After the bell on Monday, online commerce giant Mercadolibre (MELI) announced a large convertible bond offering. As the company has racked up losses this year leading to reduced cash flow, and a previous bond offering comes due in less than a year, capital was certainly needed. It will be interesting to see what the company pays on this deal, given how its recent results have been plagued by a very strong US dollar.

The company is offering $800 million in 10-year convertible notes, with underwriters being given an option to purchase another $120 million. A lot of the terms seem fairly standard, which can be fully read in the link above. As is usually the case, the company will enter capped call transactions to limit the amount of potential dilution from these notes.

If we look at the most recent 10-Q filing, you’ll notice that the company has 5-year convertible notes coming due in 2019. A very small number of holders have converted, but this roughly $330 million in debt is now due in less than a year. Part of the reason from the new offering was to repay a portion of this debt off, but the question is what will the overall cost be?

When Mercadolibre issued the 5-year 2.25% notes back in 2014, the 5-year US Treasury note was about 95 basis points lower than it is today. The 10-year US Treasury, perhaps more comparable given the maturity on the new offering, was about 15 basis points lower. I expect to see a higher rate this time around, especially given the offering size is more than twice the previous one. In fact, the company’s entire balance sheet only had a little more than $1.5 billion in total assets at the end of the most recent period, so this note offering is rather large, even though some of it is to repay current debt.

If I had to guess currently, I would say somewhere in the 3.00% to 4.00% annual interest rate would be fair for this offering, as we look to compare it to the previous one. It is a lot larger and has a longer maturity, plus US rates have risen since. Anything less than 3% should be considered a win, but if we are way above 4% then I will start to worry about interest expenses really impacting the bottom line, especially if underwriters exercise their option.

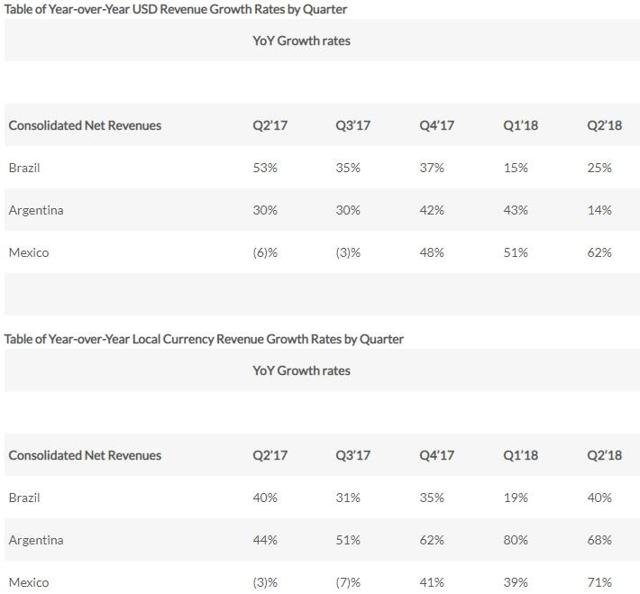

Shares of the company rallied to nearly $395 a share after the Q2 earnings report a couple of weeks ago, but they’ve come way down since, closing under $320 on Monday. Part of the reason has to do with the stronger dollar, which I warned investors about previously. The graphic below shows just how much the dollar’s rise hurt the company’s announced growth rates.

(Source: Q2 earnings report, seen here)

Given problems in countries like Turkey and Argentina are on the rise, plus the weakening of the Chinese Yuan, the dollar has risen against the currencies of the three countries noted above even further in Q3. That is going to add even more pressure to the company’s results, especially in the two largest markets, Brazil and Argentina, where the dollar is strongest.

When we look at Q2, a lot of trends were similar to Q1. Revenue growth was impacted significantly by the stronger dollar, and extra expenses meant the company shifted from a profit to a loss, this time about $28 million. With losses in both quarters this year, operating cash flow in the first six months was just $107 million, down from $226 million in the prior year period. Free cash flow was even worse than that picture given a roughly $16 million rise in capital expenditures.

In the end, we have approached the point where Mercadolibre is hitting the markets for fresh capital. Debt is coming due next year, and the balance sheet could use some help anyway. With a stronger dollar significantly hurting revenue growth and high spending combining to push the company into quarterly loss territory, it will be interesting to see what the coupon is once this deal closes. What do you think it will be? I look forward to your responses below.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: Investors are always reminded that before making any investment, you should do your own proper due diligence on any name directly or indirectly mentioned in this article. Investors should also consider seeking advice from a broker or financial adviser before making any investment decisions. Any material in this article should be considered general information, and not relied on as a formal investment recommendation.

Be the first to comment