I use several quantitative methods to source investment ideas. One of them is similar to the Trending Value strategy described in the book What Works on Wall Street. The strategy I employ here is actually one the best of the 300 strategies described there.

This strategy ranks US stocks with positive momentum on various value factors. One of the biggest differences with the book is that I rank on smooth momentum instead of on raw momentum. Smooth momentum suggests many knowledgeable investors are slowly buying into the stock.

Please see this free overview article of mine for more details on the 4 different quantitative strategies I use.

Tatneft

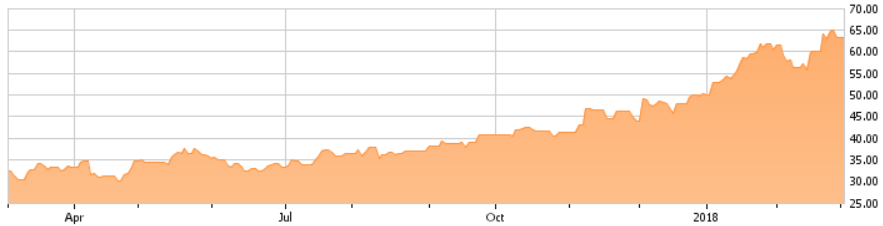

Tatneft (OTCPK:OAOFY) has the fourth best ranking on this month’s list. The ranking ignores recent momentum because this is subject to mean reversion. My ranking considers smoothness of momentum but unfortunately I do not have many price points for this automated judgement. Therefore I improve this automated smoothness analysis by looking at the charts myself. Based on the chart I think this is one of the best value/momentum stocks this month:

{kind=link}

This month’s list compares valuations and momentum of 853 selected stocks. These stocks have been selected on momentum criteria and fundamentals (mainly EV/EBIT < 20). Among these selected stocks 97% of the stocks have a less favorable rank on a combination of multiple value factors.

In particular Tatneft is relatively cheap based on P/E, EV/EBIT and Price/8-years of retained earnings. Market cap/Total retained earnings is about 2, which is not great compared to the cheapest international value stocks. Liquidity is low, even when taking liquidity in London and Moscow into account. Low liquidity compared to the public float predicts good returns.

Tatneft is a vertically integrated oil producer from the Russian republic Tatarstan. The Tatarstan government owns 36% of the company and has a golden share to prevent the company being acquired. The board of directors has 15 members including 5 board members with strong ties to the Tatarstan administration. The Management board has 11 members. Such large boards predict lower statistical returns.

The company produces almost all its crude oil in the Russian republic Tatarstan. The company pumps up regular crude and also highly viscous crude oil, or bitumen. Production of regular crude declined a bit compared to last year. Highly viscous oil is only a small part of the production but that production went up much. The company intends to further increase production of highly viscous oil. About 30% of the company’s capex goes into development of viscous oil fields.

In any case the company has enough reserves for many years of production. Proven reserves have been estimated at 870 million tonnes and annual production is only 27 million tonnes. Relative to production these reserves are much higher than reserves of most other oil companies. Unfortunately I could not find the present value of these reserves when discounting with 10%, aka the PV10.

On its website the company says there are over 1.4 billion tonnes of bitumen reserves in the republic Tatarstan. I guess most, if not all, of these 1.4 billion tonnes of bitumen reserves will eventually be recognized in the company’s books. Right now the production of bitumen is still in pilot phase. I could not find which part of the company’s proven oil reserves are bitumen. Since the reserves have been measured in 2015 and the bitumen project is still in pilot phase I assume hardly any bitumen reserves have been categorized as proven.

Over 70% of its production is exported, mainly to Poland, Germany and the Czech Republic. World market prices for its oil are 2-4% below the price of Brent oil. The company sells crude oil in Russia for more than 20% less than world market prices. The company also produces refined products. This includes 11.9 million tires. About half of the refined products are exported.

Apart from oil producing and oil refining assets the company operates about 690 gas filling stations, mostly in Russia, and owns a majority stake in a small bank. I estimate this stake is worth at least $200 million. There are also for over $400 million of claims depending on litigation and for about $100 million of non-producing oil assets in Libya.

Though the company is composed of different businesses only the oil production business is important. Almost all earnings come from the exploration and production segment, see here. Assets of the each of the segments exploration and production, refining and banking are similar in size. So the other 2 segments are inefficient in terms of the ratio Earnings/Assets. Management may think the sum is worth more than the parts but I think the opposite is true.

See also Tatneft’s website for many key numbers. This is one of the few scarcely covered large caps, with desirable assets and a strong balance sheet with low leverage. To give you an idea of the size of Tatneft some basic numbers over the 12 months ending on September 30, 2017 are below, in billions USD:

|

Revenue |

12.4 |

|

Share price (1 ADR = 6 shares) |

64.6/ADR (595 ruble/share) |

|

EPS |

5.7/ADR |

|

Market cap |

24.4 |

|

Enterprise value |

23.3 |

|

Book value |

13.3 |

|

Tangible book value |

13.3 |

|

EBIT |

2.79 |

|

EBITDA |

3.22 |

|

Free cash flow |

1.54 |

|

EV/EBIT |

8.4 |

Final remarks

Investing in this integrated oil company is a bet on oil, and on the Russian economy. So the oil price can make it go up and down. Since the world economy is running on all cylinders I think it won’t be long before oil prices further recover. That should increase the company’s profits on sales of crude. I also think the company will increase its oil production, in particular production of highly viscous oil. Higher oil prices will also lead to increased investment and government spending in Russia. That will be good for the company’s sales of refined oil products.

Informed investors seem to have bid the stock slowly up already for some time. Apparently they believe global developments and developments around oil production or proven reserves will be favorable for Tatneft.

Lastly, a concern is of course Russian leadership. I am optimistic. With this company shareholders continue to get their dividend. I do not think the Russian government will nationalize this oil company either.

I do not invest in these US-listed stocks since stocks I find with my international screener are much cheaper and therefore have higher average returns. See again my free overview article Use your extraordinary edge with these 2 investment strategies for details.

Join me here if you like having many statistically favorable positions instead of having a few high-conviction stocks.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment