By K C Ma and Lee Briggs

Recently, President Trump said that his administration will levy a 25% tariffs on “about $60 billion” worth of 1,300 Asian (China, Japan, Korea, Taiwan) imported technological goods. Where exactly the 25% levies will fall is still unknown, but the focus will obviously reflect Administration’s concerns about China’s aggressive moves to acquire and obtain new technology in areas such as semiconductors, computing, and manufacturing.

China immediately responded and followed through with its own tariffs on 128 U.S. products, mainly agricultural goods, with an import value of $3 billion. It is not yet known whether the US technology sector will be the next target of further Chinese retaliation. But it is likely with the large orders Chinese manufacturers place with Advanced Micro Devices (NASDAQ:AMD), Nvidia (NASDAQ:NVDA), Qualcomm (NASDAQ:QCOM), and other US chipmakers. However, the China’s choice of the tech “hit list” becomes a delicate one since many U.S. hardware makers rely on Chinese contract manufacturers. Therefore, any technology tariffs would make such measure a double-edged sword.

There could be more complications for Nvidia in the foreseeable future. Since the U.S. tariffs tech hit list is not out yet, if Chinese-manufactured chips and electronics components make the list, hardware makers and component distributors will be worse off. If finished goods from contract manufacturers are being levied the tariffs, then Nvidia will be hurt. As Nvidia has more than 60% of supplies imported from Asia and 34% of the revenue from the same region, the closely integrated relationship may become hardly distinguishable when it comes to U.S. tariffs and China retaliation tariffs. As semiconductor is the fastest growing technology and focused industry in China, it would seem as if Nvidia and AMD are the most vulnerable to both Trump’s tariffs and China’s retaliation. Because of this consideration, I have estimated AMD and Nvidia’s exposures to both Trump tariffs and China retaliation tariffs. Both company’s U.S. tariffs exposure is measured by each company’s cost distribution of its Asian suppliers, while the China tariffs exposure is measured by the revenue distribution of their Asian customers.

Level-1 Asian Suppliers

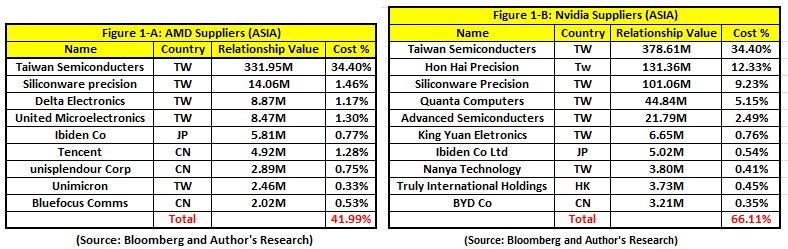

“Level-1” suppliers are the top 9-10 Asian companies directly providing products to AMD and Nvidia. They will take the full impact of the 25% US imported tariffs. Both companies will have to pay the additional cost to the level-1 suppliers if they choose to pass the entirety of the tariffs to the U.S. importers. In Figure 1-A & Figure 1-B, I identified the top 9 (10) largest Asian suppliers for AMD (Nvidia) with each of its cost contribution to the company. It is interesting to note that Taiwanese firms provide 65% Nvidia and 38% of AMD’s costs of goods sold, while the Chinese suppliers only represent 2.5% AMD and 0.35% to Nvidia. The sharp difference between Taiwan and China poses important implications. First, if Trump tariffs are only directed to China, it appears to be ineffective, at least to the semiconductor industry. As the data indicates, both AMD and Nvidia are practically not affected by the U.S. tariffs.

Taiwan vs. China

Taiwan vs. China

One unlikely twist is that Trump’s undisclosed hit list may grossly classify Taiwan as part of China, or greater China area. In that case, about 41% of AMD’s cost of goods sold will be subject to U.S. tariffs, while more than 65% of Nvidia’s import cost will be levied. In other words, AMD cost will increase by 10% and Nvidia by 16%. Such increase could be devastating to both firms but least likely simply from the political reality in that region. President Trump has made his intention of separating Taiwan from China very clear by calling Taiwanese “President” at the first day in White House.

“Made in China” vs. “Made by China”

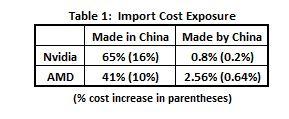

The second complication is that whether tech goods manufactured in China (made in China) or manufactured by Chinese firms (made by China) will be levied is still an open question. This will be a serious factor since most Taiwanese manufacturers have significant production facilities in China. In Table 1, the import cost exposure for each scenario is identified and calculated. For AMD, the exposure can range between 2.56% and 41% and Nvidia from 0.80% to 65%. Applying 25% tariffs to the exposed cost ratio represents the increase in cost. AMD is expected to have a cost increase from 0.64% to 10%, and Nvidia from 0.2% to 16%, depending on how U.S. tariffs apply.

Level-2 Asian Suppliers

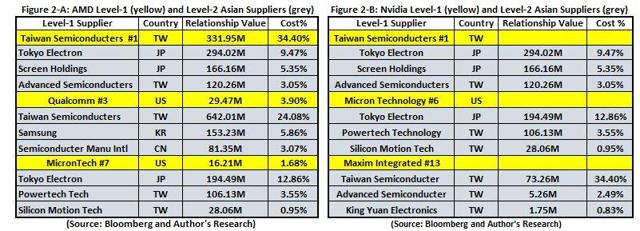

“Level-2” suppliers are any AMD’s suppliers, Asian or not, who provide Asian products to AMD or Nvidia from their own Level-1 Asian suppliers. The need for the identification is that Level-2 suppliers will also pass their increased cost from their Level-1 Asian suppliers to AMD. To make it a bit clearer, I illustrate a real example below for the different cost contribution from both Level 1 and Level 2 suppliers.

Qualcomm is a Level-1 (3.90%) U.S. supplier to AMD and Taiwan Semiconductor is a Level-1 (24.08%) supplier to Qualcomm. Although Qualcomm is not subject to U.S. tariffs, Qualcomm will still pass the cost increase (0.23%) from its Level-1 Asian supplier’s U.S. tariffs burden to AMD (Figure 2-A and Figure 2-B). There may be some remote chance that AMD may be exposed to some Level-2 Asian suppliers even if there is no transaction between the two. Though, the derived effect should be minimal. Thus, in a way, AMD may be exposed to the Level-2 Asian suppliers. In short, the nine Level-2 suppliers may add another 1%-1.5% to the AMD’s Level-1 suppliers’ 44% cost exposure.

As the supply tree can theoretically go on forever, that is, the imposition of 25% tariffs serves more like a multiplier which has a far-reaching impact and not just confined within only direct Asian suppliers. The good news is that after Level-2 suppliers, the actual cost increase will quickly converge to a negligible level. For all practical purposes, AMD’s U.S. tariffs exposure on cost should be confined within Level-1 and Level-2 suppliers only, which is around 45% at best. The worst case scenario is that AMD should see up to 10% imported cost increase if the full 25% tariffs apply to 44% of its cost base, and Nvidia’s cost may increase by 16%. However, if Trump’s tariffs are only directed to the tech goods made by Chinese firms, the cost increase for both firms will be negligible between 0.2% and 0.64%.

China’s Retaliation Tariffs

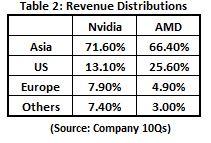

Given the strong and surprising stance of Trump’s tariffs, there will be and there have been retaliations from the targeted countries, i.e. China, Japan, Korea, and Taiwan. So, while Nvidia and AMD may not be significantly affected by Chinese retaliation on the supplier side, it has much larger stake on the Asian revenue side. On this front, Nvidia is more vulnerable than most since it has more than 71% revenue exposure from that region, where AMD has over 66% (Table 2).

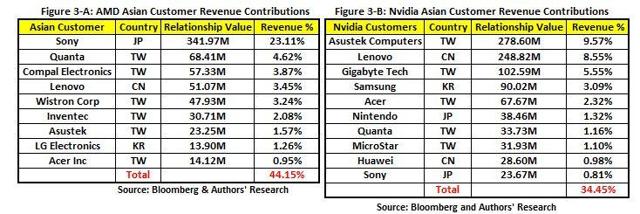

To show this, I further identified AMD’s Asian customers and their revenue contributions. The customer is considered “qualified” if its revenue contribution can be individually identified. The “unqualified” customer is the one that its revenue is estimated approximately based on its market capitalization (Table 3-A). AMD has around 44% of Asian qualified revenue and 22% of unqualified revenue. Nvidia has 34% of Asian qualified revenue and 37% of Asian unqualified revenue (Table 3-B).

Realistically, the most likely country to impose a retaliation tariff is China. This is because that China is the main target of Trump’s tariffs. At this point, Nvidia has around 9.5% China revenue exposure and AMD 3.4% are at risk if Trump tariffs are restricted to China only. Given the relatively small revenue portion that each firm is exposed to China retaliation tariffs, even with a similar 25% tariffs levied on the U.S. revenue, it is hard to imagine that there is a significant loss in revenue for both companies in the end. Furthermore, considering the political reality in that region, it is less likely that Japan, Korea, and Taiwan will join suit with China to organize a coordinated tariff in retaliation.

Finally, many have considered that the recent exchanges of tariffs threats between the U.S. and China are no more than political posture and reelection campaign rhetoric. Just days after Trump’s announcement, China has taken off 201 tariffs on Apple (NASDAQ:AAPL) after Apple donated $400 million to poor Chinese students. According to some reports, China has offered to increase the purchase of U.S. semiconductor chips, replacing offerings from South Korea and Taiwan. Thus, it stands to reason that the tariffs’ impact on AMD and Nvidia’s revenue and cost should be measured and contained.

With less than 1% net negative impact on both companies’ bottom line from tariffs, NVDA and AMD’s 10% losses in market capitalization since March 26’s announcement seem excessive.

Disclosure: I am/we are long NVDA.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment