Introduction

Sometimes the best oil investments aren’t found on a large exchange like the NYSE or the London Stock Exchange. Lundin Petroleum (OTCPK:LNDNF) (OTCPK:LNDNY) (OTCPK:LUPEY) is a Swedish oil company focusing on Norwegian oil fields, trading on the Stockholm Stock Exchange. The company has a stake in the huge Johan Sverdrup oil field which it’s jointly developing with Statoil (STO), and appears to be undervalued based on its low production costs and expected production growth.

Source: finanzen.net

As the company’s main listing is in Swedish Crowns, its current market capitalization of 69B SEK is approximately $8.72B USD using an USD/SEK exchange rate of 7.91. The shares are currently priced at 204.5 Swedish Crowns on the Stockholm stock exchange, where Lundin Petroleum is trading with LUPE as its ticker symbol. The average daily volume is 960,000 shares for a total dollar volume of approximately $25M per day.

Source: stockcharts.com

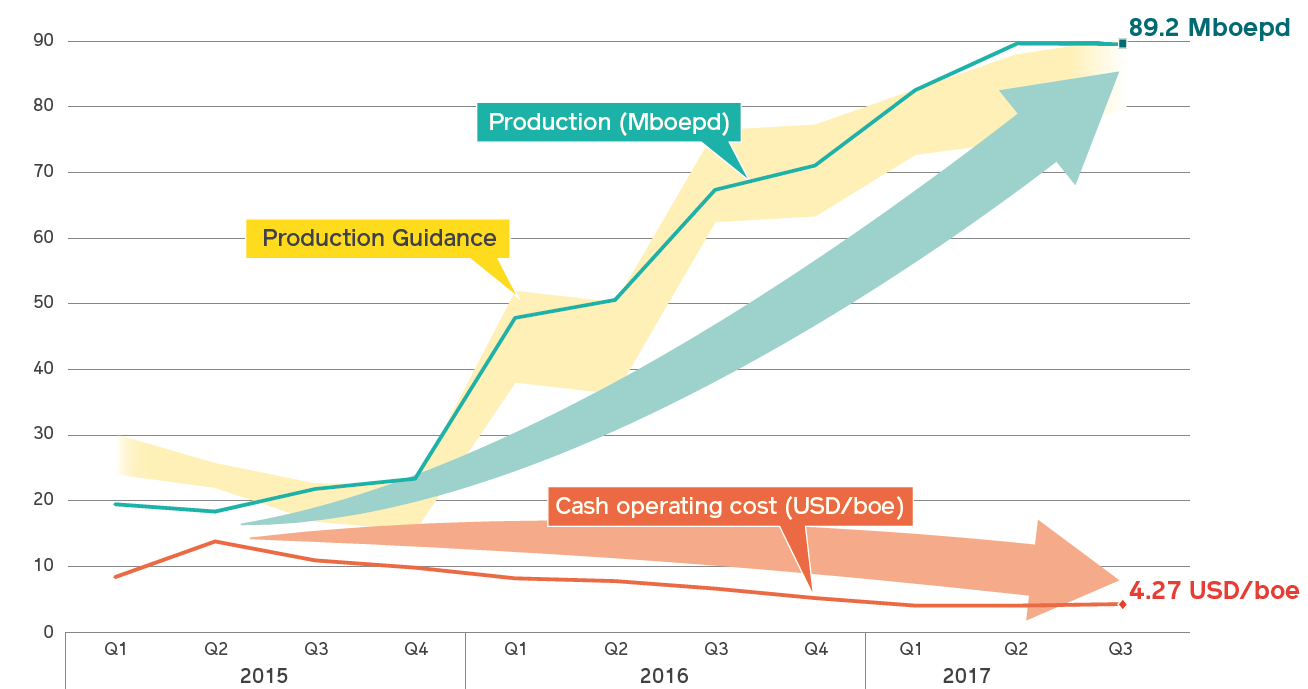

Perhaps one of the lowest cost producers out there

Investors in the oil sector can be subdivided into roughly three categories. The first category would be the ‘pure’ speculators which are hoping for a company to make a (commercial) discovery, whilst a second category of oil investors is buying high-cost of overleveraged oil producers as those will provide the biggest leverage when the oil price increases.

I belong to a third category: I like to have an (enormous) margin of safety to make sure that if/when the market moves against me, my investees don’t go under. That’s why I like the low-cost producers. Sure, the margins won’t increase as much as higher cost producers when the oil price increases, but if I’m producing oil at $10/barrel, I still sleep well at night even if oil would be trading at just $40/barrel (on the condition the company also has a decent balance sheet).

Source: company presentation

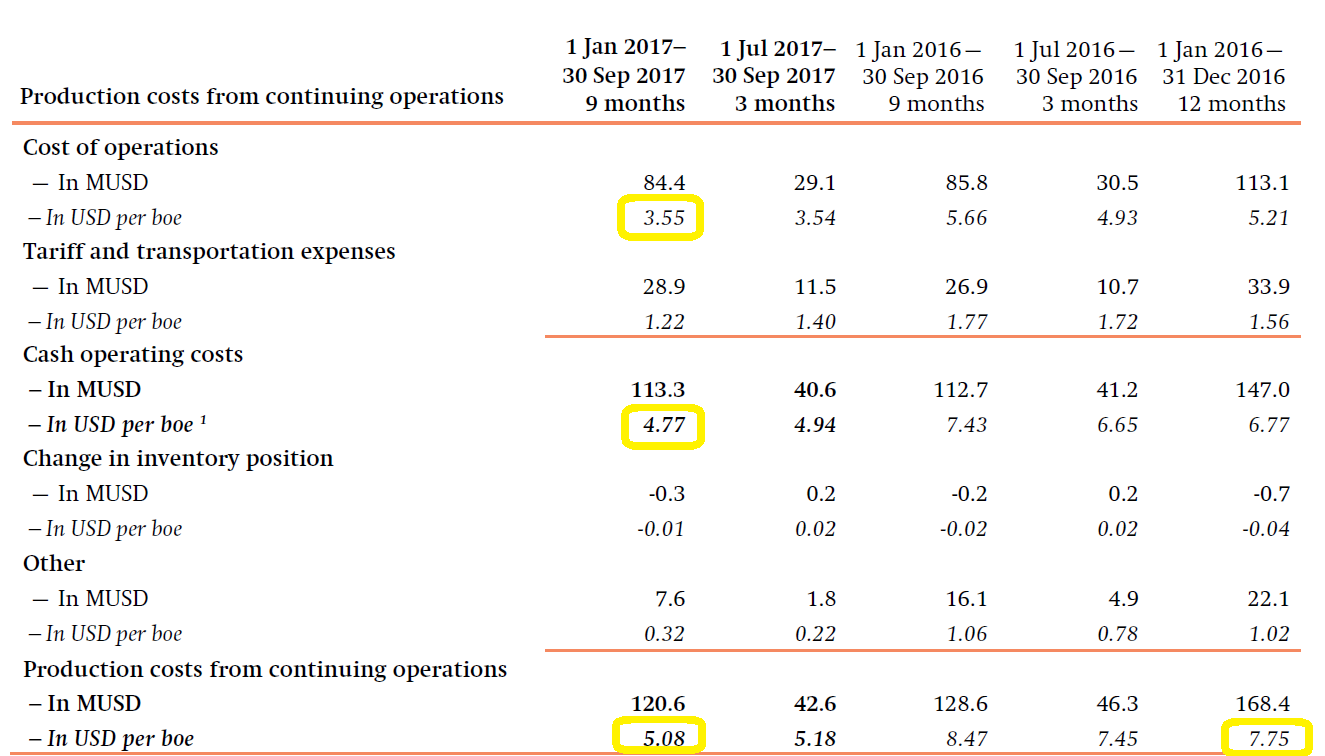

Lundin Petroleum is a company which really fits my bill. The company is being run by oil veterans and is producing its oil at a shockingly low production cost of less than 5 dollars per barrel. That’s right. In the first nine months of 2017 (we are still waiting to see the full-year result), the pure production cost of Lundin Petroleum was just$3.55 per barrel of oil, increasing to $4.77 per barrel once you include the tariff and transportation expenses.

Source: Lundin Petroleum quarterly update

On a fully-loaded cost basis (including the proceeds/expenses related to the business interruption insurance and the cost share agreement on the Brynhild oil project – where the expenses were based on the oil price), the production cost was just $5.08 per barrel, down from an already low $7.75 per barrel in FY 2016.

This means the company was able to sell its average production rate of 87,100 barrels per day at an average oil price of almost $50/barrel for a total revenue of $1.4B and an EBITDA of $1.07B. Indeed. Even when the oil price was still relatively weak, Lundin Petroleum reported an EBITDA margin of approximately 76%. Phenomenal.

Source: financial statements

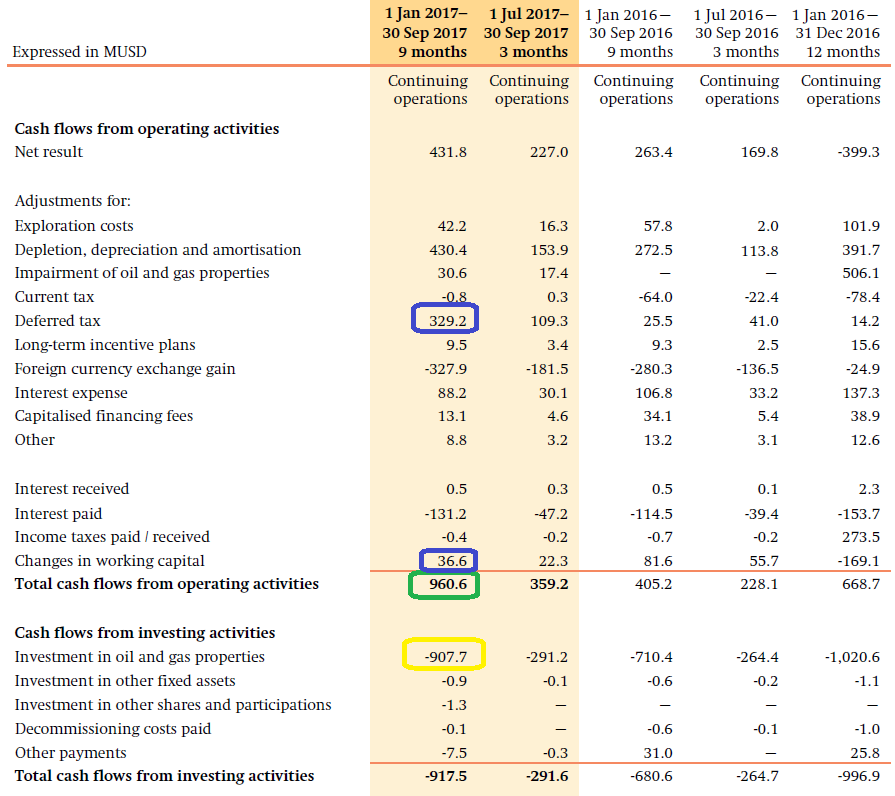

Looking at the cash flow results of Lundin Petroleum in the first nine months of the year, it’s clear why Lundin Petroleum effectively is a cash cow. The operating cash flow in the first nine months of the year was approximately $961M , but this included a lower tax bill (as the majority of the taxes were deferred) and a positive contribution from working capital changes. If we would adjust the operating cash flow for both ‘issues’, we would have ended up with approximately $600M in operating cash flow.

Growth, growth, growth

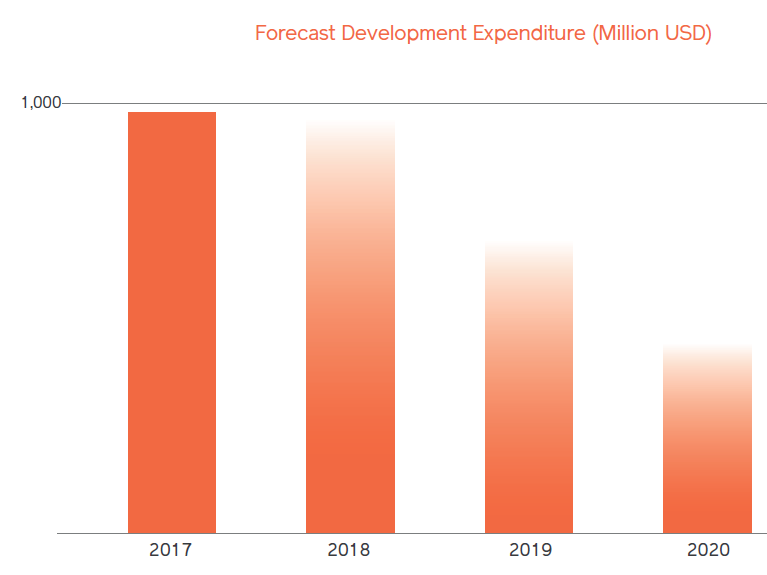

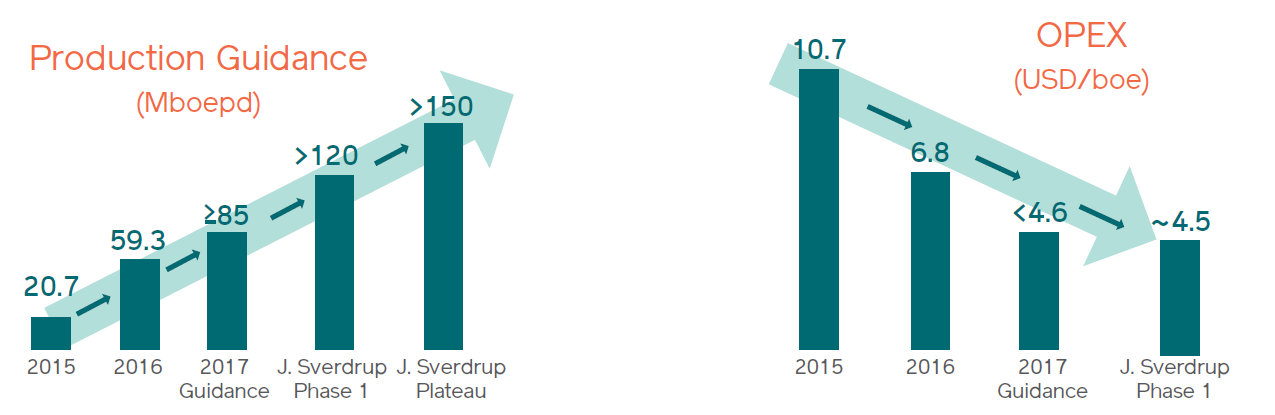

This wasn’t sufficient to cover the $908M in capital expenditures, but Lundin Petroleum is on the verge of reaching ‘peak spending’. Have a look at the next image, published in the company’s official corporate presentation:

Source: company presentation

As you can see, the capex will fall by 50% by 2020, but in combination with a lower capex level, the production rate will actually increase towards 120,000 barrels per day in 2020-2021:

Source: company presentation

This allows us to extrapolate the 9M 2017 results into a longer-term view (as the production cost will remain pretty stable).

Step 1 would be to extrapolate the 9M operating cash flow of $600M to the full-year result, which is an easy calculation resulting in $800M. Secondly, by using the 120,000 boe/d production rate, we also need to increase the cash flow by the same percentage (+37.8%). Keeping the oil price stable, this means we can reasonably expect the full-year operating cash flow to be approximately $1.1B.

But that’s based on an average Brent oil price of approximately $52/barrel ($50/barrel effectively received). If I would now apply a Brent price of $56/barrel (with a $4 net revenue increase per barrel, setting $2/barrel aside for taxes and tariffs), the operating cash flow would increase to $1.3B.

If the capex then indeed drops to $500-600M per year, the free cash flow will increase to $700-800M per year, for a free cash flow yield of almost 10%. And that’s just after incorporating Phase I of Johan Sverdrup (2019). Once Phase II is up and running (2022), the total production rate will increase by an additional 25%. Assuming a similar Brent oil price, the free cash flow result could approach $1B by 2022-2023.

The financial results aren’t in yet, but the reserve update is!

The financial results over 2017 will be published next week, and I expect these to be really good as the fourth quarter should be exceptionally strong thanks to the higher oil price.

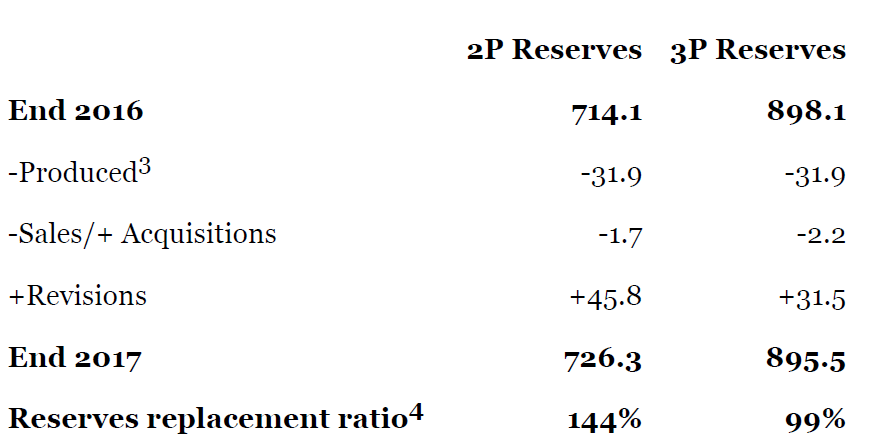

Although some oil and gas companies publish their reserve updates at the same time as their financial results, Lundin Petroleum has just updated its oil reserves and resources. The total amount of 2P reserves came in at 726 million barrels, which is 12 million barrels more than the reserve report at the end of 2016. The reserves replacement ratio was approximately 144%, which means Lundin has added 44% more barrels to the 2P Reserves than it has produced.

Source: press release

The 3P reserves decreased by 2.6 million barrels for a replacement ratio of 99%, which is fine as well, as Lundin’s focus hasn’t really been on expanding the 3P reserves (which include the possible reserves on top of the more ‘reliable’ proved and probable reserves).

Using an annual oil production rate of 44 million barrels per year (based on 120,000 barrels per day from 2020 on), the current size of the 2P reserves is sufficient to underpin a total ‘production life’ of 16.5 years. And that’s good enough for now!

Investment thesis

Whilst Lundin Petroleum might not look too appealing right now due to the high level of capital expenditures, the company is slated for a turnaround. Whilst the capex will decrease, the production rates will increase and even at a (lower) Brent oil price of $55/barrel, it looks like the free cash flow might come in at $700-800M by the time the first phase of the Johan Sverdrup oil field will go in production in 2019. This could increase to $1B per year from 2022 on when the second phase of the oil project will be ‘ready to go’.

There still are some issues to be cleared up, as Lundin Petroleum and its executives have been named in a lawsuit for crimes against humanity in Sudan. The net debt and debt levels are also relatively high, but should decrease relatively fast as the EBITDA will increase whilst the free cash flow will be used to reduce the net debt. But for now, the risk/reward ratio looks appealing. Keep in mind the production rate in FY 2018 will decrease to 74-82,000 boe/day, but the total capex level will also decrease by almost $200M to $800M, so I expect Lundin Petroleum to break even on the cash flow front in 2018.

______________________________________________________________

Consider joining European Small-Cap Ideas to gain exclusive access to actionable research on appealing Europe-focused investment opportunities, and to the real-time chat function to discuss ideas with similar-minded investors!

Most of the companies discussed there don’t have US ticker symbols, so the service will only be useful if your broker grants you access to European markets (Interactive Brokers, Fidelity, or pretty much any Europe-based broker).

_______________________________________________________________

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment