Sometimes we get a reminder of how vast the world is around us, and the far reaches that business can find in this world. Of all the possible businesses and multi-billion dollar companies out there, one of the least thought of may be ABM Industries Incorporated (ABM). With so many companies out there, ABM Industries has made billions of dollars doing all of the “little things” for other companies. What do I mean? Let’s explore the business behind this dividend champion with our next spotlight feature.

source: ABM Industries Incorporated

“Little Things” That Add Up To Big Business

ABM Industries has built a business empire by performing all of the “little things” (as I call them) for other business. These facility management services are what keep other businesses running from a literal standpoint.

source: ABM Industries Incorporated

source: ABM Industries Incorporated

The core of ABM Industries is performing the logistics and services that keep actual buildings running properly. Janitorial services, Parking, HVAC, Landscaping, and more. ABM Industries performs the basic logistical upkeep of corporate buildings/facilities so that its clients can pour their resources and labor into revenue generating avenues.

source: ABM Industries Incorporated

source: ABM Industries Incorporated

The range of customers that ABM Industries has put together ranges from small to large companies, sports franchises, and some of the largest corporations in the world, spread across a vast array of industries.

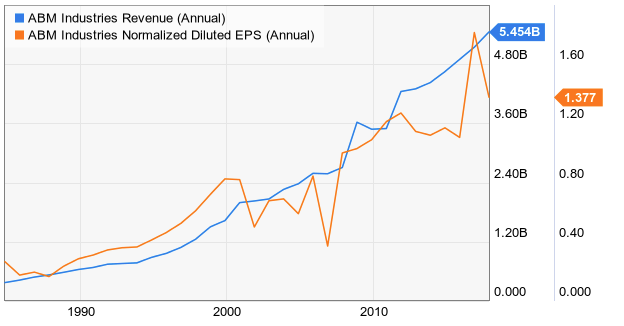

This variety of services has added up to some big business over the years. Both revenues and earnings have consistently tracked higher over the years, and significant top line growth has taken place in the last decade as revenues moved from just over $3.5B to almost $5.5B just in the last decade.

source: Ycharts

source: Ycharts

This consistency has resulted in an impressive dividend track record. The dividend has been raised a staggering 51 consecutive years. If you thought the list of “dividend champions” was exclusive (only 123 out of several thousands of traded stocks), the unwritten circle of “dividend aristocrats”, or “dividend kings” – those with 50 year streaks or higher, is even smaller!

A Closer Look At Things

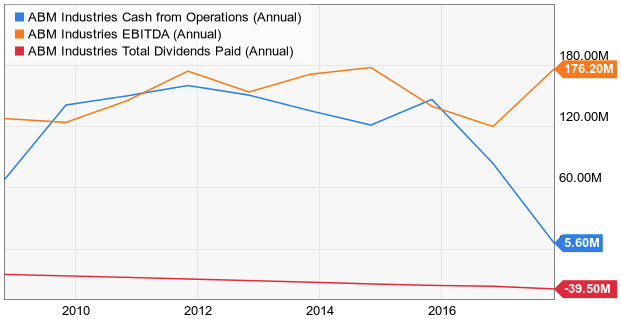

Now if we take a closer look at the business, some interesting data points start to stand out. This dividend – though raised like clockwork every year, isn’t growing very much. In fact, over the past decade, the dividend CAGR is 3.5%. That is only a touch higher than the long term average inflation rate in the US of 3.22%. This is disappointing, because as an investor I want my “purchasing power” to increase over time. When the dividend growth isn’t outpacing inflation, that is a lost tool of wealth building from the investor tool box. You want your dividend to outpace inflation so that your “purchasing power” further compounds as you reinvest those dividends. The good news is that ABM Industries can afford the dividend. The annual payout of $0.70 per share is typically a bit less than both earnings and cash generated from operations.

source: Ycharts

source: Ycharts

When you poke around the financials a bit though, the picture starts to become a little bit more clear. ABM Industries operates at a very low margin point. Its EBITDA margin has been 4.3%, and will just clear 5% in 2018.

It shows up when you look at a company that does almost $5.5B in revenues, yet only yields a tiny amount of that in cash flows. They did more than $5B in 2016, and still couldn’t clear $100M in cash flows. This is troublesome because I find that typically, “cash cow” type companies are the best long term investments. This is because companies with strong cash generation can not only use that cash for straight forward payouts such as dividends and share buybacks, but also by organically reinvesting funds back into the company to drive growth. I typically look for companies that convert at least 10% of their top line into free cash flows, and ABM Industries isn’t even close to that. It’s more like in the low single digits on a year to year basis.

