The most dangerous diminutions of freedom come from those who are convinced of their moral rectitude.” ― Daniel Hannan

Not exactly the start to the quarter that investors wanted on Monday. The first day of trading in the quarter saw all the major indices slide at least two percent with the Nasdaq falling almost three percent on the first day of the second quarter of 2018. Tuesday brought a late surge of buying into equities, which allowed the indices to cut their losses substantially yesterday.

Trading in February and March was volatile after a good start of the year in January, as investors worried about rising interest rates (which have now ebbed recently) and then concerns about a “trade war.” While the market is selling off on the announcement of $50 billion of new Chinese goods targeted for tariffs as well as potential retaliation from China, nothing has gone into effect as of yet. Our new targets have been put out for “comment” until late May. That gives both parties time to negotiate a “settlement,” which is what happened recently with the revised South Korean trade deal.

As I have been saying for two months now, I am almost exclusively deploying “dry powder” into the market on dips via Buy-Write orders. I believe this is a rock-solid risk mitigation strategy and one I plan to continue to use until the market stabilizes.

There seems to be a “whiff” of panic in the market currently, and watching the Dow move 500 points in a day or more is not fun for anyone. That being said, I do think hope is on the way for investors in the form of first-quarter earnings reports that will start to hit the wires in mass starting in mid-April.

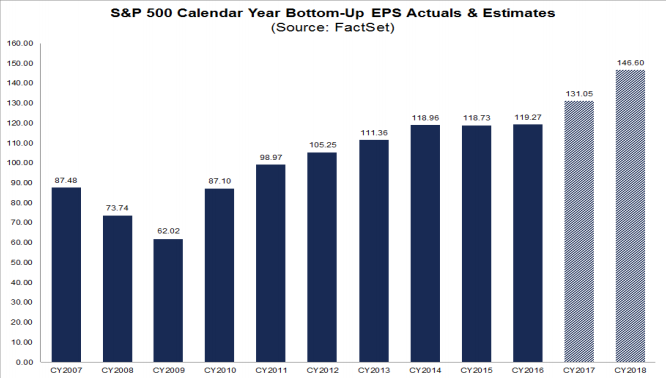

Earnings almost always “step over” the bottom line consensus as analysts are usually “guided” by management to set a “low bar” with earnings expectations throughout the quarter. However, I think this earnings season could see some significant “beats” that should get the market back on track. I have this view for several reasons.

First, despite recent worries about a “trade war,” the global economy is in “sync” for the first time since the financial crisis.

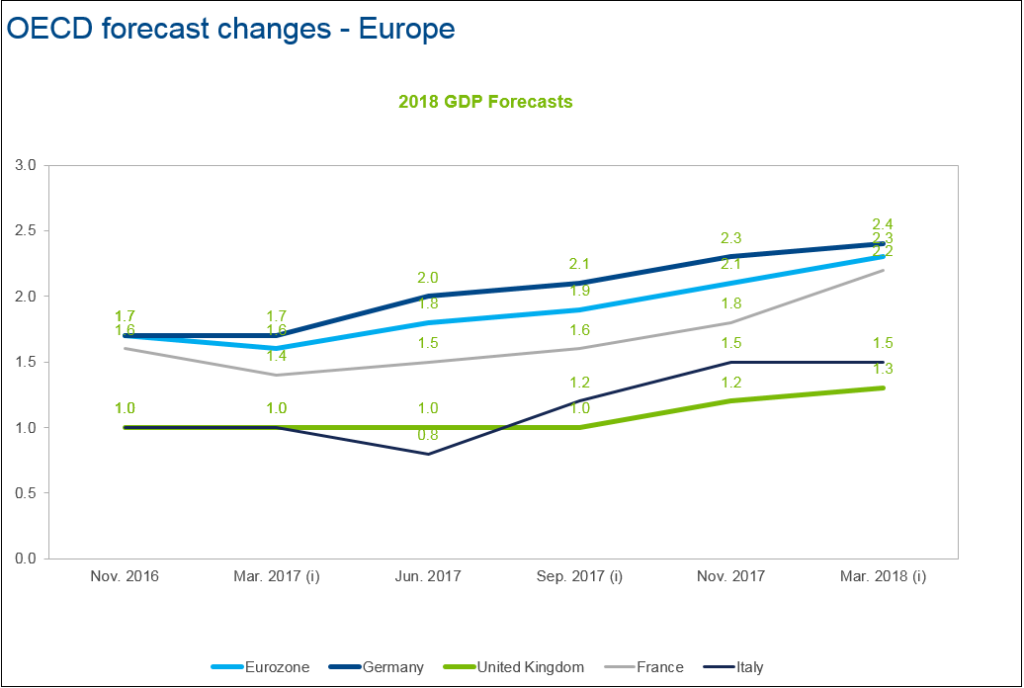

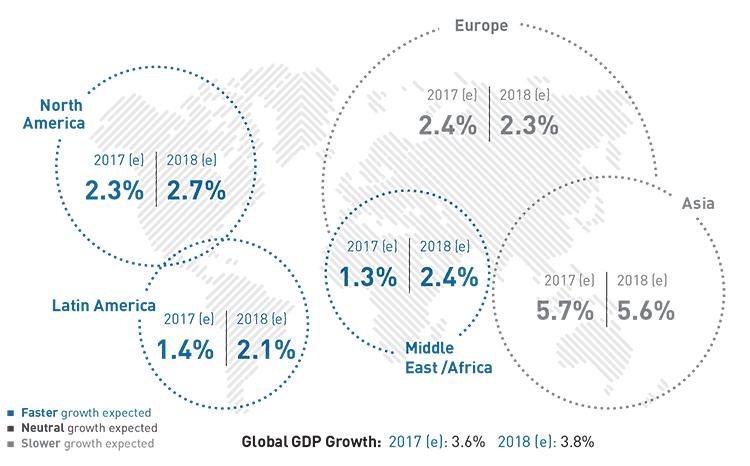

Just under four percent GDP growth is expected from the world economy this year. Even Europe is getting into the act after what has been a “lost decade” for economic growth.

In addition to global growth, the dollar on average has lost ground to major currencies for five straight quarters. This should continue to have a beneficial impact on the profits of American multi-nationals.

Domestic economic growth is also on the upswing. After posting anemic growth of just 1.6% for the full year of 2016, GDP grew 2.3% in 2017. The last three quarters of the year saw roughly three percent growth. With a strong jobs market and the impacts from tax reform, it is quite possible the domestic economy could grow three percent or better for the entire year for the first time since 2005 in 2018.

Finally, the corporate tax cuts are going to start showing up in quarterly profits for the first time this quarter. This will be an especially powerful driver for profitable domestically focused small and mid-cap stocks like home builders and retailers. Before tax reform, $1 of pre-tax domestic income yielded 65 cents in profits. After tax reform, that same pre-tax dollar yields 79 cents, a better-than-20% positive for the bottom line.

I don’t think analysts have fully factored that into earnings estimates for the quarter or the year yet. Just look at the just posted results from Lennar (LEN) this morning. The large home builder posted earnings per share of $1.11. This was more than 30 cents a share above the consensus. Now that is what qualifies as a major “beat” in my book. The company also stated on its conference call that its effective tax rate should drop from 34% in 2017 to 24% in 2018, thanks to tax reform.

I think Lennar’s experience will be repeated many times in coming weeks. Therefore, I think the first-quarter earnings season should be more than solid enough to relieve the anxiety in the market.

The market is trading at roughly 17 times forward earnings, providing an earnings “yield” of ~5.9%. Given the “risk-free” yield of the 10-Year Treasury is currently under 2.8%, the market does not seem expensive once volatility ebbs. This is especially true if the cavalry (in the form of robust first-quarter earnings) are on the way.

He who steals a belt buckle pays with his life; he who steals a state gets to be a feudal lord.” ― Zhuangzi

Author’s note: To get these types of articles and Instablogs as soon as they are published, just click here for my profile. Hit the big orange “Follow” button and choose the real-time alerts option.

Disclosure: I am/we are long LEN.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment