in Britain, with the end result that Starbucks promised to pay corporation tax in the future, even though Starbucks was never profitable in Britain and still carries forward tax losses, the public turned away from Starbucks. From personal experience working in London, it seemed that Starbucks is kept alive by expats, mainly in London and other major cities. Move just 20km away from London to smaller towns like Harpenden or St. Albans and Costa is dominating!

Additionally, Costa has undoubtedly the better food menu and unlike the “standard” food choices Starbucks offered, Costa, being a UK company, has a way better food menu for the British taste. From sandwiches, wraps to scones & millionaire shortbread, the menu, in my opinion, is better than Starbucks, period!

Costa does not only operate its fully-equipped coffee shops but also Costa Express. These are self-service coffee machines that are set up at supermarkets or small petrol stations, making sure Costa is also available at lower-traffic locations.

{kind=link}

…but only in the UK

While the UK is its core market, the company has a much smaller footprint than its big US-competitor.

Whitbread Annual Report 2017; note that 8,237 Costa Express locations are not included

With around 36% of Costa’s store outside the UK, the international locations account for only 14% of sales for the company, showing the dependency on the UK. Furthermore, Costa is closing its stores in several countries (“non-core”, e.g. France) to focus its activities.

Also, many smaller markets are only served by the Costa Express self-serving machines (e.g. Malaysia), which is another reason for the lower sales figures.

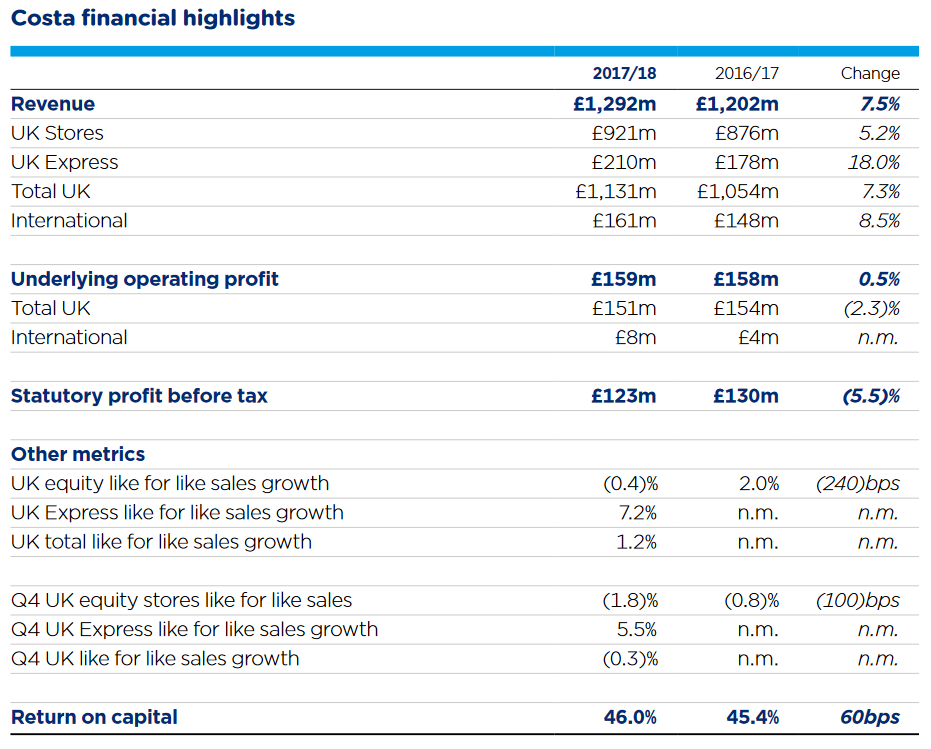

Costa’s dominance in the UK shows in its financial statements

For 2017, Costa reported £159 million adjusted operating profit at a margin of 12.3%.

|

Whitbread Annual Report 2017

To put the sales figure into perspective, Costa’s UK sales are 45% higher than Starbucks’ total EMEA sales, although it has to be considered that for its franchise stores, Starbucks only captures the franchise fees, not the total sales.

While the like for like sales for the full coffee stores have seen a slight decrease, the express service has seen growth in the like for like sales. Additionally, the company has increased its UK store count by about 9% to 2,422 stores and sees even faster growth rates for the express service.

Earlier I mentioned that I preferred Costa’s food menu over that of Starbucks and I don’t seem to be the only one. 40% of the sales in its full coffee stores are food items, significantly more than the 17% for Starbucks.

Whitbread Annual Report 2017

While the increase in store count drives revenue, the end of the runway might be in sight for the UK market, Citigroup predicted a maximum of four to five years of growth left in the UK coffee market.

Costa’s growth strategy seems oddly familiar

With its home market slowly reaching saturation and an already high market share, it seems odd that the company is winding down parts of its international operation.

But the long-term growth plan could be copied & pasted from a Starbucks presentation.

Costa has identified China as its main international growth market, with the company currently having 449 stores there at the moment, aiming for 1,200 by 2022 (according to the Annual Report 2017). This is significantly less than the 6,000 stores Starbucks is targeting for the same time period, but considering Costa’s enterprise value (based on the price paid by Coca-Cola) is only 7% of Starbucks’ market cap, this is still an ambitious target. Noteworthy is that Costa bought out its South China joint venture with Yueda in 2017 for greater control over the stores for a price of £35 million, underlining its commitment to China.

Considering how much Starbucks struggles to bring its EMEA segments to perform to its expectations, Costa might have learned a lesson from them and focusing on the big fish China and serving other markets with its low-investment Express business.

Other than China, Costa notes their new Premium roastery (biggest in Europe) in the UK, new drinks like Nitro Cold Brew, and a focus on ordering through the mobile app as major growth drivers. Again, we have heard most of this before from Starbucks.

The acquisition price is in-line with the market

The quoted price of £3.9 billion doesn’t seem too outrageous to me.

When trying to put that price into perspective, one major issue is that Whitbread does not issue separated cash flow statement for Costa & Premium Inn and the consolidated one is somewhat useless as we have no indication how the cash flows are shared between Costa and the hotel business.

Therefore, I’m relying on the EV/EBITDA ratio of 16.4 provided by Whitbread in the sale announcement.

| Costa | Starbucks | Dunkin’ Brands | |

| Enterprise Value (in million) | £ 3,900 | $ 71,400 | $ 8,704 |

| EBITDA (in million) | £ 238 | $ 5,477 | $ 486 |

| EBITDA Multiple | 16.4 | 13.0 | 17.9 |

| Table by Author, data from Whitbread Annual Report 2017 & GuruFocus | |||

Comparing the multiple paid with Starbucks and Dunkin’ Brands (DNKN), Coca-Cola’s offer seems in-line with the current market valuations, yet personally, an EBITDA multiple of 16.4 still seems a bit on the high side.

Not without risk

Coca-Cola takes a gamble with this acquisition with two major risks that I see:

First is the China wild card. Similar to Starbucks, Costa is betting big on China as a major growth driver and investors are asking the same questions they do with Starbucks. Is China really shifting to coffee long term or is it only a short-term trend? Will the Chinese pay a premium for a coffee from European brands? Only time will tell.

Second issue is the Brexit. With growing concerns whether a deal can actually be made or if there will be an uncontrolled Brexit, buying a UK business that derives 86% of its sales in British pounds is a risk. While a Brexit agreement will most likely push the British pound up, an uncontrolled Brexit will have the opposite effect, eroding the value of the profits earned in US dollar. On top of that, uncertainty during an uncontrolled Brexit might negatively influence sales.

Nevertheless, there is also opportunity if China pays off. Furthermore, Costa does not have a ready-to-drink cold coffee yet, I wouldn’t be surprised if we see that soon, although Costa purposely chose to set up its self-serving stations at supermarkets rather than selling cold drinks.

Lastly, the obvious benefit is it decreases Coca-Cola’s dependence on declining Soda sales.

Conclusion

Costa Coffee is a strong business with a solid position in its home market and the price seems somewhat in-line with market values, yet not a bargain.

Costa will need significant capital investments if it wants to achieve its China store count targets, yet the likely slowdown in UK store openings will ease cash flow requirements.

I am happy to see Coca-Cola diversify, although Costa’s current profit won’t meaningfully move the needle for them, and I don’t see too many synergies between the two. I can’t imagine Costa offering Soda anytime soon (maybe switch water & milk to KO brands), maybe Coca-Cola can push some Costa branded items through its distribution channel, but that will basically be it.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment