General Electric (GE) is getting dangerously close to closing at new yearly lows. Potential asset sales for the power conversion unit and digital business are doing nothing to get market participants buying the stock again. Needless to say, GE’s run back to $15 in May did not last. What will it take for the stock to stop making fresh 52-week lows?

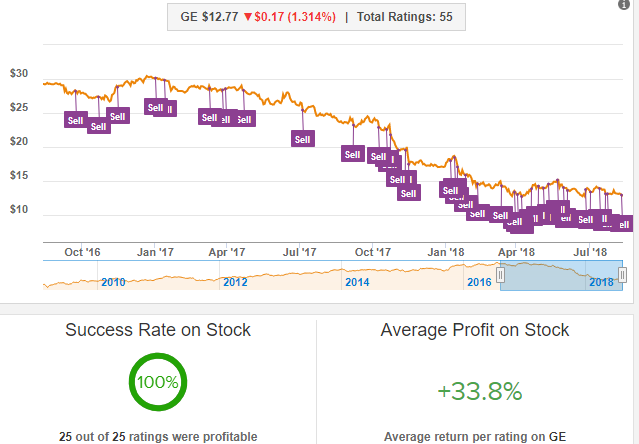

JPMorgan’s (JPM) Stephen Tusa resumed the bearish calls against GE last week by calling the stock a sell. Tusa’s perfect success rate and 33.8 percent average return on GE will only get better if the stock does meet the analyst’s $11 price target:

Source: Tipranks

Rumors of GE selling the power conversion unit only supports the negative calls against the conglomerate. GE paid $3.2 billion for the asset in 2011 but may settle for less than half of that, at $1.5 billion. For shareholders, whether GE sells the unit at a loss or keeps it will have little impact on the stock price. The overpayment reflects management’s poor leadership and capital allocation over the last seven years.

If investors had a choice, they would want GE to sell the unit. In FY 2017, the unit dragged results lower as GE took “significant charges at Capital and Power Conversion.” Removing the distraction allows current management to focus on two stronger units: Aviation and Medical.

Digital Business for Sale

On July 30, rumors, as reported by Wall Street Journal, circulated that GE would sell the digital unit. In 2017, revenue grew 12 percent Y/Y to $4 billion but new orders fell an unacceptable 23 percent. In an age where digital is growing in the double or triple digits, GE is better off selling the unit. It can no longer afford to spend billions to prop up the unit. As part of the asset sale, GE could secure support from the digital unit for the aviation, power, and medical units.

Digital is made up of four key units:

PredixAsset Performance Management (APM) software ServiceMax, a field service solution Manufacturing Execution Systems (“MES”) software

IoT has potential growth. Many firms are pivoting into this field. BlackBerry (BB), for example, is targeting the IoT market as it sells secure software solutions. Nokia (NOK) is betting that 5G, whose speed is critical for IoT, will drive the network upgrade cycle. In the semiconductor space, Intel (INTC) and Qualcomm (QCOM) are developing chip solutions through Atom Automotive and Snapdragon Automotive, respectively. It stands to reason that if these fast-growing chip giants are developing IoT solutions, then GE’s digital unit and its play in IoT should attract bidders.

Weak Quarterly Results Raise Warning Flags

GE’s second-quarter results reminded investors of the headwinds ahead. The company also forecast third-quarter EPS on the low-end of the $1.00 – $1.07 guidance. FCF for the year will be at the $6 billion range, at the low-end of the previous $6 billion – $7 billion forecast. On its conference call, GE flagged the challenges in turning around its Power business, as order softness put pressure on cash flow and working capital. The good news was that Aviation and Healthcare both performed well, as did Oil and Gas. FCF was $258 million, with cash at $1 billion better than last year for the first half of the year.

For the full-year, FCF will top $6 billion. GE ended the quarter with $8.9 billion (excluding Baker Hughes), down $2.9 billion from last year. It used $1.4 billion in adjusted industrial free cash flow and distributed $2.1 billion to shareholders through its quarterly dividend. GE expects to end the year with over $15 billion in cash.

Valuation

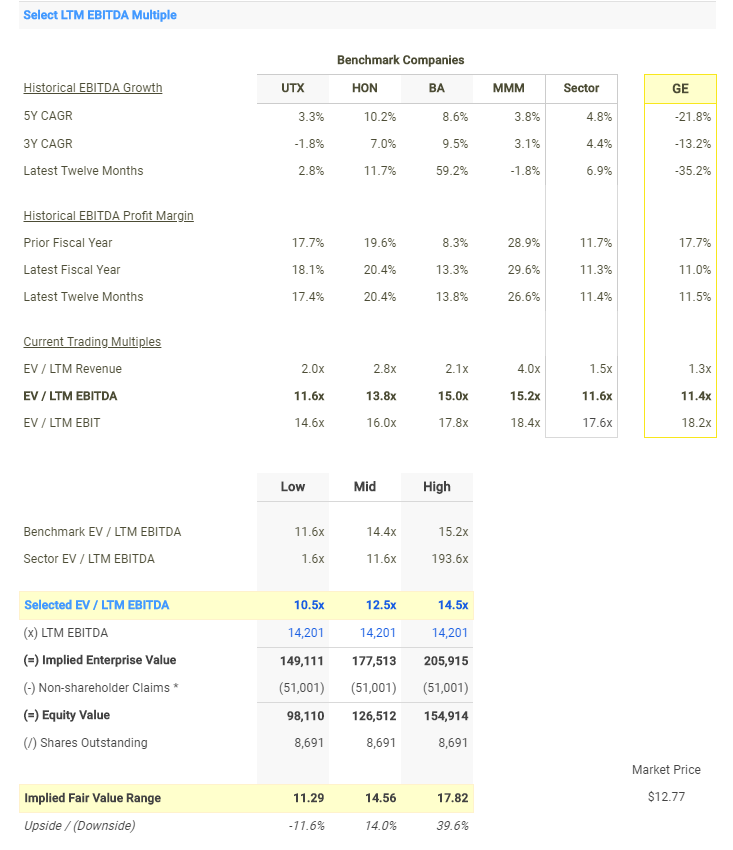

Analysts have an average price target of $15.32, implying upside of 20 percent. This is the price target I previously set for GE stock. Similarly, an LTM EBITDA Multiple that compares GE to that of Honeywell (HON), Boeing (BA), 3M (MMM), and United Technologies (UTX) would imply a fair value of around $15 for GE:

Source: finbox.io (click on the link to crunch your own numbers in the model)

GE is the only conglomerate that is down in the double-digits in the last year:

GE data by YCharts

GE data by YCharts

Takeaway

Pricing pressure in Power will continue to hurt GE’s results, so selling the unit is the best thing to do. As market conditions worsen, GE will face pressure on orders. It already modeled cost cuts to operations in its forecast. Although management expects pricing pressure for equipment, services revenue should be stable.

The short-term downside on GE stock is clear: as macro uncertainties increase, the stock will close at new lows. Eventually, the stock will bottom, as asset sales and the potential plan of splitting the company in two units – Aviation and Medical – unlocks shareholder value.

Please [+]Follow me for value stocks on sale. Click on the big “follow” button beside my avatar.

Want more? Join the Do-it-Yourself Value Investing marketplace service. Get hands-on support from a community of members seeking discounted stocks.

Disclosure: I am/we are long NOK.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment