The opening lines of Farfetch’s (FTCH) recently-filed F-1 IPO document begins with a bold statement: “Farfetch exists for the love of fashion.” The London-based e-commerce operator, which this year celebrated its tenth anniversary since its founding in January 2008, has filed to go public on the New York Stock Exchange.

E-commerce and consumer-focused startups have been bubbling on both the public and private markets for many years. There’s an e-commerce startup for just about every product niche – mattresses (Casper), eyewear (Warby Parker), pants (Bonobos), and many other less well-known companies. Then there are also horizontal e-commerce companies that span many different categories, but serve up their offerings in a novel manner – the best example here is Stitch Fix (SFIX), Katrina Lake’s subscription box company that sends customers a “Fix” of five items from which they can choose to keep all or none of the items. Stitch Fix faced resistance from the markets early on in its IPO, with most commentators believing the company to be a short-term fad – but in recent months, Stitch Fix shares have jumped to more than 2x their original IPO price.

Needless to say, there is still plenty of appetite in the markets for consumer startups. Farfetch, in particular, offers a very interesting niche in the luxury end of the fashion and apparel e-commerce space. This is an important distinction: while many “ordinary” brands and retailers have embraced e-commerce as an important sales channel, higher-end brands have largely been resistant to straying away from in-store retail channels. According to Farfetch, only 9% of all luxury sales are conducted online. With the younger generation of millennials now beginning to enter their prime earning years, however, even the hardiest of the luxury brands are beginning to change their marketing strategies and starting to pay attention to digital.

This is where Farfetch comes in. In its F-1 registration document, the company writes:

“The global luxury market is evolving, driven by an accelerating shift of consumers to online discovery and purchase, the increasing importance of Millennials and the growth of luxury consumption in China and other emerging markets. We connect a global consumer base to the highly fragmented supply of luxury fashion, and we have established ourselves as the innovation partner to the luxury industry.”

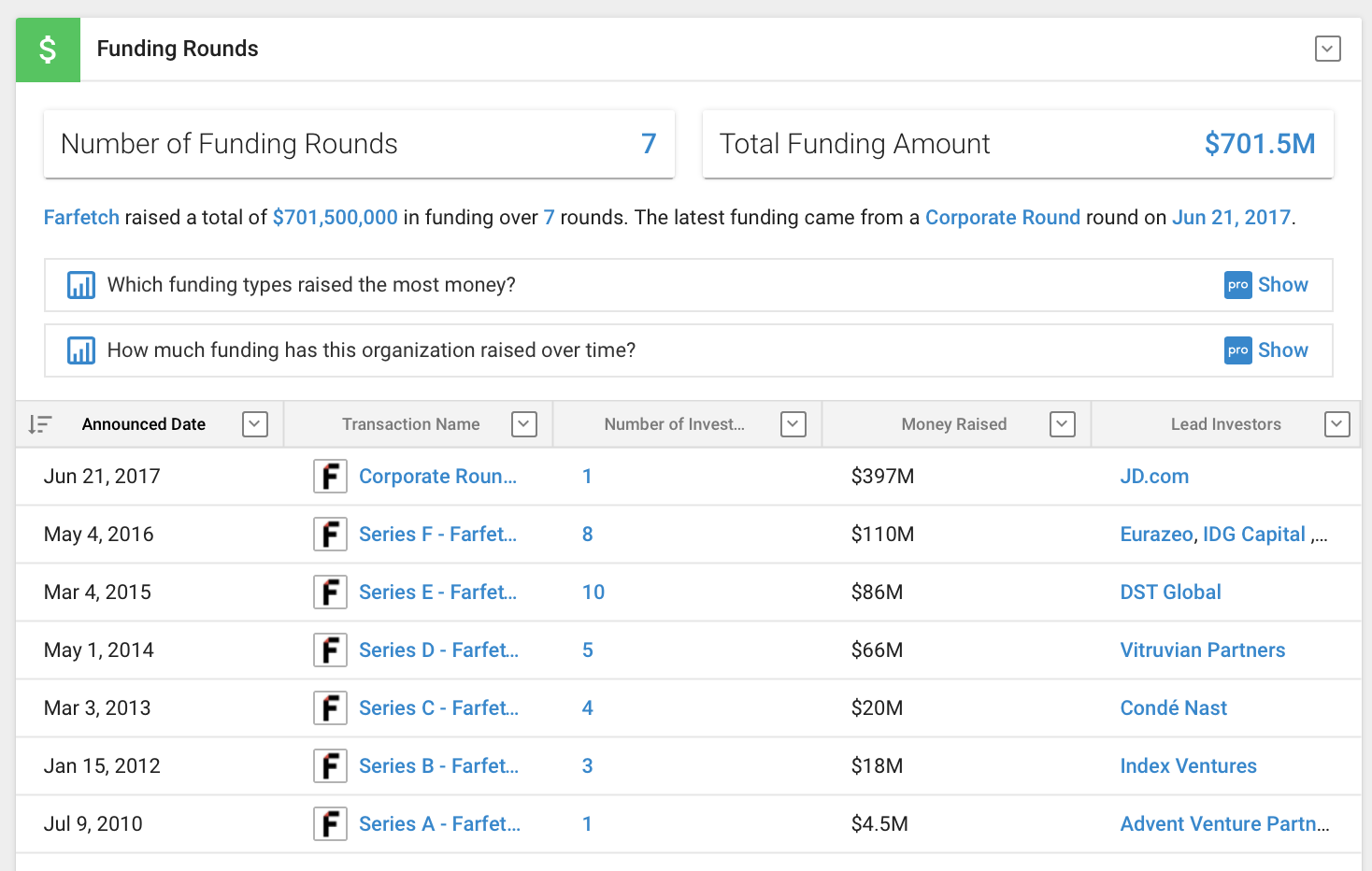

According to Crunchbase, plenty of investors have already stepped up to finance Farfetch in the private markets. A cumulative ~$700 million in funding has been raised in the ten years that Farfetch has been around, including an equity investment from JD.com (NASDAQ:JD), the Chinese e-commerce giant:

Figure 1. Farfetch funding timeline

{kind=link}

Source: Crunchbase

Given the large amount of funding that has been raised to date, Farfetch is almost certainly above a unicorn valuation. Its Series F round was completed at $1.6 billion valuation, but recent observers have predicted that Farfetch may nab a $5 billion valuation in this IPO.

The final pricing for this IPO is still TBD, so it’s difficult to render a positive or negative opinion on this IPO at this point in time. However, there’s a lot of information we can glean now from the company’s filings to get ready for the upcoming IPO:

The premier e-commerce platform for high fashion

While many e-commerce companies exist to serve the fashion and apparel industry, including websites and channels owned by brands themselves, Farfetch aims to be the defining platform for all things luxury.

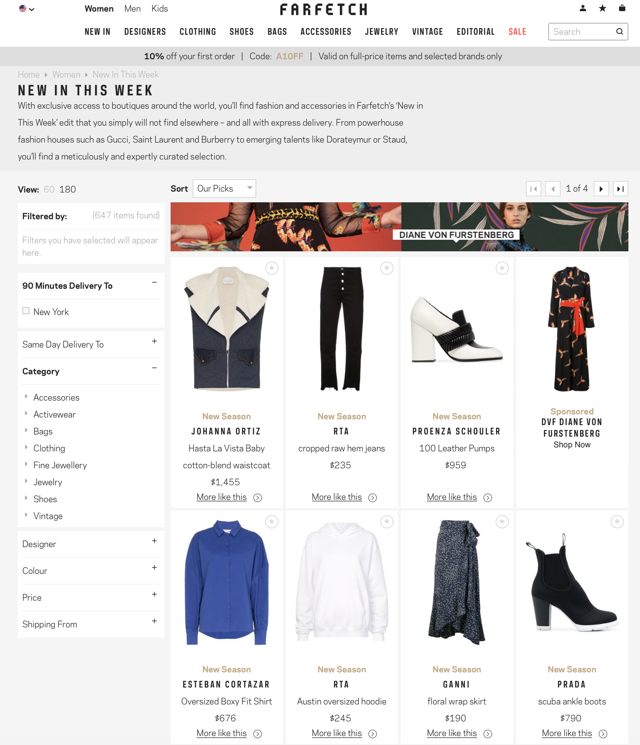

A snapshot of the company’s website, featuring “Top Picks” in the women’s department, is shown below. Brands represented on Farfetch’s platform include well-known names such as Gucci and Prada, but also extend to more niche high-end designers and labels.

Source: Farfetch.com

Farfetch primarily operates a marketplace model – as in, it’s merely a marketing channel for luxury sellers that takes no possession of inventory. Fulfillment is generally executed by the luxury sellers, though packaging includes a Farfetch label. In return, Farfetch takes a percentage of sales, which it calls the “Third-Party Take Rate”. The company has built relationships with nearly 1,000 luxury sellers – 614 of which are retailers, and 375 of which are luxury brands.

On the consumer end, Farfetch is available to customers in over 190 countries, and as of the end of June 2018, Farfetch had 1.12 million active customers (defined as a customer that had placed an order any time within the past twelve months), up 40% y/y. Over half of Farfetch’s customers are millennials, and the customer base skews female with an average age of 36 and an average annual income of $121,500. In addition, just under $1 billion of GMV was conducted on the Farfetch platform last year.

Farfetch’s partnership with JD.com is also an interesting aspect to note. The relationship goes far beyond an equity injection from the Chinese giant – Farfetch also notes in its F-1 that it “leverages JD.com’s local logistics network, consumer payment solutions, technology capabilities, and its marketing resources, including its WeChat partnership.”

China is an incredibly important market for any company – not just for the sheer population count but also due to a rising upper-middle class that has demonstrated a keen taste for luxury goods. The famed consulting firm McKinsey & Co. put out a report about how Chinese shoppers have begun to dominate the luxury scene, far more so than their U.S. counterparts. A China strategy critical for luxury brands, and in JD.com, Farfetch has a direct link to Chinese consumers.

In addition to operating its e-commerce channel, which provides more than 80% of the company’s overall revenues, Farfetch acquired a London-based retailer called Brown’s in 2015. Brown’s consists of two in-store retail locations in London, and Farfetch asserts that having ownership of a retailer, despite contributing just $15.4 million (4%) of revenues in FY17, helps the company to “understand the luxury fashion ecosystem through the lens of a boutique.”

Figure 2. Farfetch revenue mix

Source: Farfetch F-1 filing

Financial overview

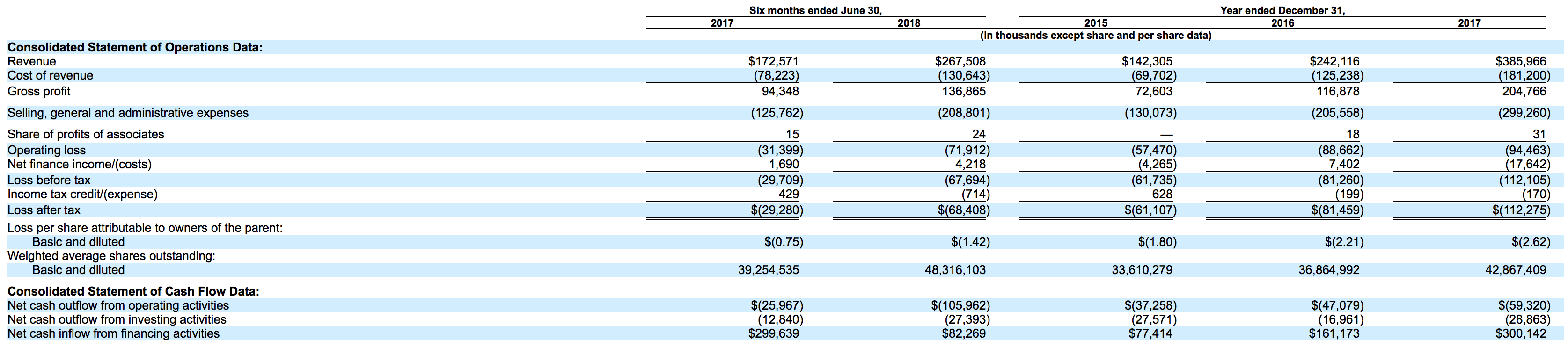

Here’s a look at Farfetch’s financials for the past three years and first half of 2018:

Figure 3. Farfetch historical results

Source: Farfetch F-1 filing

Revenues in FY17 grew 60% y/y to $386.0 million. That growth rate has largely carried over into the first half of 2018, with revenues growing 55% y/y to $267.5 million.

For the most part, revenue growth hinges on Farfetch’s ability to expand its GMV. For the last several years, Farfetch’s Third-Party Take Rate has hovered between 31-33%, even falling 200 bps to 31.7% in the first half of 2018 relative to the first half of 2017. A 61% y/y growth rate in GMV, however, has been able to make up for the drop in commissions:

Figure 4. Farfetch GMV and take rate

Source: Farfetch F-1 filing

Consistent with Farfetch operating a fee-based marketplace platform (with the exception of the small portion of retail revenues generated by Brown’s, as previously discussed), its overall gross margin is high – at least, compared to the typical e-tailer that carries inventory. Farfetch generated a gross margin of 51.1% in the first half of FY18, 360 bps worse than 54.7% in the year-ago quarter, with the drop being primarily attributed to the lower Take Rate in order to attract more brands and grow GMV. Investors will be closely watching the gross margin trend at Farfetch, as with any other e-commerce company.

The company’s heavy investments in sales and marketing, however, have pushed the company into fairly sizable losses. Demand generation activities have picked up as the company enters into new countries and markets. As a result, operating losses nearly doubled in the first half of 2018 to -$71.9 million, representing an operating margin of -26.9%, substantially worse than -18.2% in 1H17.

Operating cash burn in the first half of the year also jumped up to -$106 million. With $337 million in cash and impending proceeds from this IPO, however, Farfetch still has enough liquidity to finance several years of losses.

Key takeaways

The big variable remaining in Farfetch’s IPO is its valuation. If the company manages to achieve the $5 billion valuation that many observers are expecting, it will be a tremendously expensive IPO to invest in. At a 55% y/y growth rate for this year, Farfetch will hit just under $600 million in revenues this year – positioning Farfetch for a ~8.4x revenue multiple at a $5 billion valuation. Though Farfetch’s high growth is appealing, its large level of losses – as well as a decline in its take rate, and the threat of GMV deceleration – should induce caution in investors at excessive valuations. And though Farfetch has maintained a near-100% retention rate with its top brands thus far, there’s nothing preventing luxury brands from peeling off the Farfetch platform and utilizing their own stores instead to avoid paying the ~30% commission to Farfetch.

That being said, however, Farfetch will be an exciting IPO to watch, given its advantage in the luxury market and fast-growing appeal with high-income shoppers. It’s entirely possible for Farfetch to replicate Stitch Fix’s returns and double in a short amount of time, but only if Farfetch opens low enough to allow investors some upside. More to come as the IPO draws nearer and more details become known.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Editor’s Note: This article covers one or more stocks trading at less than $1 per share and/or with less than a $100 million market cap. Please be aware of the risks associated with these stocks.

Be the first to comment