It shows up when you look at a company that does almost $5.5B in revenues, yet only yields a tiny amount of that in cash flows. They did more than $5B in 2016, and still couldn’t clear $100M in cash flows. This is troublesome because I find that typically, “cash cow” type companies are the best long term investments. This is because companies with strong cash generation can not only use that cash for straight forward payouts such as dividends and share buybacks, but also by organically reinvesting funds back into the company to drive growth. I typically look for companies that convert at least 10% of their top line into free cash flows, and ABM Industries isn’t even close to that. It’s more like in the low single digits on a year to year basis.

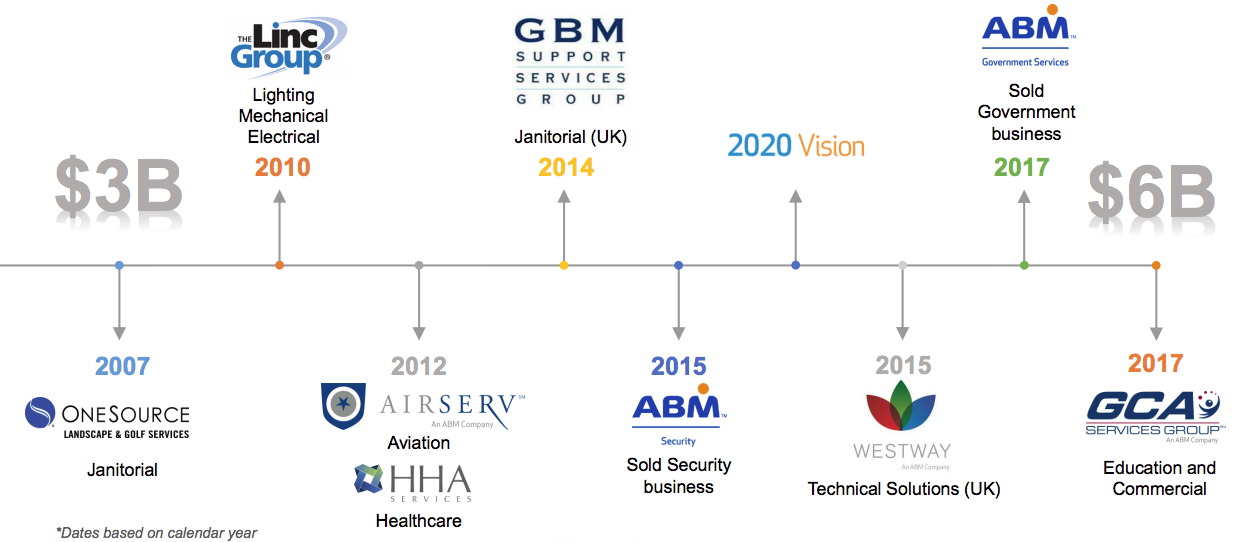

Because cash flow generation is limited for ABM Industries, it has turned to acquisitions to increase the size of its business over the years.

source: ABM Industries Incorporated

source: ABM Industries Incorporated

In doing so, there are some additional risks that ABM Industries may face. Now I must admit that ABM Industries is neither the first, nor the last company that we will look at who happens to heavily utilize a M&A growth strategy. But there have to be building blocks of success in place for the strategy to work over the long haul.

First, the acquisitions have to add value to the business. Now obviously the increase in revenues is a good thing. But has the company gotten any more profitable or efficient from these various deals?

source: Ycharts

source: Ycharts

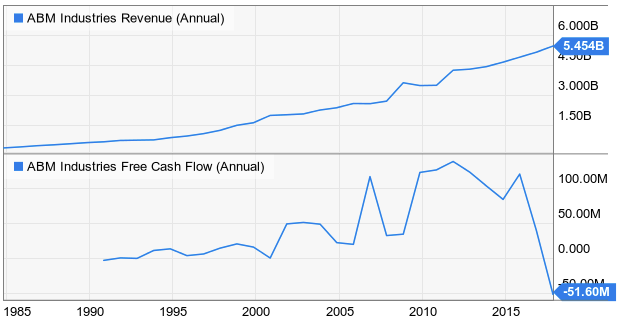

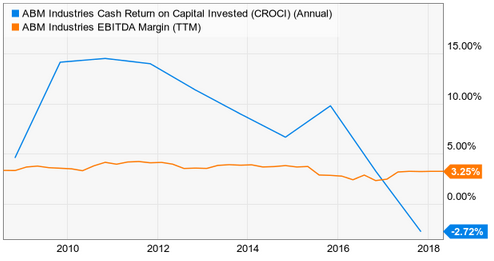

Over the past decade while revenue has grown from $3B to almost $6B, EBITDA margin (this graph is straight up EBITDA margin while the earlier figure provided by ABM Industries was an adjusted figure) has slightly eroded over the time frame. At the same time, the company has drastically lowered its cash return on invested capital. The company would appear to actually be worse off at generating cash flows, than when it was a smaller, leaner company.

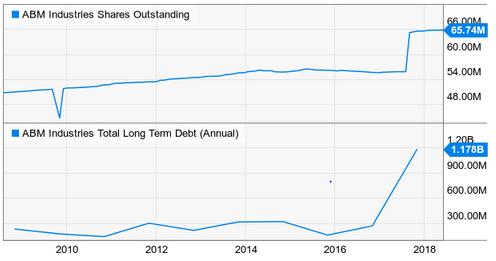

The second criteria of doing a lot of M&A, is that the company have an adequate means of funding these deals. Because ABM Industries isn’t very strong at cash flow generation, it has had to rely on other means to fund these acquisitions.

source: Ycharts

source: Ycharts

Over the last decade, both debt and shares outstanding have gone higher. This means that not only is the company more leveraged than it was, but shareholder value has been diluted along the way as the company increases the size of its share float.

A 2020 Vision

Management is aware that something needs to be done to increase profitability. The company is very labor intensive – it employs a lot of people to do field work, which carries costs in the form of wages, and insurance. These costs can become very detrimental in a short period of time as insurance costs keep rising, and a hot economy means higher wages as companies compete for high quality labor. When you throw in rising interest rates producing interest expense, it all of a sudden makes sense that the dividend doesn’t grow much. The limited cash flow generation leaves little “wiggle room”.

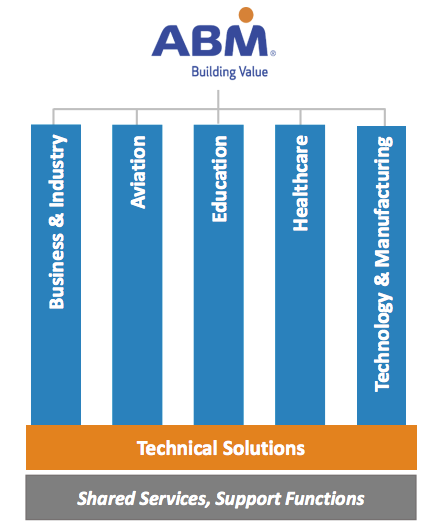

That is why ABM launched its “2020 Vision” back in 2015. With all of these acquisitions, it was a good opportunity for the company to assess itself, and address some of these profitability issues that partially stemmed from a company structure that was disorganized, and inefficient. It reorganized its reporting structure in 2018 into six cohesive segments.

source: ABM Industries Incorporated

source: ABM Industries Incorporated

The company started to mesh and share resources between business segments to increase efficiency, centralized its procurement practices, and invested into cloud based technology to upgrade key technical assets such as its CRM program (Customer Relationship Manager for those who are curious about the acronym).

source: ABM Industrial Incorporated

source: ABM Industrial Incorporated

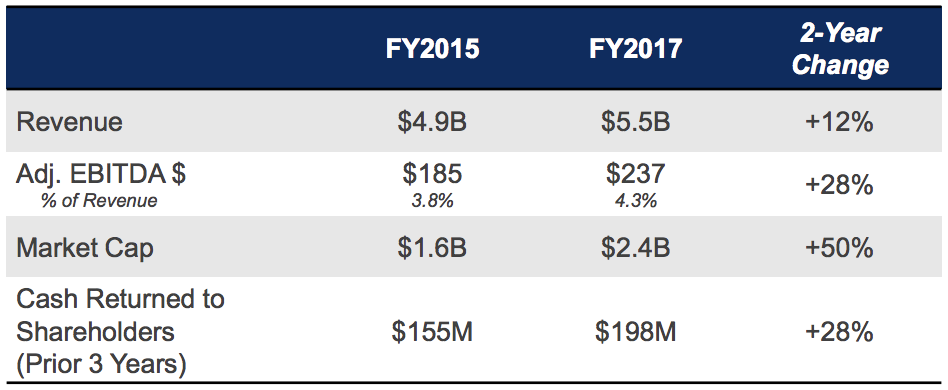

While these improvements will surely help the company run better, the underlying margin problem has yet to drastically improve. The adjusted EBITDA margin has moved up to 4.3%, but target levels were 4.8% at that point when management reviewed these results. Adjusted EBITDA margin is projected to rise to just over 5% in 2018, but it doesn’t seem like enough. This doesn’t give me much confidence that profitability will drastically change for the better. Pricing for many of ABM’s customers are worked out in term contracts so if costs don’t come down to help margins, there isn’t much that ABM can do in the short term.

Valuation

The failure of ABM Industries to grow its margins has been one of the potential sticking points that has hurt shares over the past year.

source: ABM Industries Incorporated

source: ABM Industries Incorporated

Shares have been on a roller coaster of a ride over the past three years. Initial optimism surrounded the ambitions of the 2020 Vision agenda, and then perhaps disappointment at lackluster results followed. The P/E ratio now sits at just under 16X this year’s earnings estimate, which is a pretty sizable discount to the 21X earnings multiple that it has traded at over the past decade. The dividend yields 2.33% on the share price, which is right on target with averages.

source: ABM Industries Incorporated

source: ABM Industries Incorporated

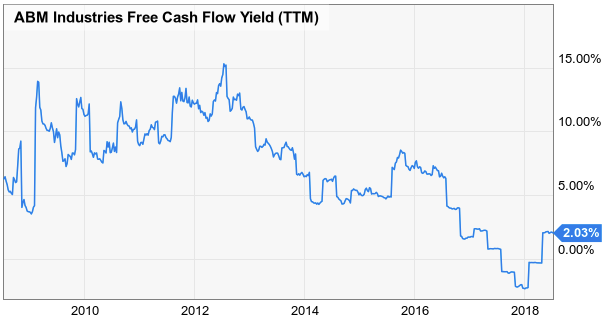

Despite the attractive P/E ratio, I am a bit troubled by the low yield on free cash flow. What this measures is basically “how much cash flow am I getting for my dollar”? Because ABM Industries is not generating much cash flow, the stock needs to trade at a very low valuation to get value out of cash flows. The value in ABM Industries from a cash flow basis has been on the decline since 2012.

source: Ycharts

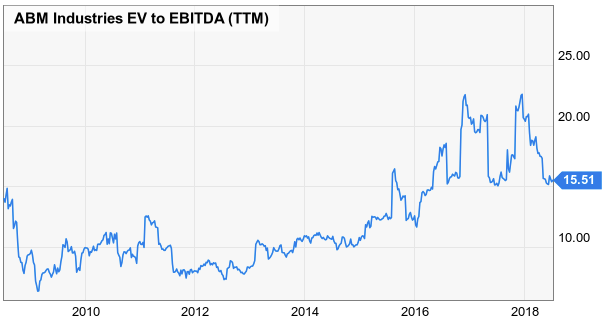

I decided to take a look at some measurements that take into account the actual business assets of ABM Industries. I used Enterprise Value because I wanted to compare the entire value of the company (from the perspective that I was potentially going to buy the company), and compare that figure to its actual earnings power. I typically look for a ratio of 10X or less. As we can see, the last time such a ratio was under 10X, was about three years ago. Essentially the company has grown, but the earnings power of the company hasn’t followed sufficiently. There is a disconnect between perceived value, and actual business performance.

Wrapping Up

If we take all of this information and combine it, what are our conclusions? The ultimate root of ABM Industries’ problems is that the company isn’t profitable enough. The company has tried to grow via acquisition, but the growing top line hasn’t impacted the bottom line enough. The company’s dividend is safe, but the company as a wealth engine is a bit stuck in the mud.

The company seems to be stuck with these low margins, while exposed to a risk of rising labor costs, and insurance costs. Meanwhile, it must be careful about further leveraging itself as rising interest rates and limited cash flow don’t provide a lot of room for interest expenses.

The stock has come way down from its highs, so you could argue that the company is an OK trade when comparing its P/E multiple to historical averages. But investment wise? When you look at how much earnings power and cash flow you are actually getting from shares – it comes up a bit short for me. The company is stable and serves a key area of need for large organizations across the world. As an investor though, I am left asking “where does it go from here”? Cash flow is the “life blood” of a company – and an investment. With ABM Industries unable to produce much, it’s difficult to get excited.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment